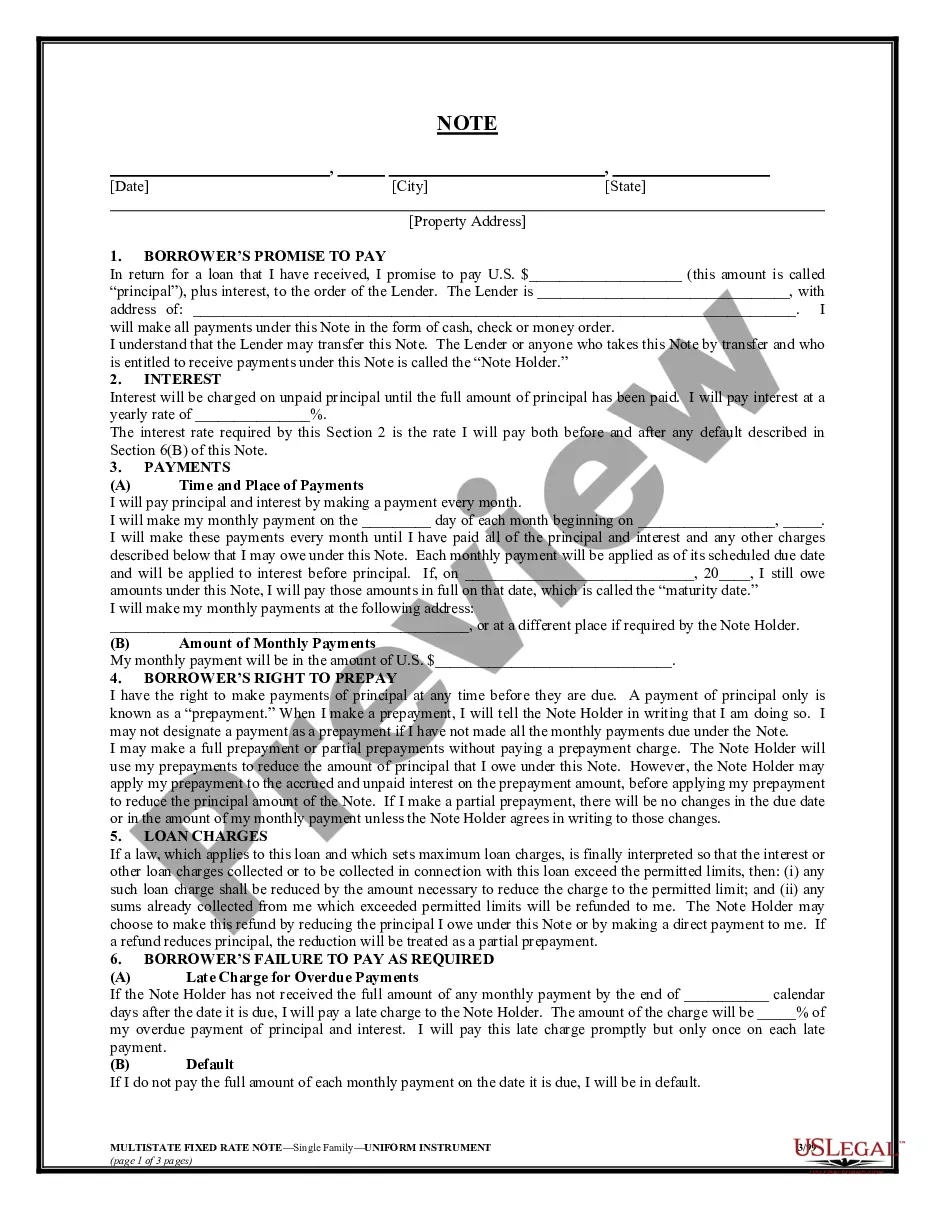

This form is a Promissory Note with Confessed Judgment Provisions. The maker of the note promises to repay a loan received from the lender, with interest. The form provides that if the maker defaults upon the loan, the lender may exercise the option of demanding the immediate payment of the entire loan.

Orlando Florida Promissory Note with Confessed Judgment Provisions

Category:

State:

Multi-State

City:

Orlando

Control #:

US-NOTE88

Format:

Word;

Rich Text

Instant download