The Fair Credit Reporting Act (FCRA),15 U.S.C. 1681-1681y, requires that this notice be

provided to inform users of consumer reports of their legal obligations. The first section of this summary sets forth the responsibilities imposed by the FCRA on all users of consumer reports. The subsequent sections discuss the duties of users of reports that contain specific types of information, or that are used for certain purposes, and the legal consequences of violations.

Wake North Carolina Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA

Category:

State:

Multi-State

County:

Wake

Control #:

US-FCRA-06

Format:

PDF

Instant download

Description

Free preview

How to fill out Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA?

Drafting legal documents is essential in the modern era.

However, you don't always need to seek professional help to generate some of them from scratch, such as Wake Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA, utilizing a service like US Legal Forms.

US Legal Forms presents over 85,000 templates to choose from across various categories ranging from living wills to property paperwork to divorce forms.

If you are already a subscriber of US Legal Forms, you can find the relevant Wake Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA, Log In to your account, and download it.

Clearly, our platform cannot entirely replace an attorney. If you're faced with an especially complex situation, we suggest employing a lawyer's services to review your document before signing and filing it.

- Review the document's preview and outline (if provided) for a general understanding of what you'll receive post-download.

- Confirm that the template you select is tailored to your state/county/region, as state regulations may influence the validity of certain documents.

- Inspect the associated document templates or restart your search to find the appropriate file.

- Click Buy now and create your account. If you already possess one, opt to Log In.

- Select the option, then a suitable payment method, and acquire Wake Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA.

- Opt to save the document template in any available format.

- Navigate to the My documents section to re-download the document.

Form popularity

FAQ

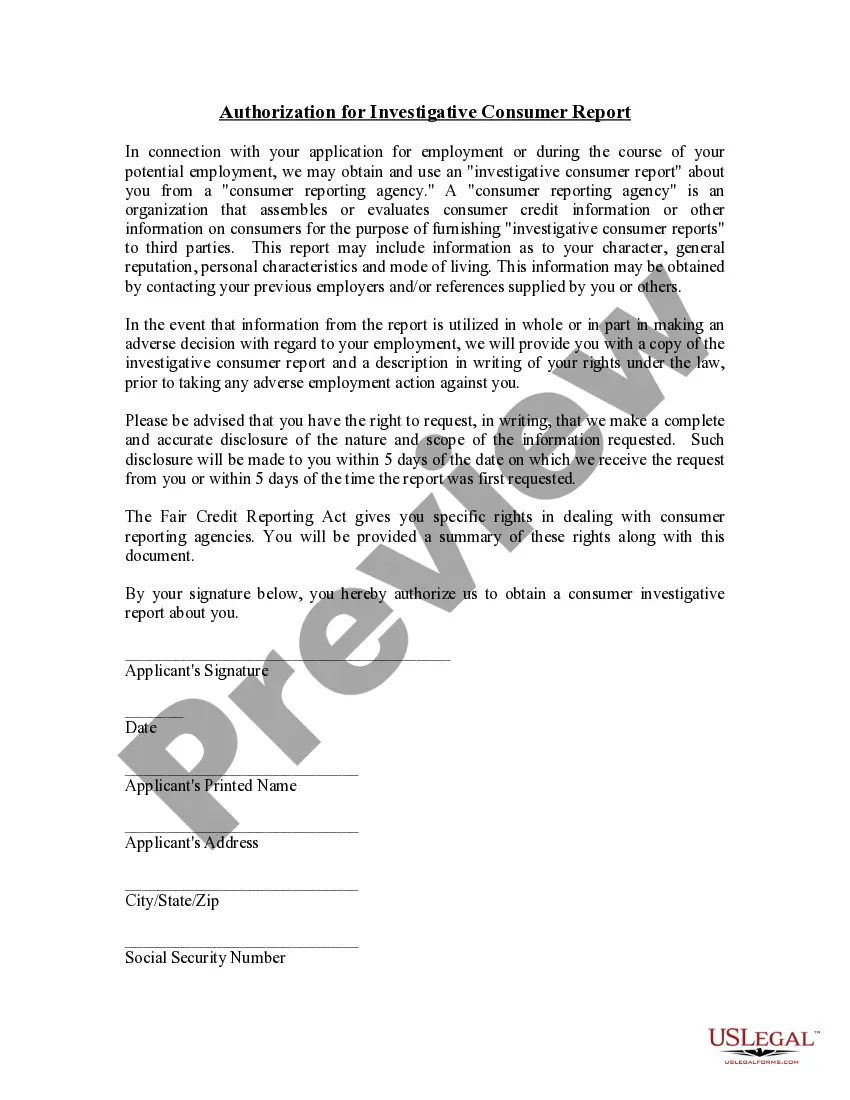

Under the FCRA, if a user takes any adverse action based on information obtained from a consumer report, they must inform the consumer about the action. This includes providing the name and contact information of the consumer reporting agency that supplied the report, as well as a statement that the agency did not make the decision. It's essential to ensure compliance with the Wake North Carolina Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA.

The disclosure requirements are triggered when a credit score is used by a person in taking adverse action. Some violations have occurred when persons interpreted the term use too narrowly to include only situations when adverse action is solely or primarily based on the credit score.

The FCRA requires any prospective user of a consumer report, for example, a lender, insurer, landlord, or employer, among others, to have a legally permissible purpose to obtain a report.

Thus, under the FCRA, certain consumer information will be subject to two opt-out notices, a sharing opt-out notice (Section 603(d)) and a marketing use opt-out notice (Section 624). These two opt-out notices may be consolidated.

It must include information about the credit bureau used, an explanation of the specific reasons for the adverse action, a notice of the consumer's right to a free credit report and to dispute its accuracy and the consumer's credit score.

Notice violations under the FCRA might occur when: a creditor fails to notify you when it supplies negative credit information to a CRA. a user of credit information (such as a prospective employer or lender) fails to notify you of a negative decision based upon your credit report.

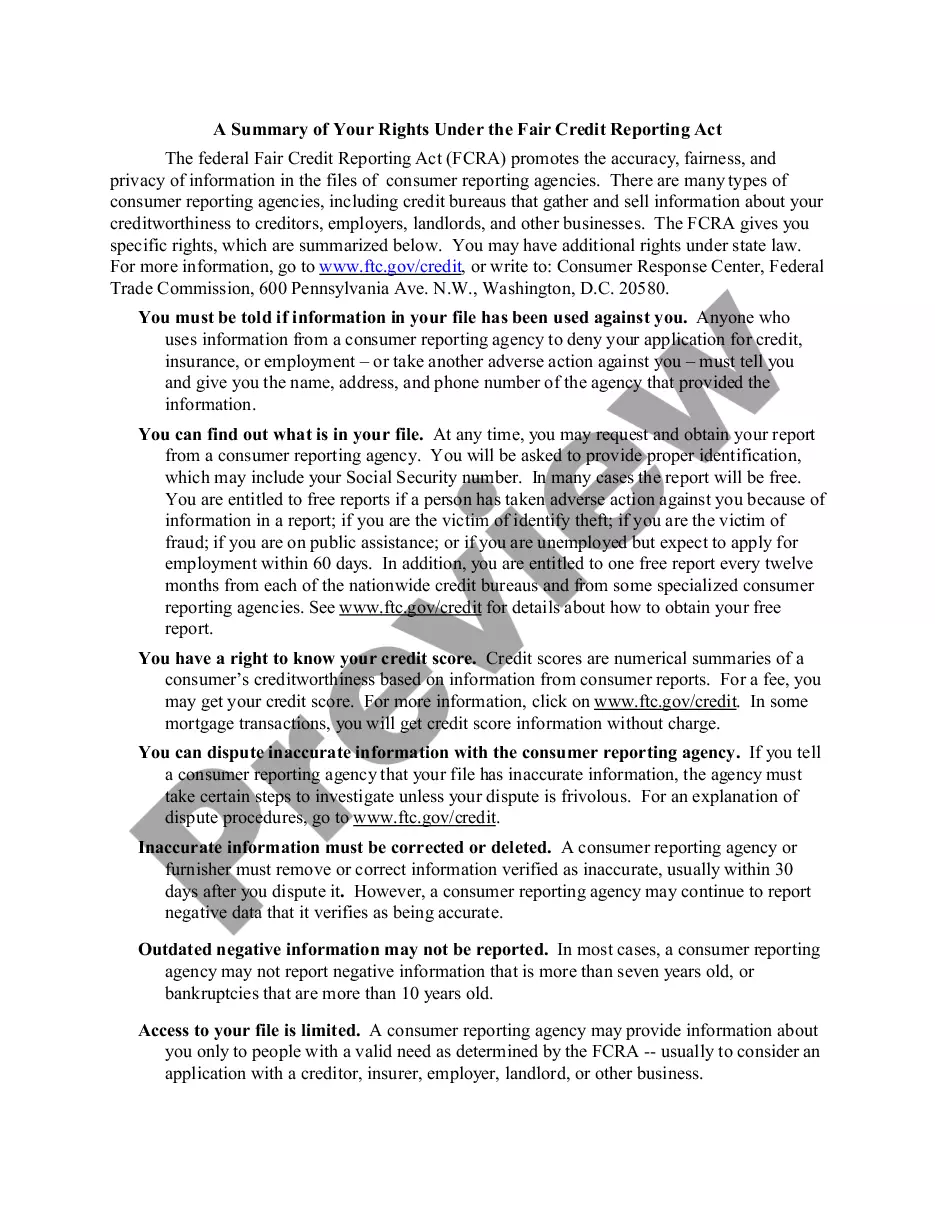

The primary law is the Fair Credit Reporting Act (FCRA). Among other things, the FCRA limits who can access your credit reports and for what purposes. Here are some of the rights provided to consumers under the FCRA: 1. Credit bureaus must provide your credit report to you when you ask for it.

Under the FCRA, consumer reporting agencies are required to provide consumers with the information in their own file upon request, and consumer reporting agencies are not allowed to share information with third parties unless there is a permissible purpose.

If you report information about consumers to a CRA like a credit bureau, tenant screening company, check verification service, or a medical information service you have legal obligations under the FCRA's Furnisher Rule.

The FCRA is not a strict liability statute. An inaccurate consumer report therefore does not automatically result in liability. Instead, the FCRA imposes civil liability for negligent and willful failures to comply with its requirements (15 U.S.C. §§ 1681n, 1681o).