Oklahoma Western District Bankruptcy Guide and Forms Package for Chapters 7 or 13

Overview of this form

The Oklahoma Western District Bankruptcy Guide and Forms Package is a comprehensive resource specifically designed for individuals seeking to file for Chapter 7 or Chapter 13 bankruptcy. This package includes essential forms and detailed instructions drafted by licensed attorneys, ensuring that users have the necessary guidance to navigate the bankruptcy process effectively. It distinguishes itself by catering to both liquidation and voluntary repayment, which are two contrasting approaches to managing debts through bankruptcy.

Form components explained

- Instructions for filing Chapter 7 or Chapter 13 bankruptcy.

- Chapter 7 Statement of Your Current Monthly Income (Official Form 122A-1).

- Chapter 7 Means Test Calculation (Official Form 122A-2).

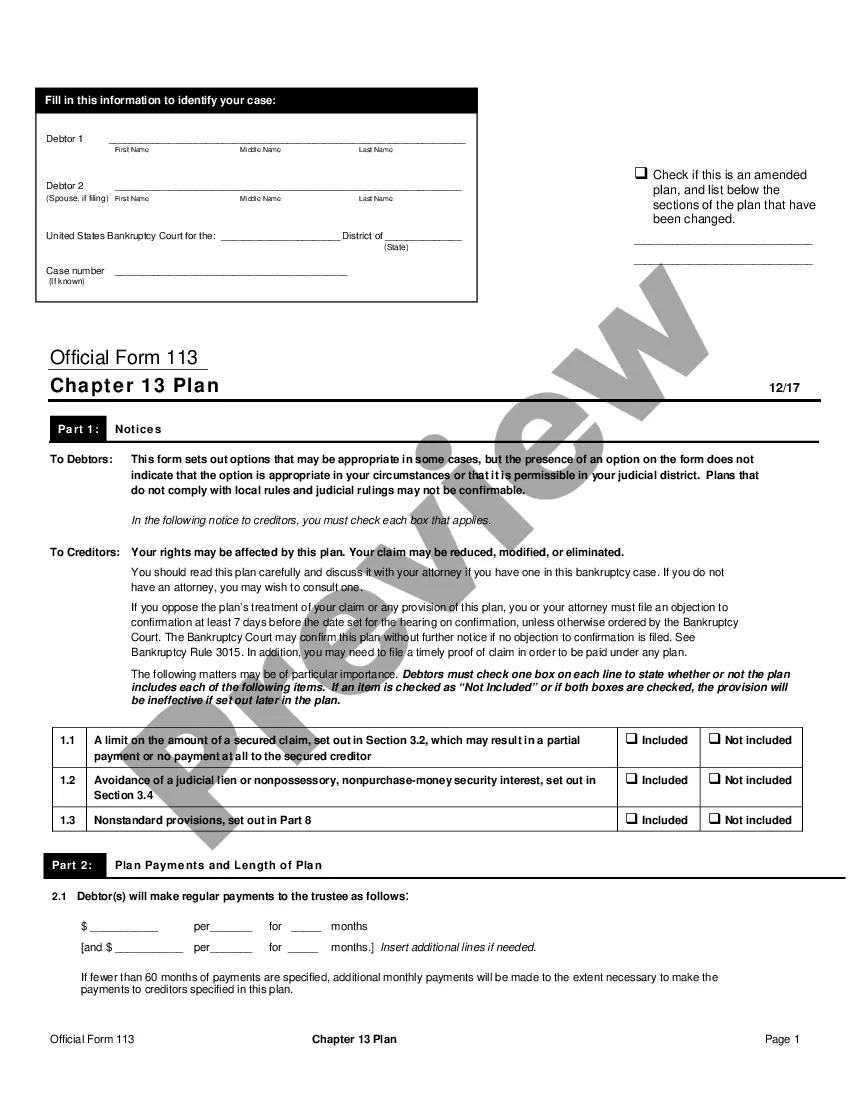

- Chapter 13 plan template for repayment of debts.

- Exempt property identification forms (Schedule C - Official Form 106C).

Common use cases

This form package is typically used when an individual is experiencing financial difficulties and is considering filing for bankruptcy. If you have debts that you cannot repay, opting for Chapter 7 provides a path to debt discharge by liquidating non-exempt assets. Alternatively, Chapter 13 is suitable if you have a regular income and wish to repay your debts over time while retaining your assets.

Who should use this form

- Individuals facing significant financial difficulties.

- Married couples who want to file jointly.

- Sole proprietors looking to discharge business-related debts.

- Those who prefer structured payment plans to manage debt.

- Individuals seeking to understand their options prior to the bankruptcy filing.

Completing this form step by step

- Gather all financial documents, including income statements and lists of debts.

- Choose the appropriate bankruptcy chapter (Chapter 7 or Chapter 13) based on your financial situation.

- Fill out the Chapter 7 Statement of Your Current Monthly Income (Official Form 122A-1) if applicable.

- Complete the necessary forms concerning exempt property, such as Schedule C (Official Form 106C).

- Submit the completed forms and any required fees to the bankruptcy court.

Notarization requirements for this form

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to disclose all debts or providing inaccurate financial information.

- Choosing the incorrect chapter of bankruptcy based on personal circumstances.

- Not filling out the means test accurately, leading to potential dismissal of the case.

- Neglecting to list all exempt properties, which can result in asset loss.

Benefits of using this form online

- Convenience of downloading forms anytime from anywhere.

- Editable templates that can be customized to fit individual needs.

- Access to updated legal information and resources tailored to bankruptcy filings.

Looking for another form?

Form popularity

FAQ

Certain family and household expenses might help you pass the means test for Chapter 7 bankruptcy. If your income is higher than your state's median income for a similar size household, you must complete the entire bankruptcy means test form to determine whether you qualify for Chapter 7 bankruptcy.

Even if you make too much money to automatically pass the Chapter 7 means test, you may still be able to qualify for Chapter 7 bankruptcy. This is because you can deduct certain expenses in full to help you reduce your disposable income on the means test.

To pass the means test, you must have little or no disposable income. The means test compares your average monthly income for the six months preceding your bankruptcy against the median income of a similar household in your state. If your income is below the median, you automatically qualify.

Alimony and child support. Certain unpaid taxes, such as tax liens. Debts for willful and malicious injury to another person or property. Debts for death or personal injury caused by the debtor's operation of a motor vehicle while intoxicated from alcohol or other substances.

If your annual income, as calculated on line 12b, is less than $84,952, you may qualify to file Chapter 7 bankruptcy. If it's greater than $84,952, you'll have to continue to Form 122A-2, which we'll review in the next section. It should be noted that every state has different median income calculations.

The means test was designed to limit the use of Chapter 7 bankruptcy to those who can't pay their debts. It does this by deducting specific monthly expenses from your "current monthly income" (your average income over the six calendar months before you file for bankruptcy) to arrive at your monthly "disposable income."

Even if you make too much money to automatically pass the Chapter 7 means test, you may still be able to qualify for Chapter 7 bankruptcy. This is because you can deduct certain expenses in full to help you reduce your disposable income on the means test.

A Chapter 7 bankruptcy will generally discharge your unsecured debts, such as credit card debt, medical bills and unsecured personal loans. The court will discharge these debts at the end of the process, generally about four to six months after you start.

Bankruptcy and Foreclosure While filing for Chapter 7 bankruptcy can stall the foreclosure process during the bankruptcy proceedings, which usually takes about four months, mortgage lenders can ask the court to lift the bankruptcy stay so that the lender can proceed with the foreclosure.