Chandler Arizona Survey Affidavit- Refinance

Category:

State:

Multi-State

City:

Chandler

Control #:

US-S058ST

Format:

Word;

Rich Text

Instant download

Description

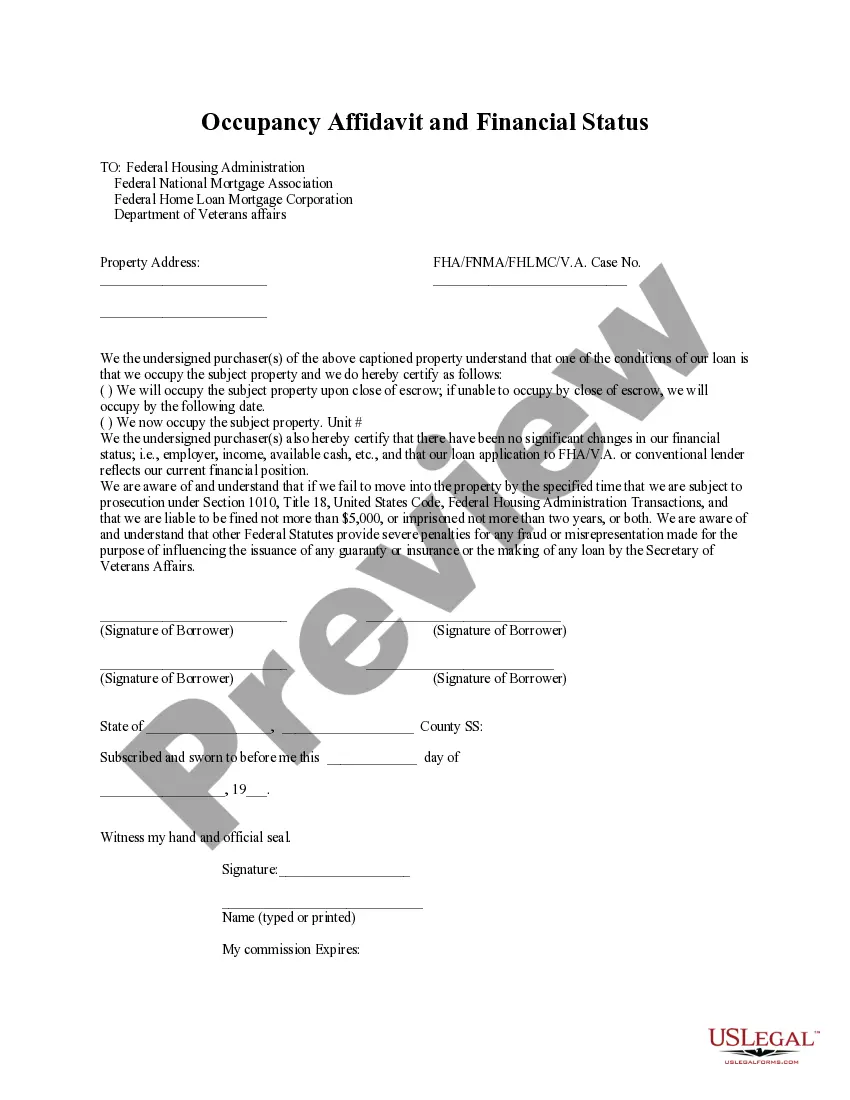

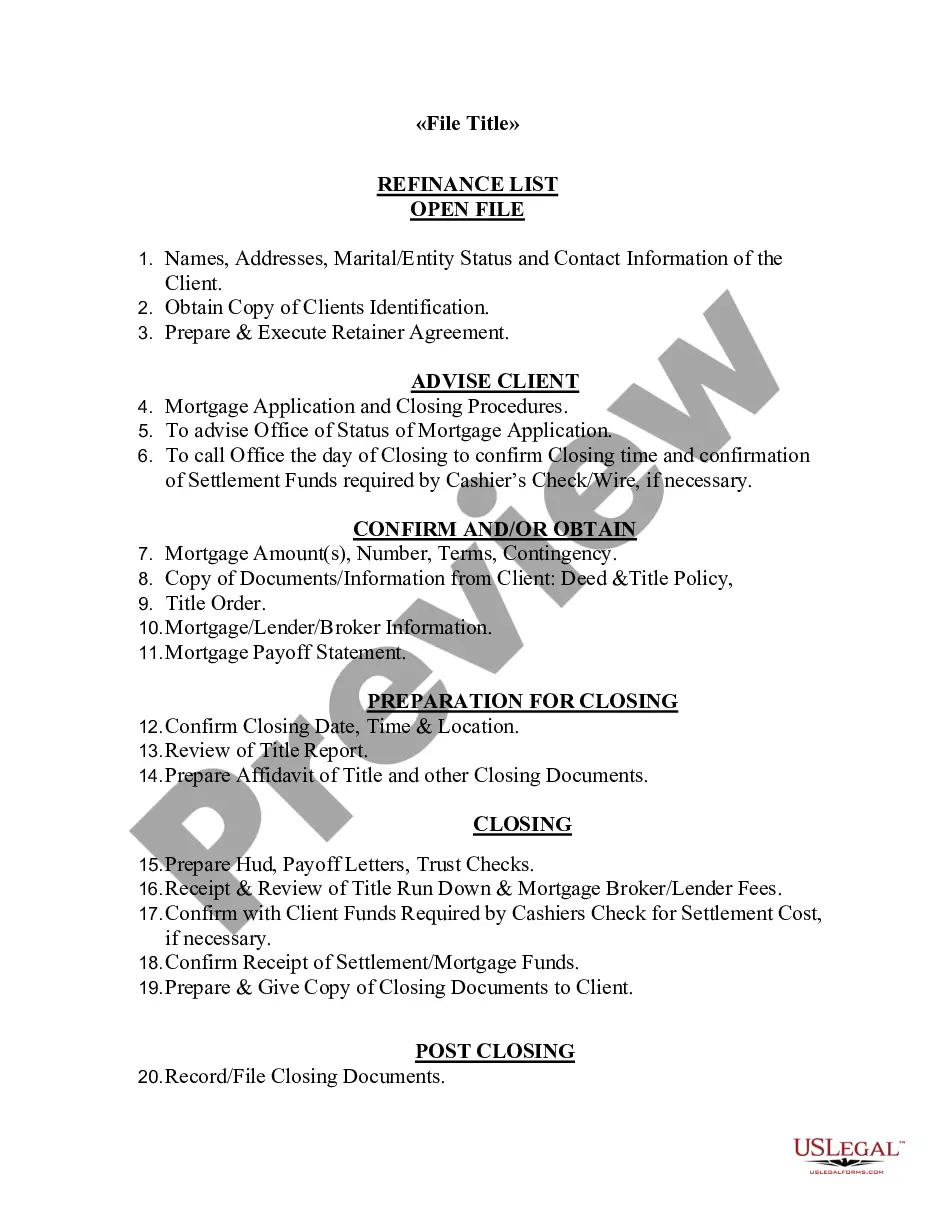

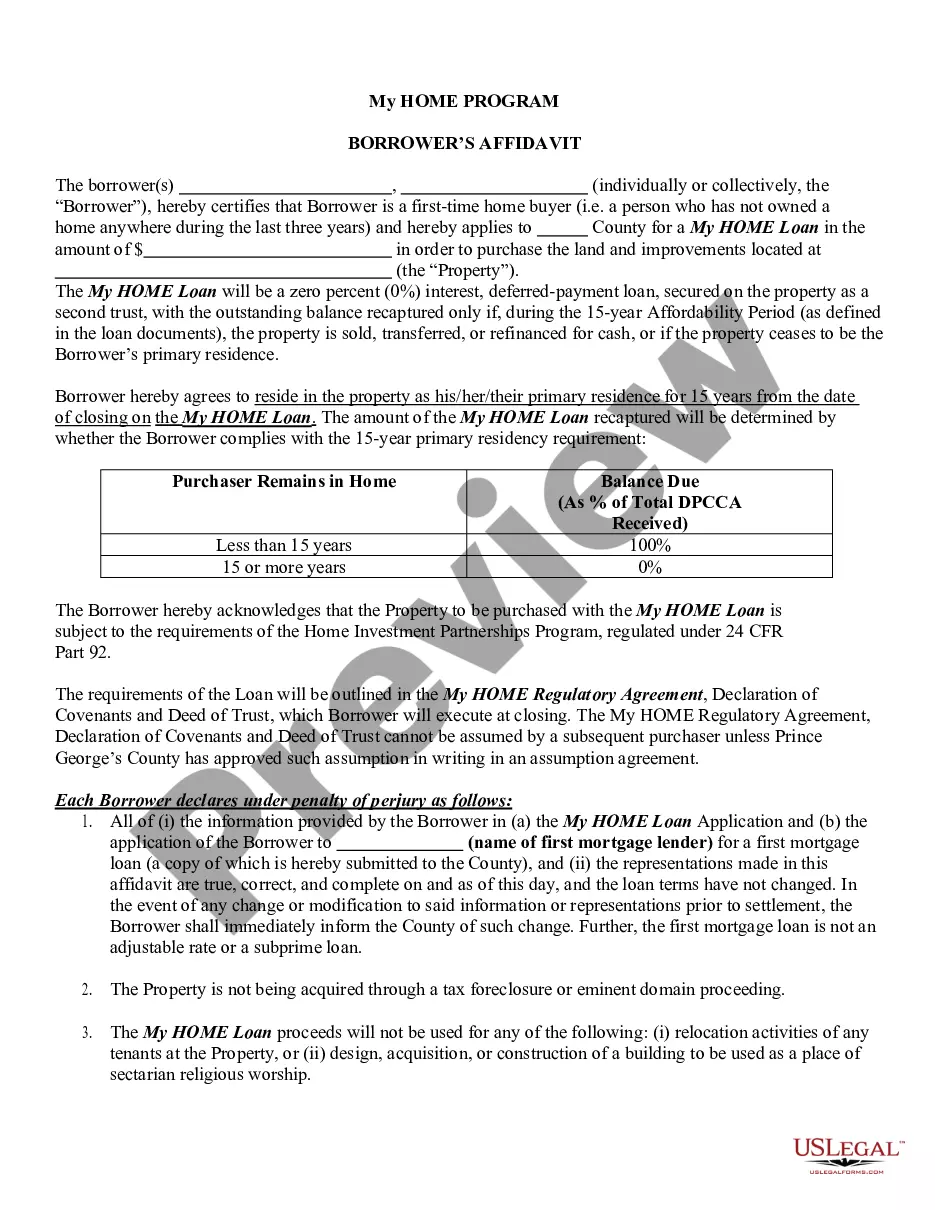

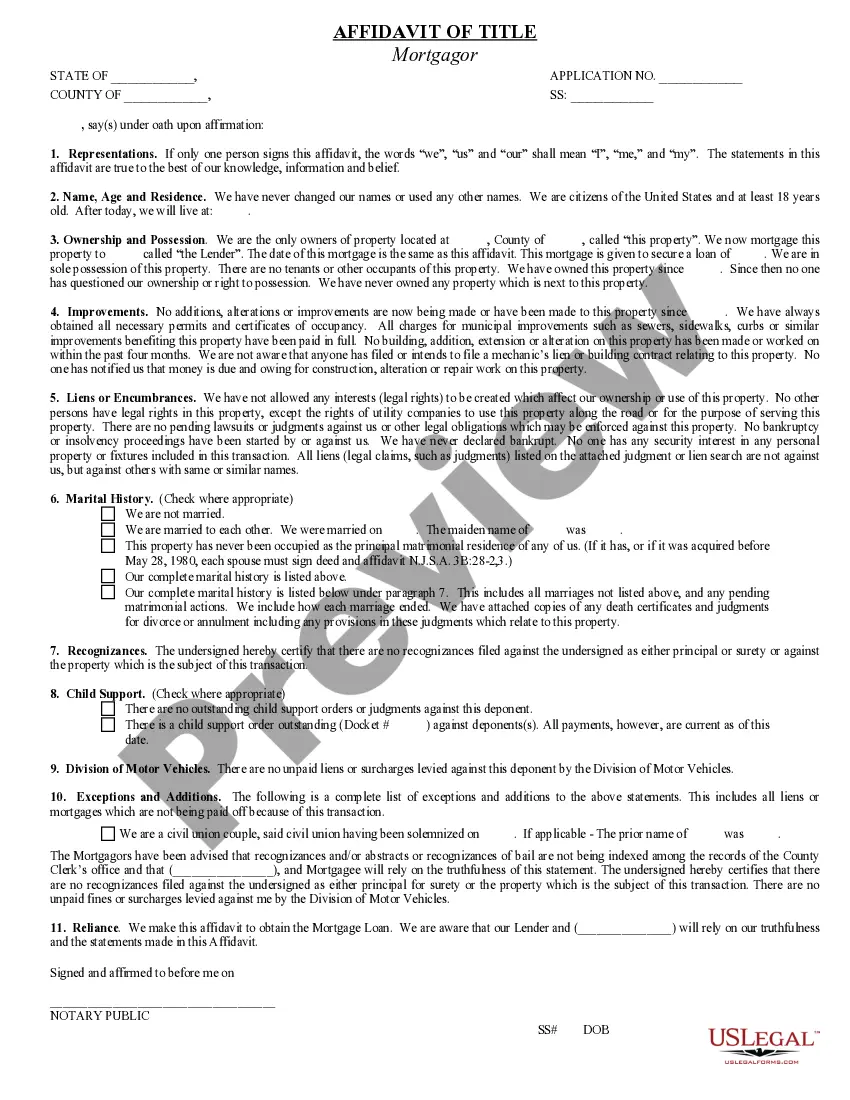

The affiant confirms the owner of property and title ownership history along with the contents of a survey conducted on the subject property.

Free preview