King Washington Approval of Stock Option Plan

Description

How to fill out Approval Of Stock Option Plan?

Laws and guidelines in every domain differ across the nation.

If you are not a lawyer, it’s simple to become confused by a range of regulations when it comes to creating legal documents.

To prevent expensive legal fees when preparing the King Approval of Stock Option Plan, you require a validated template applicable to your locality.

This is the easiest and most cost-effective method to obtain current templates for any legal purposes. Locate them all in just a few clicks and maintain your documentation in order with US Legal Forms!

- Review the page content to confirm you have found the suitable sample.

- Utilize the Preview feature or read the form description if it is available.

- Look for another document if there are discrepancies with any of your parameters.

- Use the Buy Now button to acquire the template once you identify the correct one.

- Select one of the subscription options and Log In or create an account.

- Decide how you wish to pay for your subscription (with a credit card or PayPal).

- Choose the format you wish to save the file in and click Download.

- Fill out and sign the document on paper after printing it or conduct it all digitally.

Form popularity

FAQ

Long-Term Incentives (LTIs) are a form of variable compensation that is earned in the present but whose payment is deferred and spread over time. This can be cash compensation but often is in the form of stock or stock options.

LTI Eligible means a Participant who, as of the start of an Enrollment Period for an Offering Period, is eligible to receive a long-term incentive compensation award under the Rules of the Takeda Pharmaceutical Company Limited Long Term Incentive Plan or any successor plan, as determined by the Committee in its sole

Long-term incentives, or LTI as they're often called, are a valuable part of a total compensation package both for delivering rewards and focusing employees on desired future outcomes and objectives.

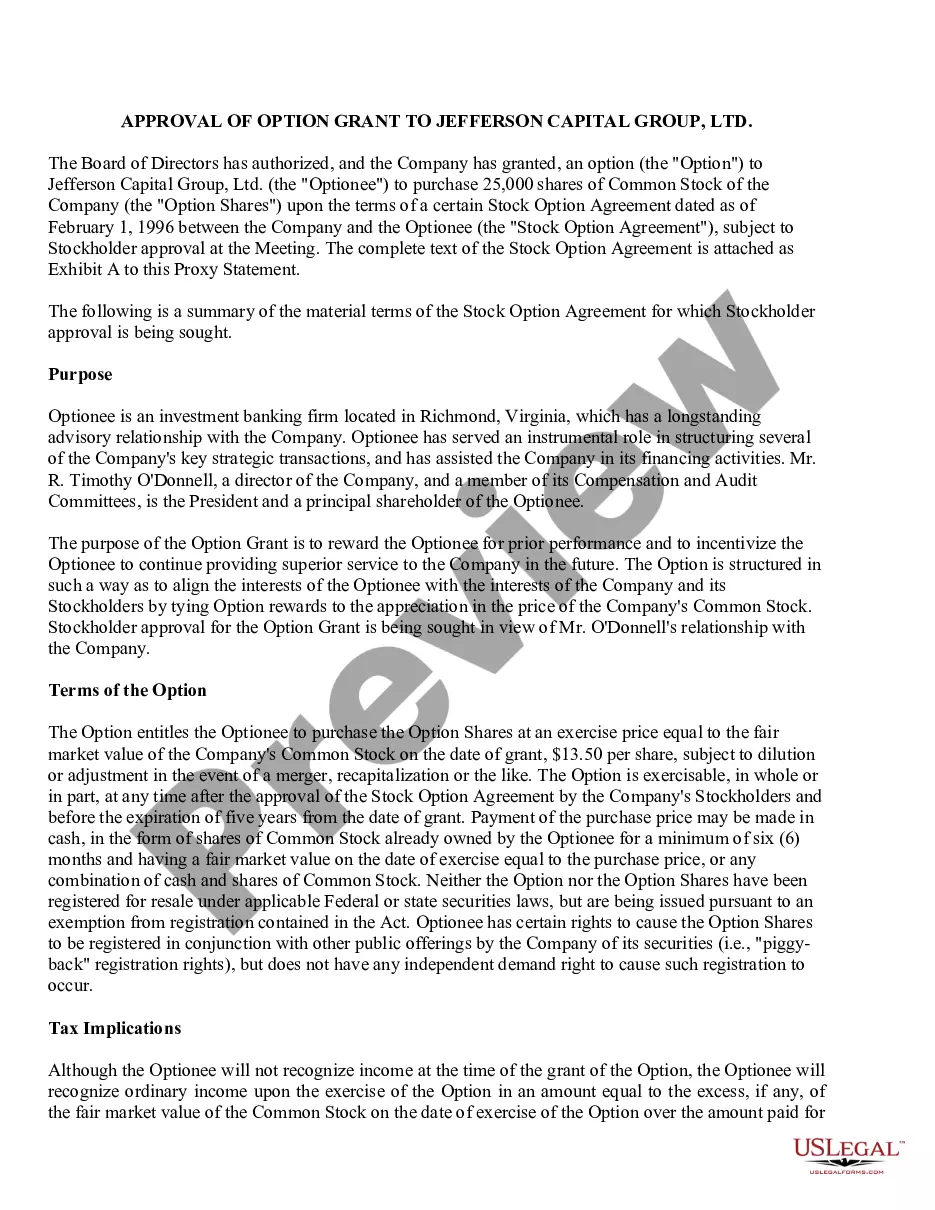

A stock option should be granted under a written stock plan that is approved by shareholders within 12 months of the date it is adopted by the company's board of directors. There are 2 types of stock options: incentive stock options (ISOs) and non-statutory stock options (NSOs).

On June 30, the SEC approved rules requiring shareholder approval of equity compensation plans, including stock option plans. The new rules will also require approval for repricings and material plan changes.

The board has to approve all stock option grants ahead of time, either at a board meeting or by unanimous written consent. If your board hasn't approved an option grant, no options have actually been granted.

Under both the NYSE and NASDAQ listing standards, a public company must obtain shareholder approval before it can issue shares under an equity incentive plan or make material revisions to an equity incentive plan.

Shareholder approval will only be required for issuances to a related party, and will not be required for issuances to 1) a subsidiary, affiliate, or other closely related person of a related party, or 2) any company or entity in which a related party has a substantial direct or indirect interest.

Long-Term Incentives (LTIs) are a form of variable compensation that is earned in the present but whose payment is deferred and spread over time. This can be cash compensation but often is in the form of stock or stock options.

On June 30, the SEC approved rules requiring shareholder approval of equity compensation plans, including stock option plans. The new rules will also require approval for repricings and material plan changes.