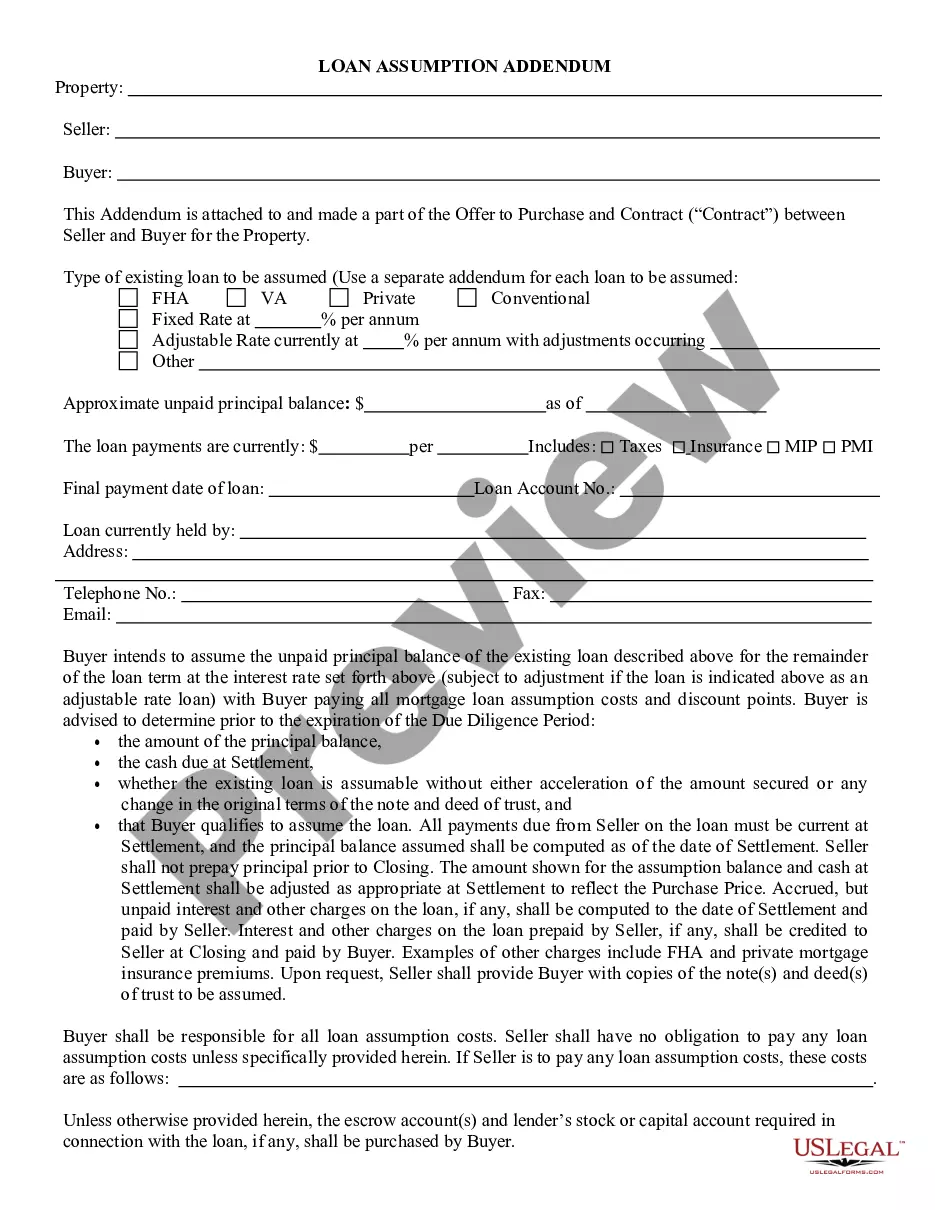

This form is an Assumption Agreement. The grantor desires to convey certain property to the grantee and the grantee agrees to assume the lien and the loan. The agreement must also be signed in the presence of a notary public.

Cook Illinois Loan Assumption Agreement

Category:

State:

Multi-State

County:

Cook

Control #:

US-00561

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Loan Assumption Agreement?

Do you need to swiftly prepare a legally-enforceable Cook Loan Assumption Agreement or perhaps any other document to manage your personal or business matters.

You have two choices: engage a specialist to create a legal document for you or compose it entirely on your own. The positive aspect is, there's an alternative option - US Legal Forms. It will assist you in obtaining expertly crafted legal documents without incurring exorbitant fees for legal assistance.

If the form isn’t what you were expecting, try the search bar in the header once more.

Choose the plan that suits your requirements best and proceed to payment. Select the file format in which you'd like to receive your document and download it. Print it out, fill it in, and sign on the specified line. If you've previously registered an account, you can effortlessly Log In, locate the Cook Loan Assumption Agreement template, and download it. To re-download the form, simply visit the My documents section. Purchasing and downloading legal forms is straightforward with our catalog. Additionally, the templates we offer are routinely updated by industry professionals, providing you with increased assurance when handling legal issues. Give US Legal Forms a try now and experience it for yourself!

- US Legal Forms offers a vast assortment of over 85,000 state-compliant form templates, including the Cook Loan Assumption Agreement and form packages.

- We provide documents for a variety of life scenarios: from divorce agreements to real estate document templates.

- Having been in the industry for more than 25 years, we have established an impeccable reputation among our clientele.

- Here's how you can join them and acquire the necessary template without additional hassle.

- Firstly, verify if the Cook Loan Assumption Agreement meets your state's or county's laws.

- If the document has a description, ensure to check what its purpose is.

Form popularity

FAQ

When a buyer assumes a loan it is with the lender's knowledge and approval. An assumption agreement is prepared by the existing lender of record and signed by the buyer as part of the escrow process.

An assumable mortgage allows a home buyer to not only move into the seller's former house but to step into the seller's loan, too. Having an assumable loan might give a seller a marketing edge, particularly if mortgage rates have risen since the seller got the loan.

It's also misguided to think a refinance will take the same amount of time as assuming a loan. A refinance typically takes about 30 days, but a loan assumption can take anywhere from three to six months, depending on the lender.

Assumable refers to when one party takes over the obligation of another. In terms of an assumable mortgage, the buyer assumes the existing mortgage of the seller. When the mortgage is assumed, the seller is often no longer responsible for the debt.

What is a mortgage assumption agreement? It's actually pretty self-explanatory. A person who assumes a mortgage takes over a payment from the previous homeowner. Basically, the agreement shifts the financial responsibility of the loan to a different borrower.

What is mortgage assumption? Mortgage assumption is the process of one borrower taking over, or assuming, another borrower's existing home loan. When you're assuming a loan, the outstanding balance, mortgage interest rate, repayment period and other terms attached to that loan often don't change.

No, all mortgages are not assumable. Conventional mortgages (those originated by lenders and then sold in the secondary mortgage investment marketplace) may be more difficult to assume, whereas FHA, VA and USDA mortgages are assumable. At this time, Rocket Mortgage® doesn't offer USDA loans.

Advantages. If the assumable interest rate is lower than current market rates, the buyer saves money straight away. There are also fewer closing costs associated with assuming a mortgage. This can save money for the seller as well as the buyer.

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability.

How much does a loan assumption cost? You'll have to pay closing costs on a loan assumption, which are typically 2-5% of the loan amount. But some of those may be capped. And you're unlikely to need a new appraisal.