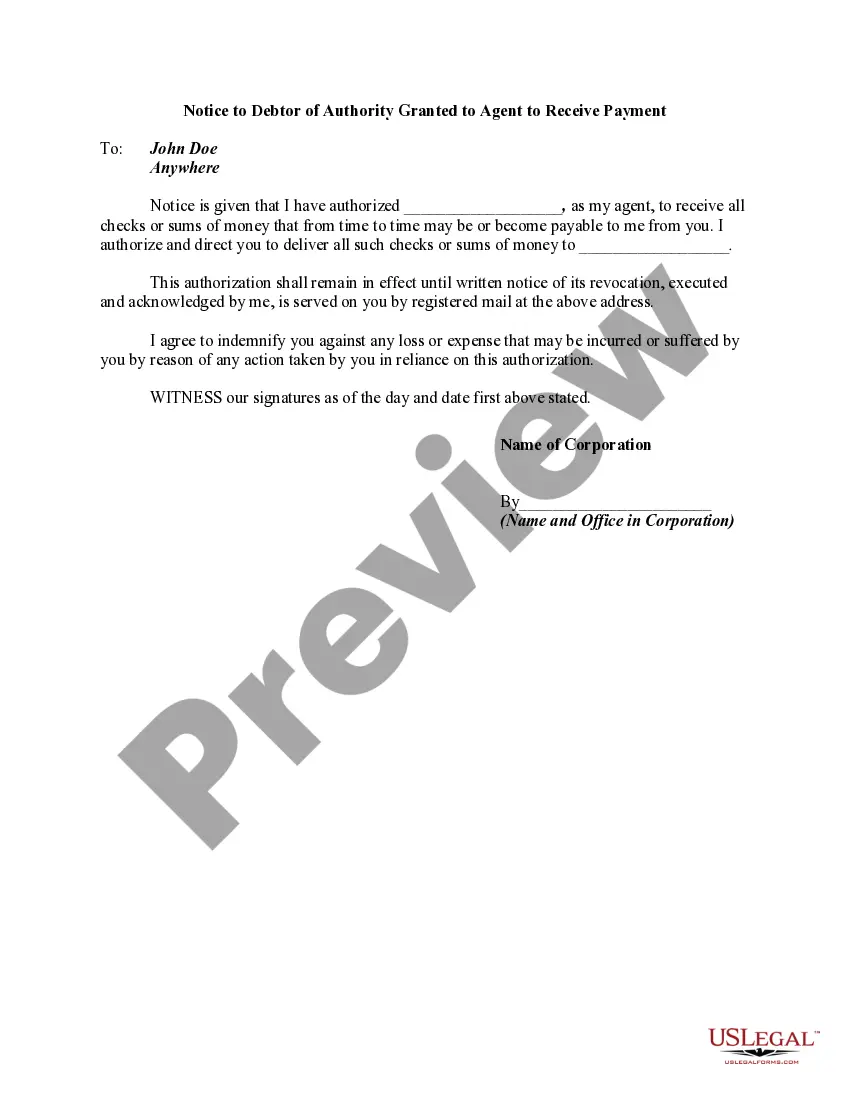

Notice to Debtor of Authority of Agent to Receive Payment

What this document covers

The Notice to Debtor of Authority of Agent to Receive Payment is a legal document that informs a debtor that they should send any payments intended for a corporation to an authorized agent. This form establishes an official relationship where an agent acts on behalf of the corporation in receiving payments. Unlike general authorization forms, this notice specifically addresses payment collection, ensuring clear communication between the parties involved.

What’s included in this form

- Identification of the debtor, including name and address.

- Identification of the corporation and the authorized agent.

- Statement of authority given to the agent to collect payments.

- Indemnification clause protecting the debtor from potential losses.

- Notary acknowledgment for legal verification.

Situations where this form applies

This form should be used when a corporation appoints an agent to receive payments from a debtor. It is ideal for situations where the corporation cannot collect payments directly due to logistical reasons or if they prefer to designate a representative for financial transactions. This ensures that the debtor is correctly informed about where to send payments, reducing the risk of miscommunication.

Who this form is for

- Corporations that need to delegate payment receipt to an agent.

- Agents authorized to collect payments on behalf of corporations.

- Debtors instructed to send payments to an authorized agent instead of directly to the corporation.

Steps to complete this form

- Enter the name and address of the debtor at the top of the form.

- Specify the name of the corporation granting authority and the name of the authorized agent.

- Outline the obligations of the debtor to send payments to the designated agent.

- Include the signature of an authorized representative of the corporation, along with their title.

- Have the document notarized by a registered notary public to validate the agreement.

Notarization guidance

This form must be notarized to be legally valid. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to provide complete and accurate contact information for both the debtor and the agent.

- Not having the document signed by an authorized corporate representative.

- Overlooking the notary requirement if mandated by state law.

- Not specifying the exact nature of the payments to be collected, leading to ambiguity.

Why complete this form online

- Immediate access to reliable legal documents drafted by licensed attorneys.

- Conveniently fill out and modify the form as needed from any device.

- Secure online notarization options available for added legal validity.

Legal use & context

- This form serves to formalize the appointment of an agent for the collection of debts, ensuring that payments made to the agent are deemed valid.

- It provides legal protection for both the debtor and the corporation against any disputes regarding payment responsibilities.

- The proper execution and notarization of this document help enforce its terms in a legal context.

Quick recap

- A Notice to Debtor of Authority of Agent to Receive Payment formalizes payment delegation.

- Ensure accurate information and notarization for legal validity.

- Useful for corporations engaging agents in collection tasks.

Looking for another form?

Form popularity

FAQ

When a Debt Collector Calls, How Should You Answer? The phone call from a debt collector never comes at a good timebut the best response is to confront the state of these affairs head-on. You may want to hide or ignore the situation and hope it goes awaybut that can make things worse.

Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. Never Provide Bank Account Information.

At a minimum, it must produce: A copy of the original written agreement between the parties, such as the loan note or credit card agreement, preferably signed by you. If the account has been sold to another creditor, then that creditor must prove that it has the right to sue to collect the debt.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.

Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. Never Provide Bank Account Information.

However there are times when you should not pay a collection agency: If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.

Here's some basic information you should write down anytime you speak with a debt collector: date and time of the phone call, the name of the collector you spoke to, name and address of collection agency, the amount you allegedly owe, the name of the original creditor, and everything discussed in the phone call.

Find out background information of the collector. Focus on business. Make a partial payment of the debt, enough to cover the commission of the collector. Do not bow to any threats but instead ask to speak to a senior staff. In case of a threat to sue, reason with the company of the extra cost involved in the process.