New Jersey Complaint for Breach of Promissory Note

Understanding this form

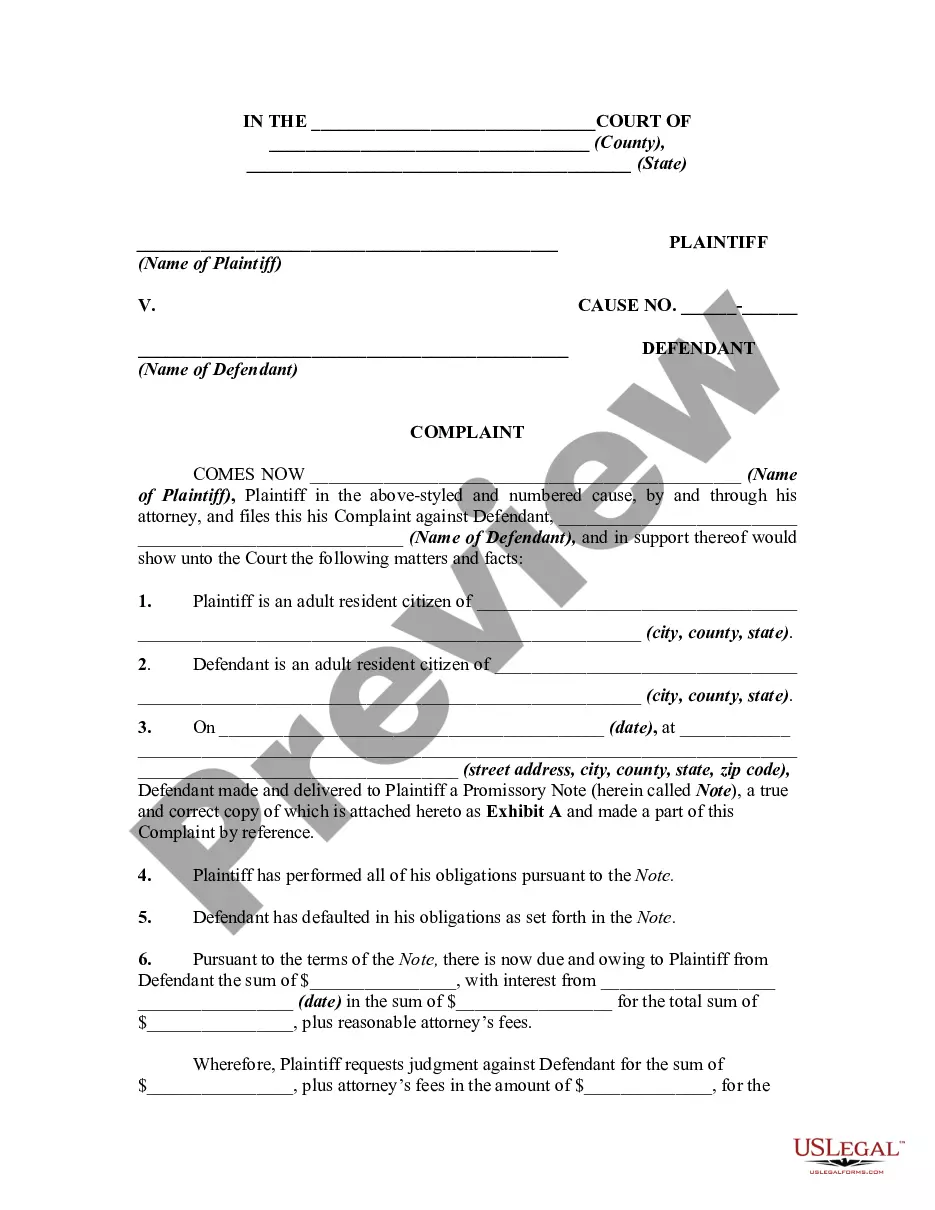

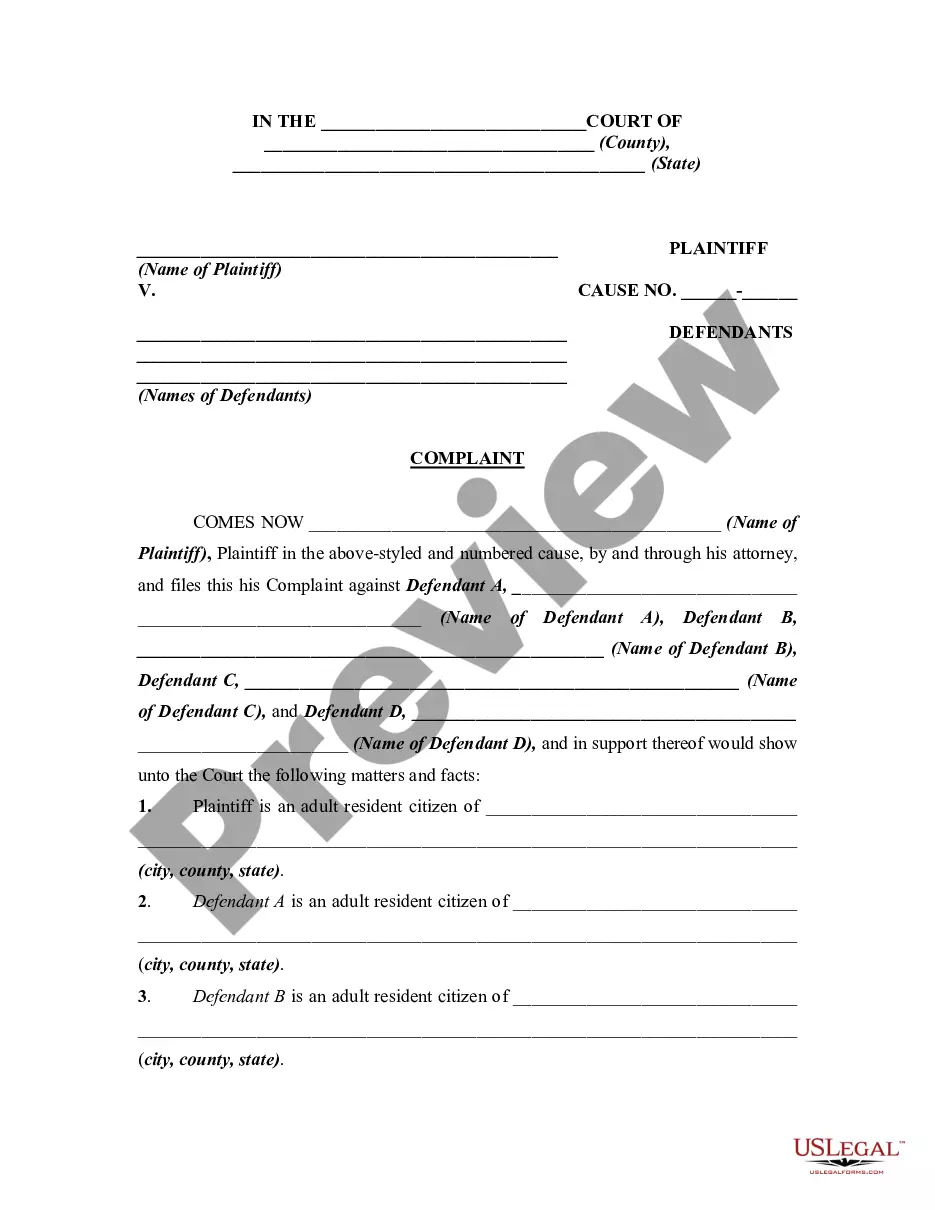

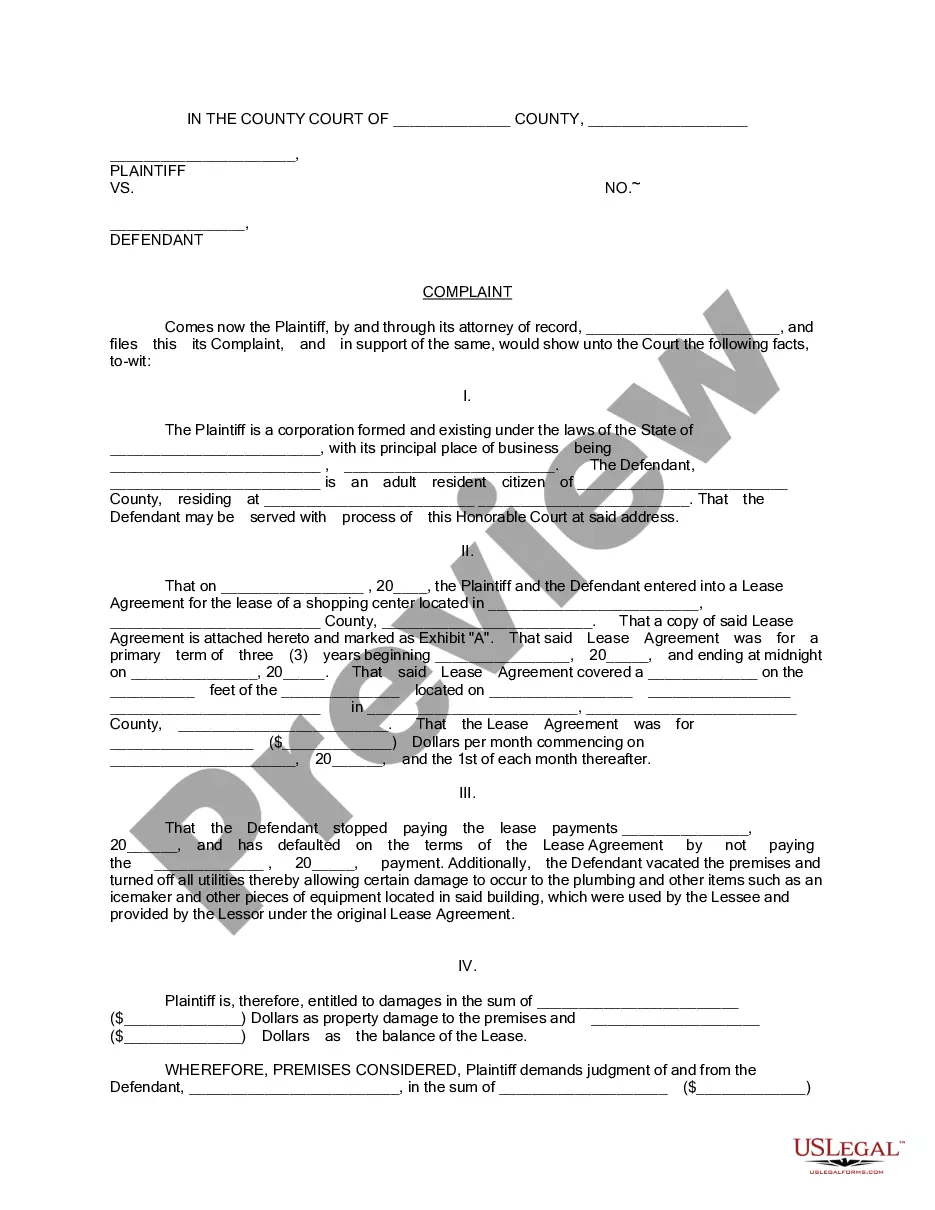

The Complaint for Breach of Promissory Note is a legal document used to initiate a lawsuit when one party (the plaintiff) believes another party (the defendant) has failed to uphold the terms of a promissory note. This form is essential for ensuring that the plaintiff can seek legal remedy for unpaid debts, distinguishing itself from other legal forms by specifically addressing breaches related to promissory notes.

Main sections of this form

- Identification of the plaintiff and defendant, including their addresses and corporate statuses.

- Details regarding the promissory notes, including amounts, payment terms, and default specifics.

- Allegations of breach and the damages incurred due to non-payment.

- Request for judgment, outlining what the plaintiff seeks from the defendant.

- Demand for a jury trial if applicable.

- Certification that no other actions regarding the dispute are pending.

When this form is needed

This form should be used when a lender wishes to take legal action against a borrower who has failed to make payments on a promissory note. Common situations include disputes over unpaid principal and interest, failure to make balloon payments, or when the terms of a security agreement linked to the promissory note are not honored. It is a vital tool for creditors seeking to recover funds legally.

Who can use this document

- Businesses or individuals who have lent money documented by a promissory note.

- Creditors seeking legal recourse when a borrower defaults on payment terms.

- Attorneys representing plaintiffs in breach of contract cases involving promissory notes.

How to complete this form

- Identify the parties involved, including their full names, addresses, and corporate statuses.

- Enter the specific details of the promissory note, including the original amounts, payment schedules, and any missed payments.

- Document the circumstances of the breach clearly, including dates and amount due.

- Specify the relief sought from the court, including any interest, costs, and attorneys' fees.

- Sign the document and include the date of signing.

Does this document require notarization?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include all relevant parties in the complaint.

- Not specifying the correct amounts due or the terms of the promissory note.

- Omitting important dates, such as the date of default or payments made.

- Filing in the wrong jurisdiction or court.

Why use this form online

- Convenience of accessing and downloading the form at any time.

- Editability to customize the document to fit specific needs.

- Reliability, as the form is drafted by licensed attorneys ensuring legal compliance.

Looking for another form?

Form popularity

FAQ

This form is used to start a civil action when a borrower fails to pay under a promissory note. It identifies the plaintiff and defendant, sets out the note’s terms and default, alleges breach and damages, and requests judgment. It may also include a jury-trial demand and a certification that no other actions are pending.

To enforce it, file the Complaint for Breach of Promissory Note in the proper New Jersey court, reference the promissory note, and identify the parties and default. The form requires detailing the note terms, the breach, and the damages, then requests judgment and may include a jury trial.

In New Jersey, the statute of limitations for breach of a written contract like a promissory note generally runs from the date of breach and can depend on circumstances; consult a licensed attorney to determine the exact period for your case.

When a breach is alleged, the form supports outlining the breach, the damages, the amount due, and the request for judgment. It also covers damages such as principal, interest, and costs, and may reserve a jury trial unless waived by the plaintiff.

Yes, a promissory note is generally enforceable if it is valid, properly executed, and not void or obtained by fraud. This form helps establish those elements by detailing the note's terms, the default, and the resulting damages, guiding the court to enforce payment.

This form focuses on a promissory note specifically, requiring identification of the note terms, the note's default, and damages tied to repayment. It includes sections for terms unique to notes, such as interest and payment obligations, and a jury-trial demand tailored to debt enforcement.