Sample Letter for Payoff of Loan held by Mortgage Company

Understanding this form

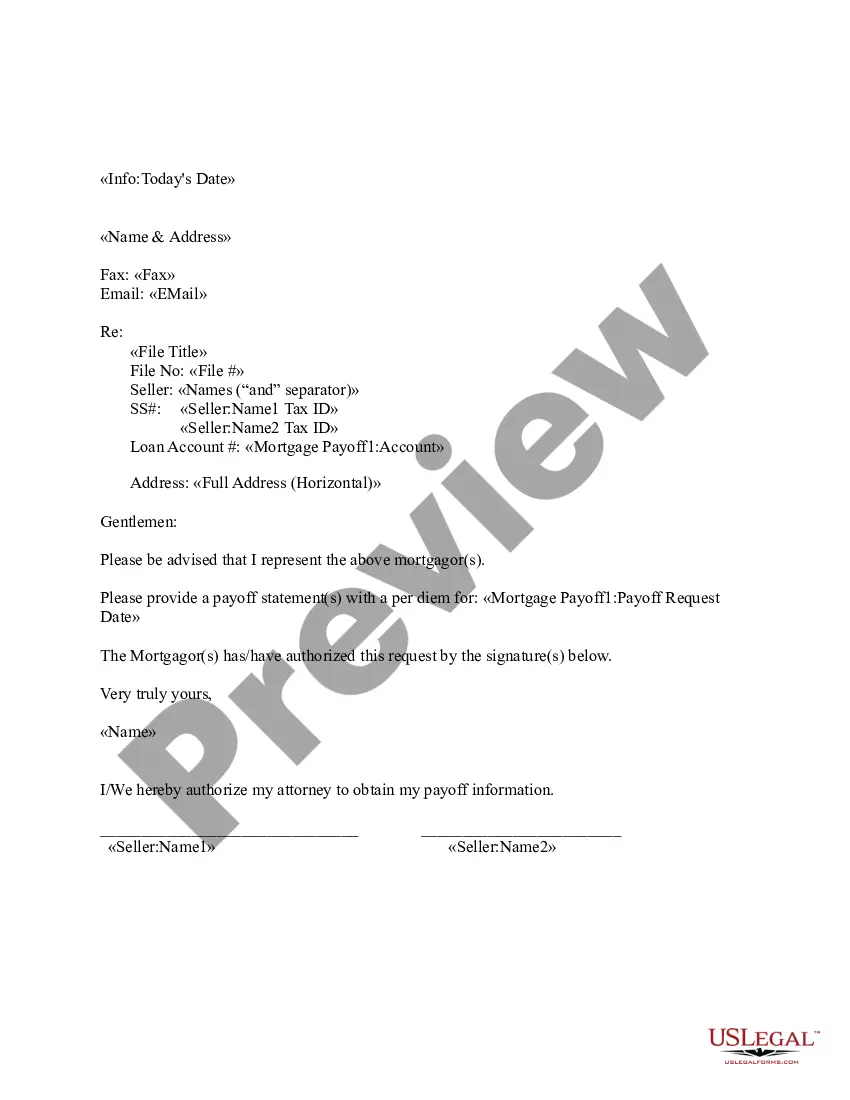

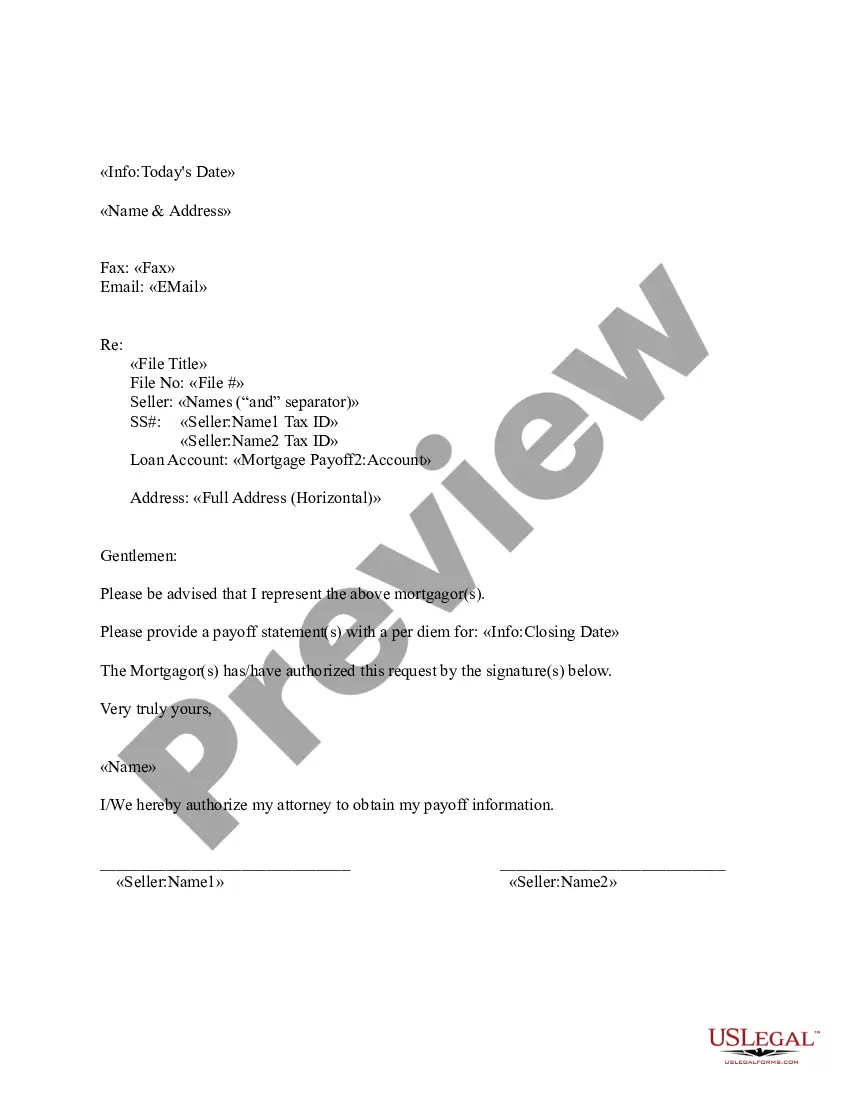

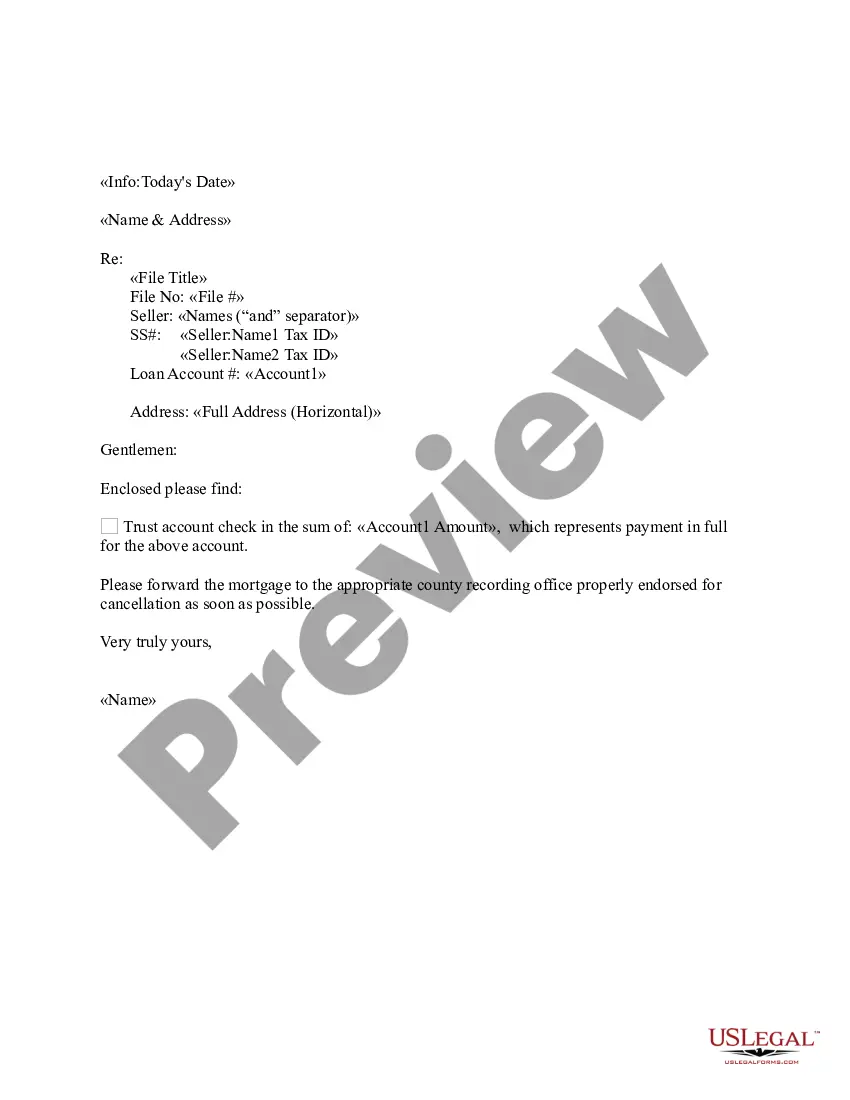

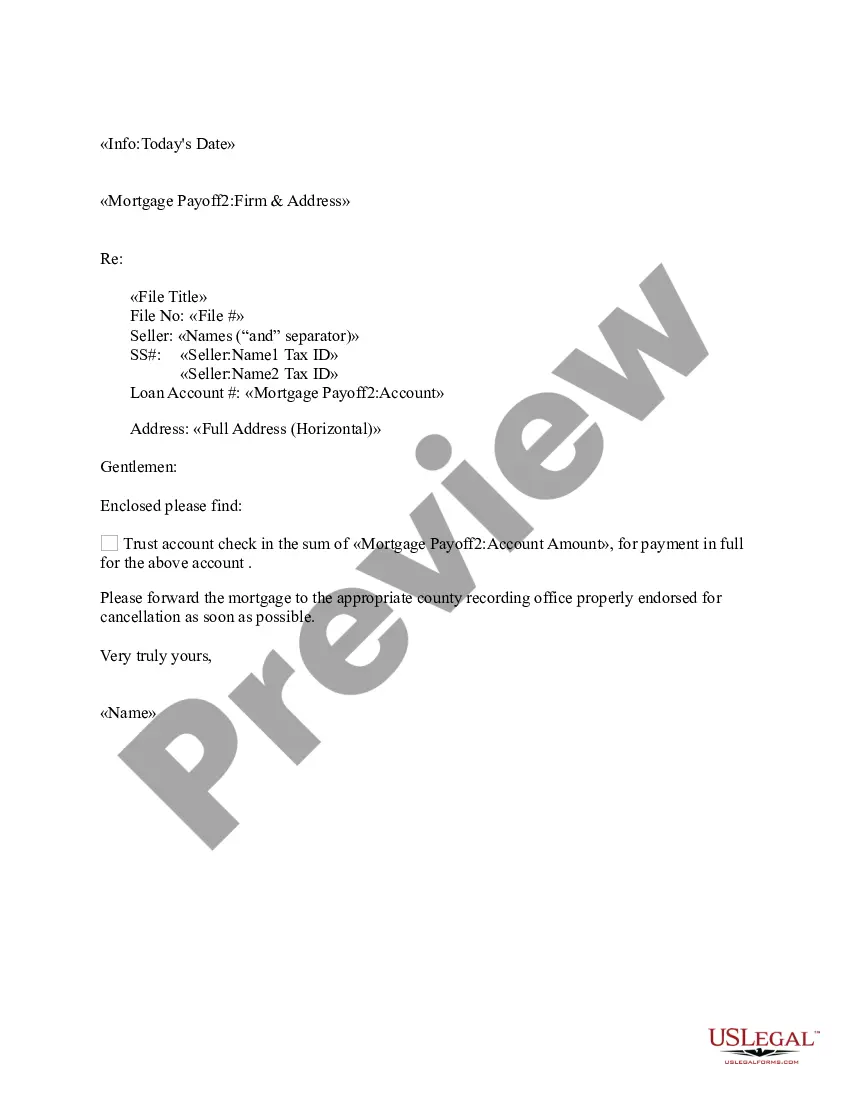

This Sample Letter for Payoff of Loan held by Mortgage Company serves as a template for individuals looking to formally request the payoff amount of their mortgage. This letter is useful for effective communication with your mortgage lender, ensuring that you have all necessary information organized and conveyed clearly. Unlike other financial correspondence, this letter specifically addresses the final mortgage payment request, setting it apart in purpose and structure.

Key components of this form

- Date: The date when the letter is written.

- Borrower's Name: The name of the individual or entity requesting the payoff.

- Property Address: The address of the property associated with the mortgage.

- Loan Reference Number: A unique identifier for the loan being paid off.

- Request for Payoff Amount: A clear statement requesting the total amount needed to fulfill the loan.

When to use this form

This form should be used when you are ready to pay off your mortgage and need to request the total remaining balance from your mortgage company. It is essential to use this letter when you are either refinancing, selling the property, or simply want to settle your mortgage completely. By formally requesting the payoff amount, you ensure that you receive an accurate and timely response from the mortgage lender.

Who should use this form

- Homeowners looking to pay off their mortgage.

- Individuals selling their property and needing to provide payoff details to buyers.

- Borrowers refinancing their current mortgage with a new lender.

- Real estate professionals assisting clients in mortgage payoff procedures.

Instructions for completing this form

- Identify the date of the letter to ensure proper timing of your request.

- Enter your full name as the borrower to establish your identity.

- Provide the complete address of the property connected to the mortgage.

- Include the loan reference number to help the lender quickly find your account.

- Clearly state your request for the total payoff amount to ensure there is no ambiguity.

Is notarization required?

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Neglecting to include the loan reference number, which can delay processing.

- Failing to specify the property address correctly.

- Not providing a clear request for the payoff amount, leading to potential misunderstandings.

- Not signing the letter before sending it, which may render it invalid.

Benefits of completing this form online

- Convenience: Download the form anytime from any device without the need for appointments.

- Editability: Customize the sample letter to fit your specific needs and situation quickly.

- Reliability: Use a template drafted by licensed attorneys to ensure comprehensive coverage of legal requirements.

Looking for another form?

Form popularity

FAQ

The loan servicer generally must deliver a payoff quote within seven days of your request. Your servicer will set an expiration date for the quote, after which interest will again accrue.

A payoff statement should include the name and address of the lender preparing the statement and be addressed to the lender that requested the payoff. It also needs to include the customer's name, the loan number and the terms of the loan, including the balance and the interest rate.

A payoff statement or a mortgage payoff letter will typically show the balance you must pay in order to close your loan. It may also include additional details, such as the amount of interest that will be rebated due to prepayment, the remaining payment schedule, rate of interest, and money saved for paying early.

A creditor or servicer of a home loan shall send an accurate payoff balance within a reasonable time, but in no case more than 7 business days, after the receipt of a written request for such balance from or on behalf of the borrower.

To get a payoff letter, ask your lender for an official payoff statement. Call or write to customer service or make the request online. While logged into your account, look for options to request or calculate a payoff amount, and provide details such as your desired payoff date.

Your payoff amount is how much you will actually have to pay to satisfy the terms of your mortgage loan and completely pay off your debt. Your payoff amount is different from your current balance.Your payoff amount also includes the payment of any interest you owe through the day you intend to pay off your loan.

A payoff letter is typically requested by a borrower from its lender in connection with the repayment of the borrower's outstanding loans to the lender under a loan agreement and termination of the loan agreement and related security and guaranties.