Irvine California Founders Agreement

Category:

State:

Multi-State

City:

Irvine

Control #:

US-ENTREP-0027-2

Format:

Word;

Rich Text

Instant download

Description

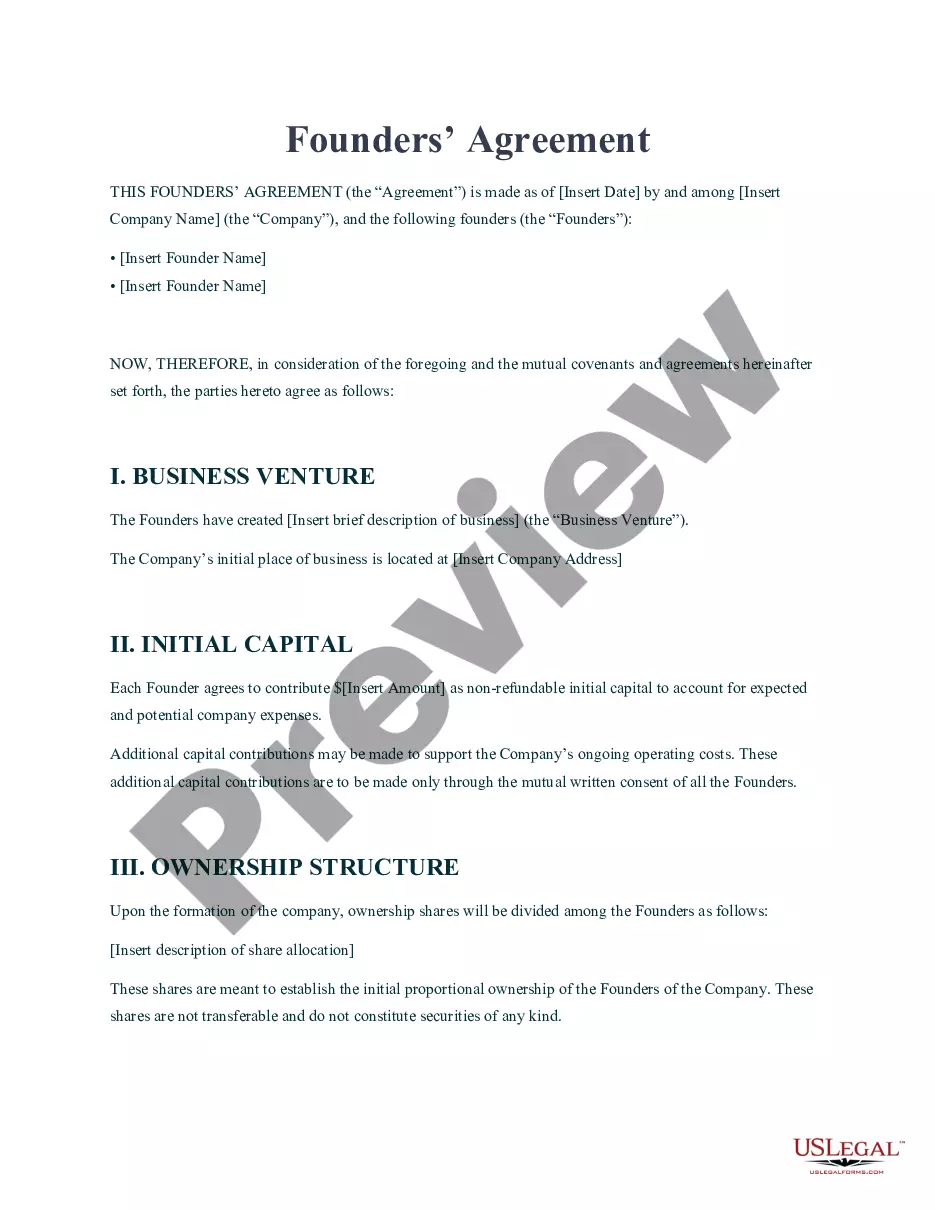

A founders' agreement is a document created by the founders of a company to establish how the company will function. It is the product of pre-incorporation discussions that should take place among the company's founders before they establish the company. It includes provisions on ownership structure, decision making, dispute resolution, choice of law, transfer of ownership, ownership percentages, voting rights, intellectual property rights, and more.

Free preview