Standardized Form for Referral of Claim for Collection

What is this form?

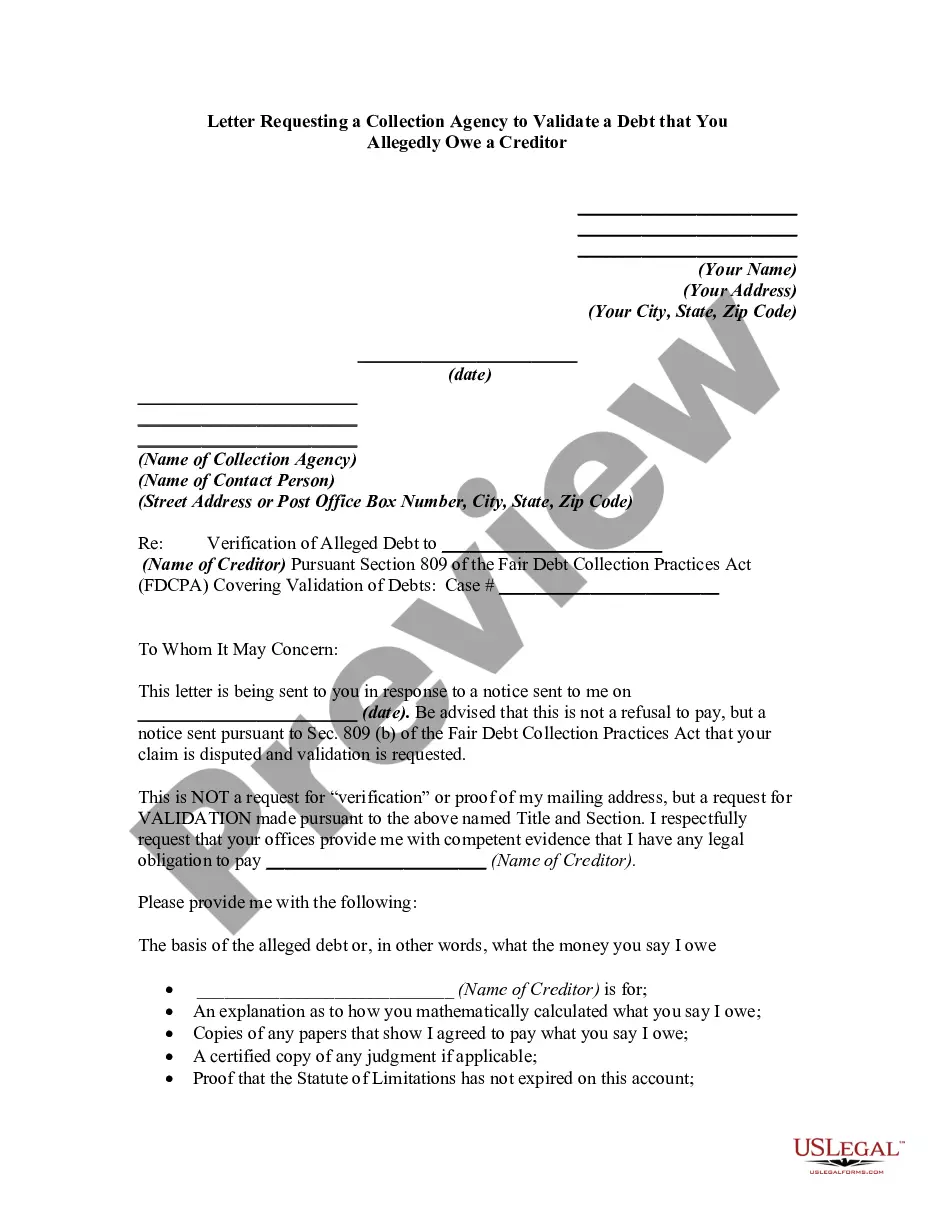

The Standardized Form for Referral of Claim for Collection is a legal document used to formally transfer a debt to a collection agency for collection efforts. This form standardizes the process, ensuring clear communication regarding the assignment of the claim, which allows the agency to take action when necessary. Unlike informal collection notices, this standardized form helps protect both the creditor and the collection agency by clarifying rights and responsibilities under the law.

Key components of this form

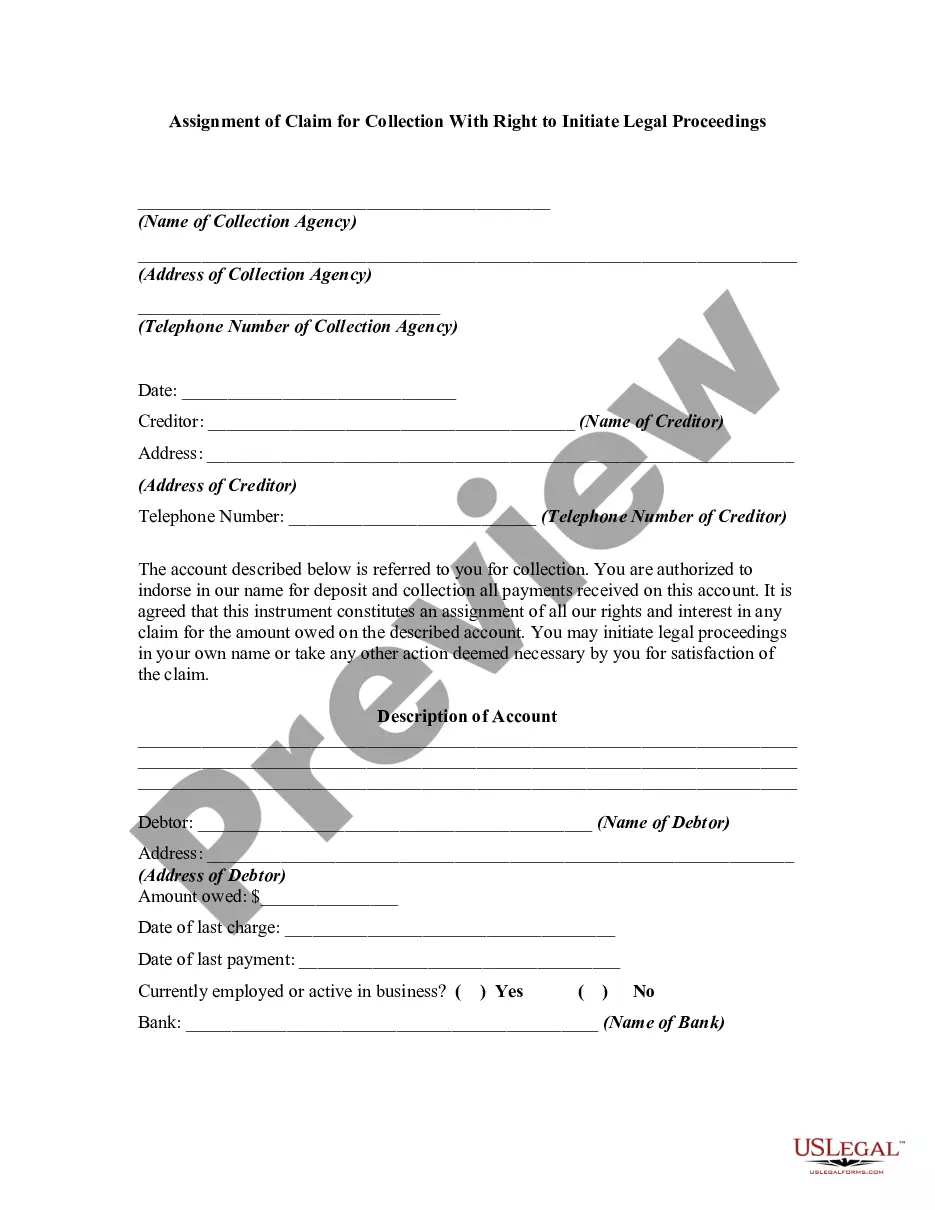

- Name and contact information of the collection agency

- Name and contact information of the creditor

- Description of the account being referred for collection

- Name and address of the debtor

- Details regarding the amount owed and payment history

- Authorization for the collection agency to deposit payments

Situations where this form applies

This form should be used when a creditor has made multiple attempts to collect a debt but has been unsuccessful. It allows creditors to efficiently transfer the responsibility of debt collection to a professional agency. Using this form is advisable when creditors seek to ensure that collection efforts comply with relevant legal standards and within the framework of their jurisdiction.

Who can use this document

- Creditors who have delinquent accounts needing collection

- Businesses looking to streamline their debt collection process

- Individuals who have extended credit and require professional collection assistance

Completing this form step by step

- Identify and enter the name and contact details of the collection agency.

- Provide your name and contact information as the creditor.

- Detail the debtor's information, including their name and address.

- Fill in the account information, specifying the amount owed and any relevant dates.

- Include instructions regarding payment and communication, including the collection agency's authority.

- Ensure that all parties sign the form to validate the transfer of the claim.

Notarization guidance

This form does not typically require notarization unless specified by local law. Ensure to verify local regulations to determine if notarization is necessary for validity in your jurisdiction.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include all necessary contact information for both creditor and collection agency.

- Not detailing the description of the account clearly.

- Leaving out the signature of the creditor, which can invalidate the form.

- Using vague or unclear language that may result in misunderstandings.

Advantages of online completion

- Convenience of downloading and completing the form at your own pace.

- Editable format allowing for easy customization to fit specific needs.

- Reliability from using attorney-drafted templates ensuring legal compliance.

- This form serves as a formal notice of assignment for the collection of debts.

- It enables the collection agency to act in the creditor's name, facilitating legal action if authorized.

- Proper completion and execution of this form can improve enforceability in collection attempts.

Looking for another form?

Form popularity

FAQ

If the debt is still listed on your credit report, it's a good idea to pay it off so you can improve your credit card or loan approval odds. Keep in mind that paying the debt won't remove it from your credit report (unless you negotiate a pay for delete), but it does look better than the alternative.

If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.

Debt collectors report accounts to the credit bureaus, a move that can impact your credit score for several months, if not years.The late payments and subsequent charge-off that typically precede a collection account already will have damaged your credit score by the time the collection happens.

You can improve your credit score by getting these collection accounts deleted from your report or at least having them reported as Paid or Current. Before you pay off a collection account, first negotiate with the debt collector to have your credit report updated to something favorable.

If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.

Contrary to what many consumers think, paying off an account that's gone to collections will not improve your credit score. Negative marks can remain on your credit reports for seven years, and your score may not improve until the listing is removed.

If the debt is still listed on your credit report, it's a good idea to pay it off so you can improve your credit card or loan approval odds.8feff On the other hand, if the debt is going to drop off your credit report in a few months, it may be better to just wait and let it fall off.

Request a Goodwill Deletion If You Have Paid The Debt. If this sounds overwhelming, you might want to reach out to a credit expert. Dispute the Collection If You Found An Error. Ask the Collection Agency to Validate the Debt. Negotiate a Pay-for-Delete Agreement.