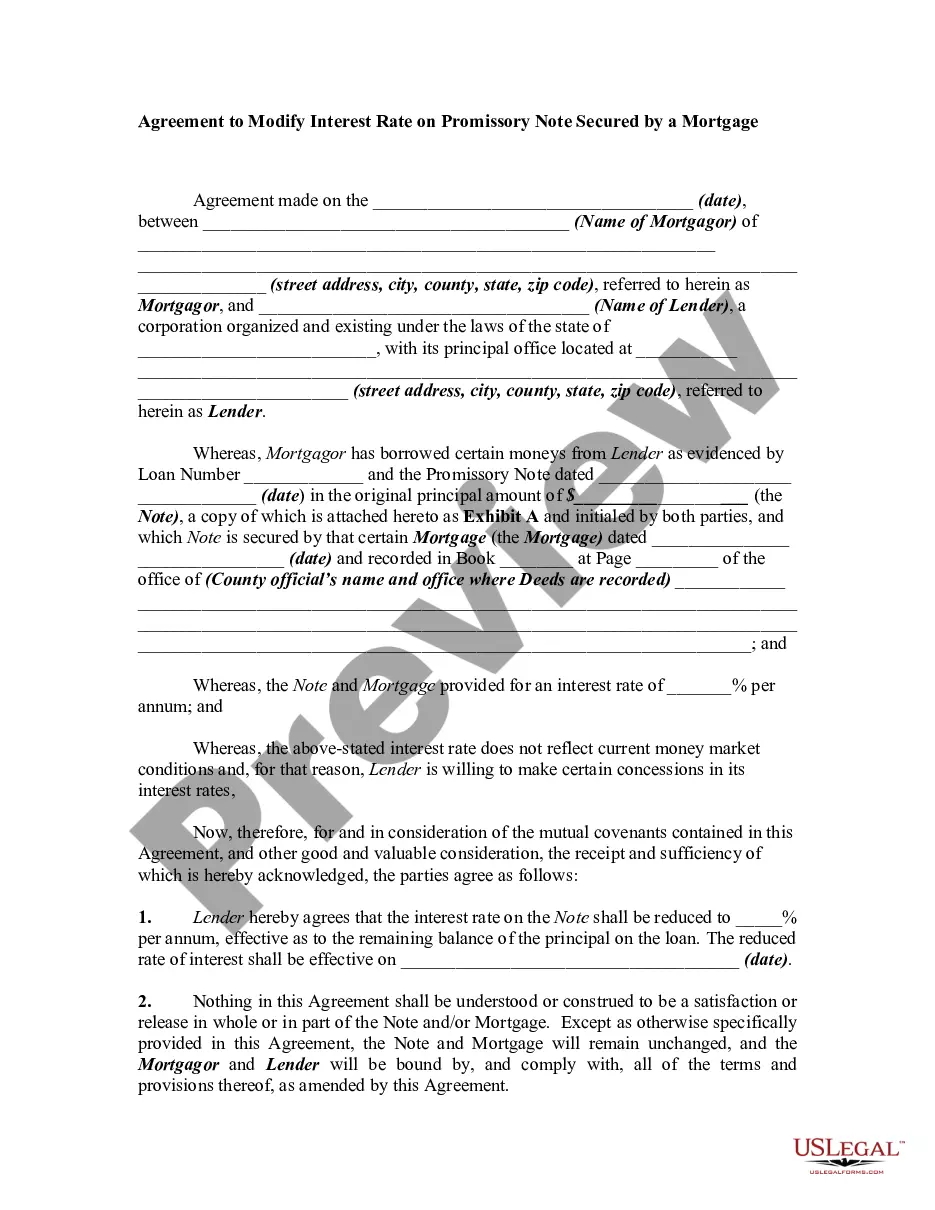

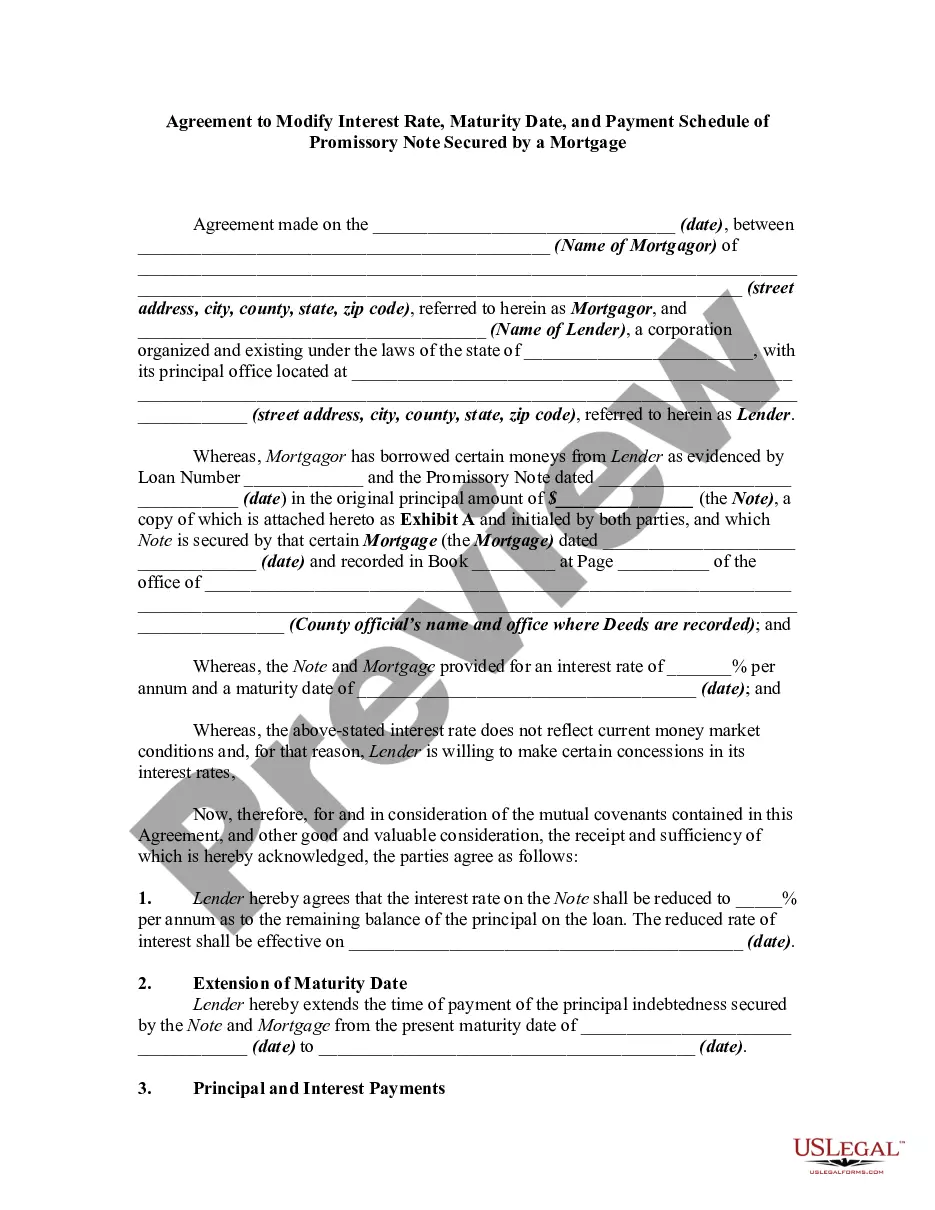

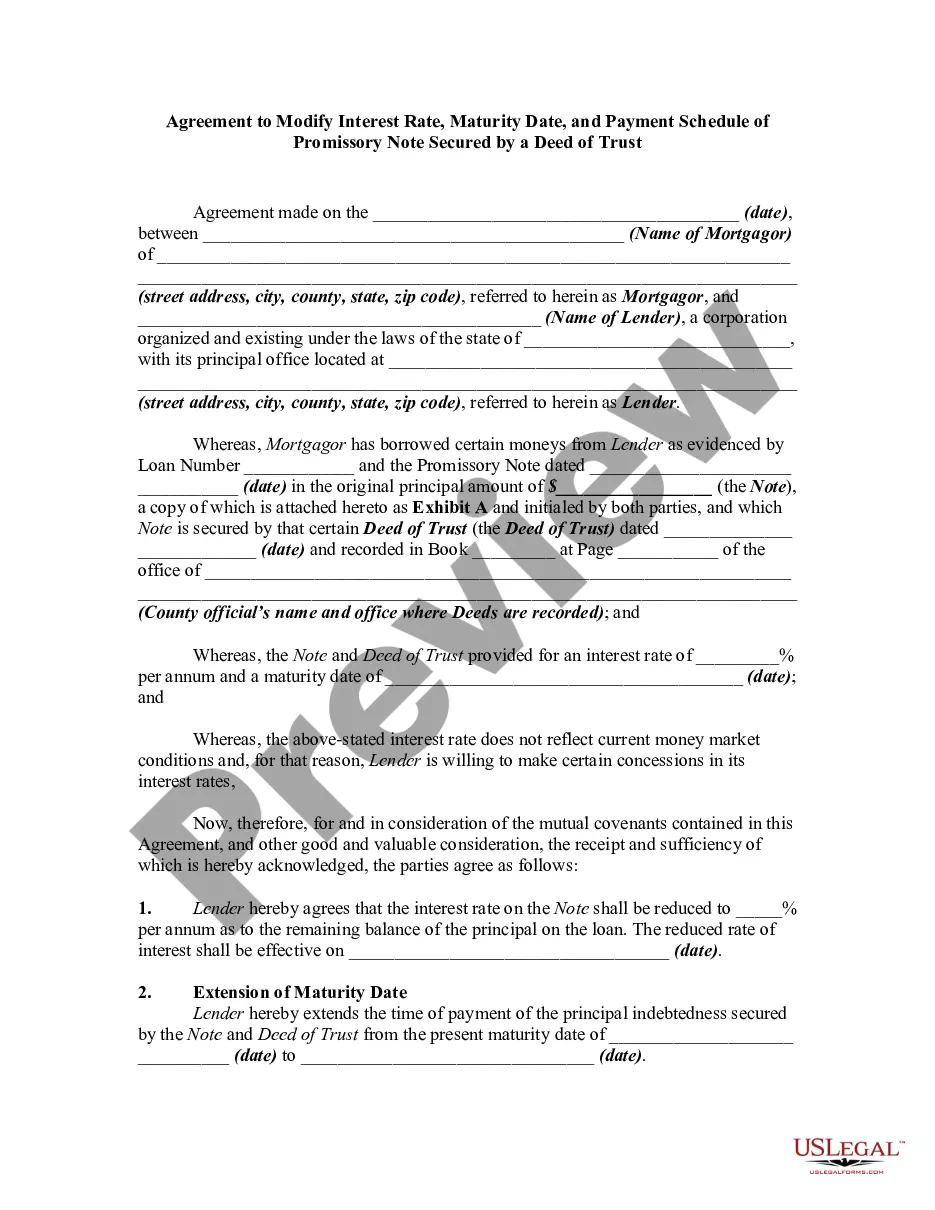

Agreement to Modify Promissory Note and Mortgage to Extend Maturity Date

Overview of this form

The Agreement to Modify Promissory Note and Mortgage to Extend Maturity Date is a legal document that allows parties to change the terms of an existing promissory note and mortgage. This form specifically addresses the extension of the maturity date for repayment, which differs from other loan modifications that may involve changes to interest rates or payment amounts. It is essential for both mortgagor and lender to formalize their agreement through this document to ensure clarity and legal compliance.

Key components of this form

- Date of the agreement

- Name and details of the Mortgagor and Lender

- Loan information, including the original principal amount and Loan Number

- Extension details for the maturity date of the Note

- Terms of principal and interest payments

- Governing law clause

- Notarization requirements

Common use cases

This form is needed when a borrower (Mortgagor) and a lender agree to extend the due date for a loan repayment outlined in a previous promissory note and mortgage. Common scenarios include financial hardship for the borrower or changing market conditions that affect repayment terms. It is crucial when both parties wish to avoid foreclosure or to maintain their existing mortgage relationship under new terms.

Who needs this form

- Homeowners (Mortgagors) seeking to extend their loan maturity dates

- Lenders, including banks or financial institutions, handling loan modifications

- Attorneys representing either party in a mortgage agreement

- Any authorized parties who are involved in the original loan agreement

Instructions for completing this form

- Identify and enter the date of the agreement at the beginning of the document.

- Fill in the names and addresses of both the Mortgagor and the Lender.

- Provide details about the original loan, including the Loan Number and principal amount.

- Specify the current and new maturity dates for the loan repayment.

- Include terms for interest payments and agree on any additional modifications.

- Ensure both parties sign the agreement in the presence of a notary if required.

Does this document require notarization?

To make this form legally binding, it must be notarized. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include all necessary parties' names and signatures.

- Not specifying the correct maturity dates or interest rates.

- Omitting required notary acknowledgments when necessary.

- Not recording the modified agreement in the appropriate register office.

Benefits of using this form online

- Convenient access to legally vetted templates at any time.

- Easy to customize based on specific needs and circumstances.

- Quick download for immediate use and recordation.

Looking for another form?

Form popularity

FAQ

In the unlikely event a borrower defaults on a promissory note, it is the lender's responsibility to execute the collection action necessary to claim the item(s) used as collateral. These actions may include: Foreclosure (for real estate investments) Repossession.

The Promissory Note is hereby modified and amended by deleting the last sentence of the first paragraph of the Promissory Note in its entirety, and replacing it with the following: All outstanding principal and interest shall be due and payable on June 3, 2012 (the Due Date).

The Loan shall be evidenced and governed by a new promissory note (the New Note) which amends and restates in its entirety, but does not extinguish, the Note. Anything to the contrary notwithstanding, if any inconsistency exists between the Loan Agreement and the New Note, the New Note shall control.

Identify the terms of the note that are creating difficulty in repayment. Communicate your need to modify the terms of the note to the note holder. Have the holder of the note draft modifications to the original note. Tip.

A loan extension agreement allows the maturity date to be extended on a current note. The agreement amends the current loan along with any other terms that agreed-upon by the lender and borrower.

Loan modification is better for the lenderLoan modification isn't the same as refinancing, which helps you get a better interest rate if you have a good enough credit score. Instead, loan modification tends to be the best option for a homeowner whose credit is bad and can't refinance the loan.

Under this option, you reach an agreement between you and your mortgage company to change the original terms of your mortgagesuch as payment amount, length of loan, interest rate, etc. In most cases, when your mortgage is modified, you can reduce your monthly payment to a more affordable amount.

A promissory note is a contract, a binding agreement that someone will pay your business a sum of money. However under some circumstances if the note has been altered, it wasn't correctly written, or if you don't have the right to claim the debt then, the contract becomes null and void.

A loan modification can improve your terms and save you money without the cost and hassle of a refinance. Unlike a full refinance, a loan modification is not a new note, nor is it a replacement of your original note. It is simply an addendum to the original document, changing the terms as agreed.