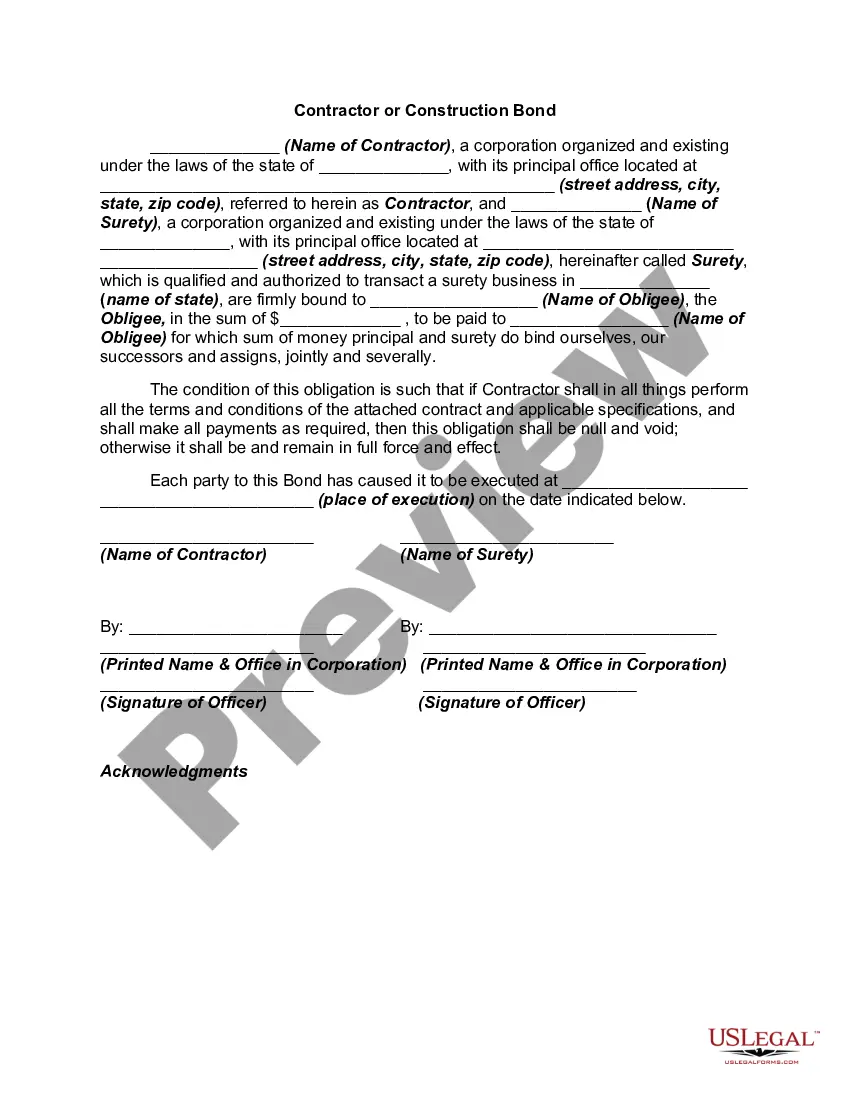

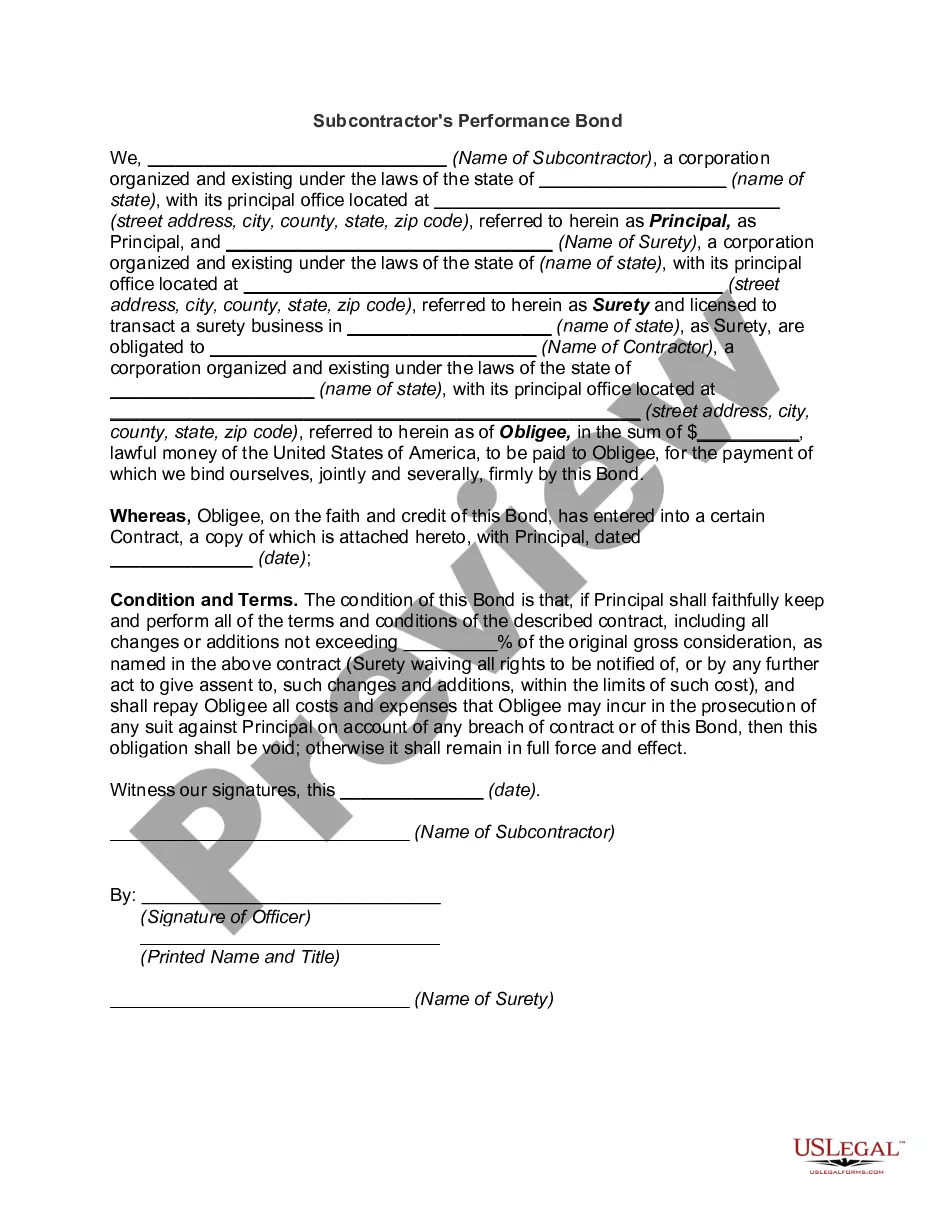

Detroit Michigan Performance Bond

Category:

State:

Multi-State

City:

Detroit

Control #:

US-1004BG

Format:

Word;

Rich Text

Instant download

Description

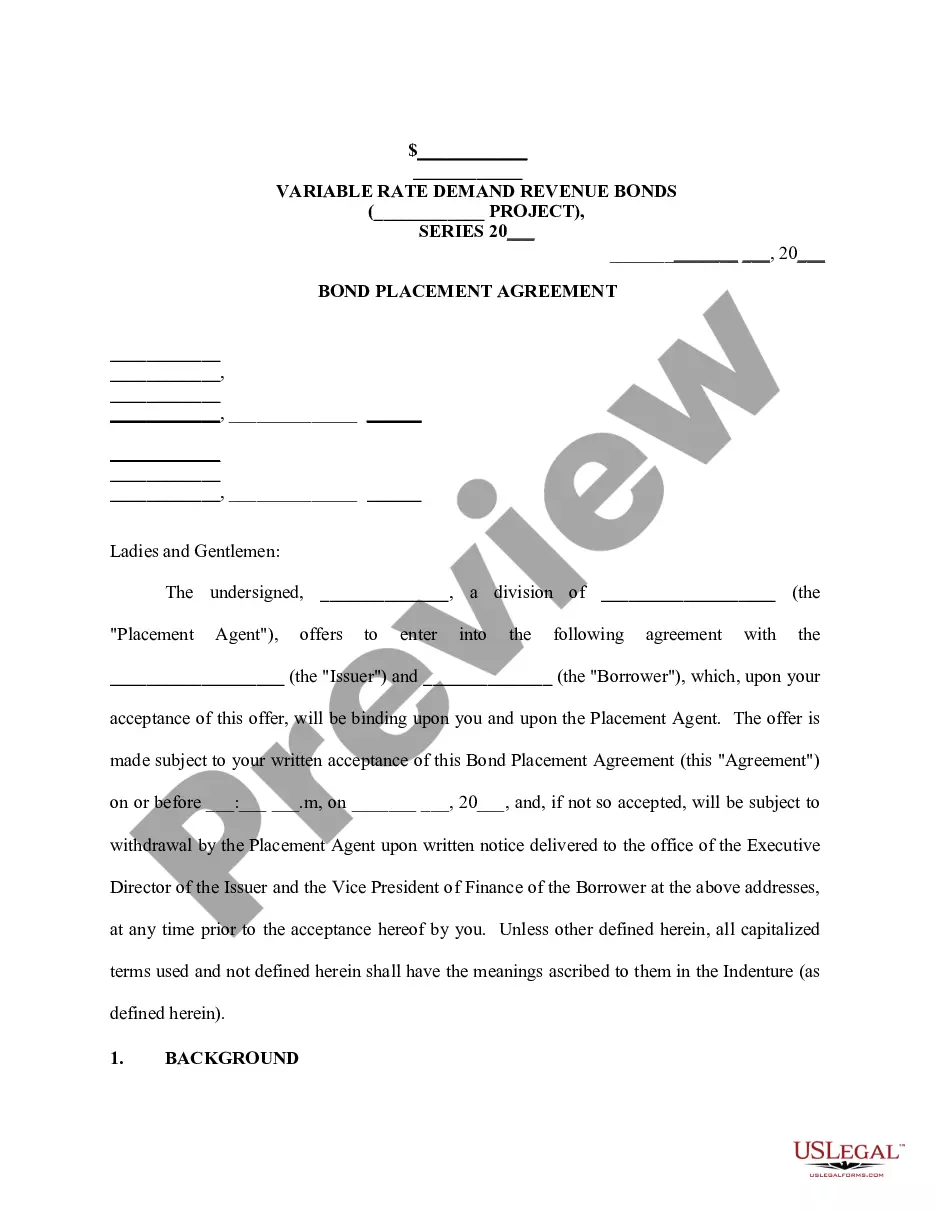

A performance bond, also known as a contract bond, is a surety bond issued by an insurance company or a bank to guarantee satisfactory completion of a project by a contractor.

Free preview