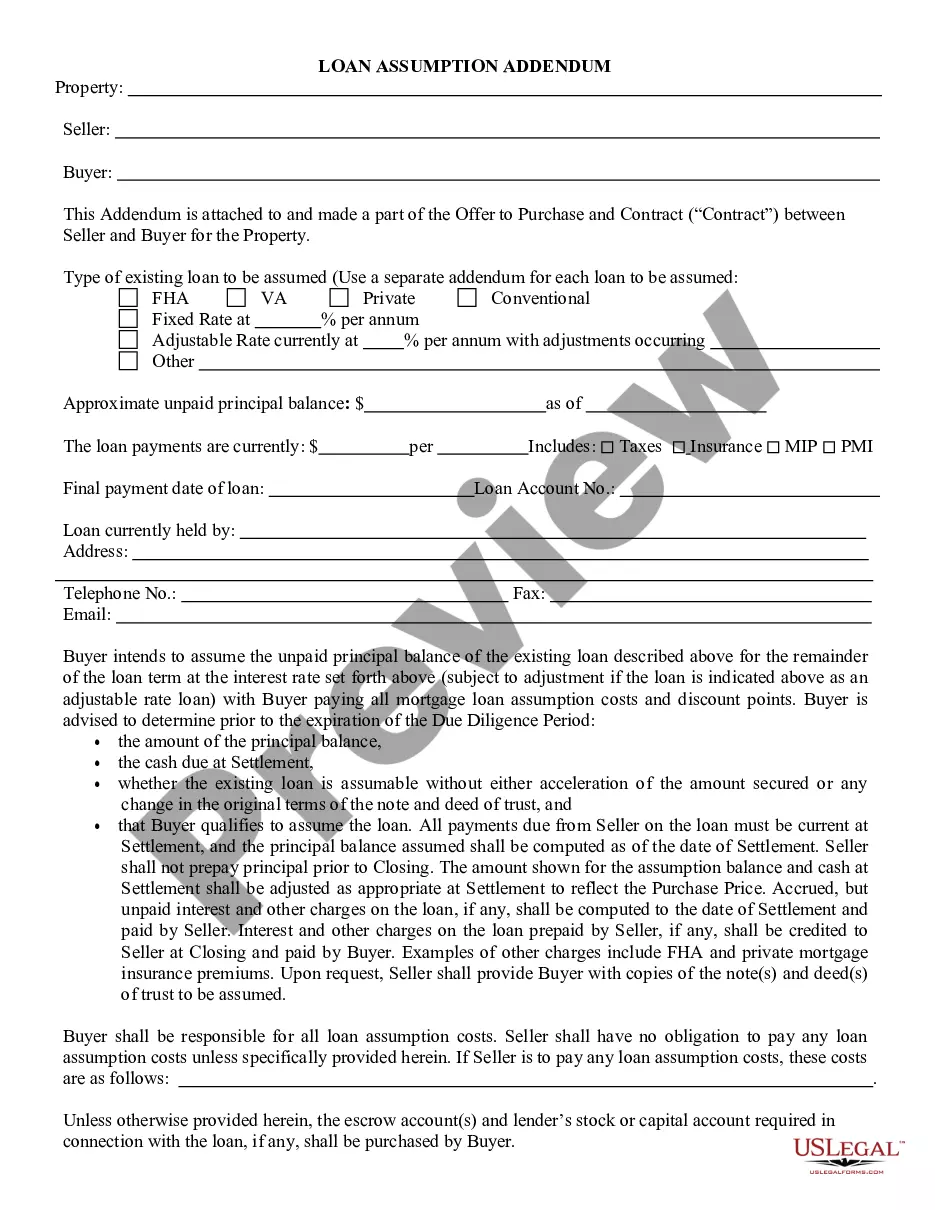

This form is an Assumption Agreement. The grantor desires to convey certain property to the grantee and the grantee agrees to assume the lien and the loan. The agreement must also be signed in the presence of a notary public.

Bakersfield California Loan Assumption Agreement

Category:

State:

Multi-State

City:

Bakersfield

Control #:

US-00561

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

The Bakersfield California Loan Assumption Agreement serves as a vital tool for transferring loan obligations from one party to another. It allows a buyer to take over an existing mortgage on a property, which can simplify the buying process. By using this agreement, you can often benefit from favorable terms that the original borrower secured. This agreement ensures that the lender approves the assumption and protects both parties involved in the transaction.

Assuming a mortgage can come with some pitfalls. One downside is that you may take on the existing mortgage's rate and terms, which might not be favorable. Additionally, in a Bakersfield California Loan Assumption Agreement, the lender may still hold the original borrower accountable for payments, creating potential complications down the line. Consider these factors carefully before deciding to assume a mortgage.

An assumption clause is a part of a loan agreement that allows a buyer to take over the seller's existing mortgage. For example, a Bakersfield California Loan Assumption Agreement may state that the borrower agrees to continue making monthly payments on the loan under the same terms. This can simplify the buying process, as the buyer does not need to secure a new mortgage. Always review this clause carefully to understand your responsibilities.

Yes, you can obtain an assumable mortgage in California. Several lenders offer loans that allow new buyers to take over existing mortgages. However, the terms of these agreements can vary, so it is essential to read the details closely. Engaging with a Bakersfield California Loan Assumption Agreement can streamline your buying experience.

Qualifying for an assumable mortgage often depends on the lender's specific criteria. Generally, you will need to demonstrate your creditworthiness and financial stability. The terms can vary by lender, so it's helpful to review the agreement carefully. If you're interested in exploring options, a Bakersfield California Loan Assumption Agreement may ease the process for you.

The alternative to an assumable mortgage typically involves refinancing your loan. In this scenario, you can secure a new mortgage that pays off your existing obligation. This process can be more complicated and may involve closing costs. If you want to avoid these challenges, consider looking into a Bakersfield California Loan Assumption Agreement.

Yes, Freddie Mac loans can be assumed under certain circumstances. A Bakersfield California Loan Assumption Agreement allows qualified borrowers to take over an existing mortgage. This process can benefit both the seller and the buyer by providing more flexible financing options. However, it’s essential to review the loan terms and consult with a knowledgeable professional to ensure compliance.