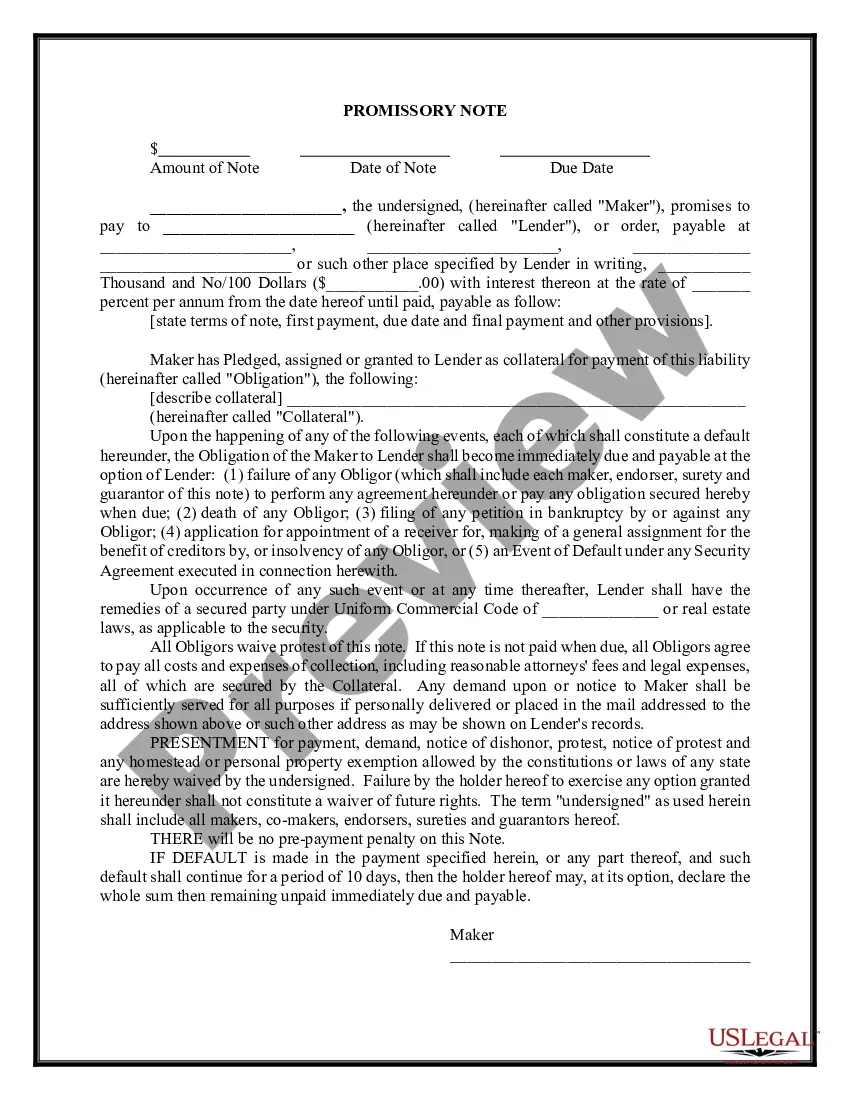

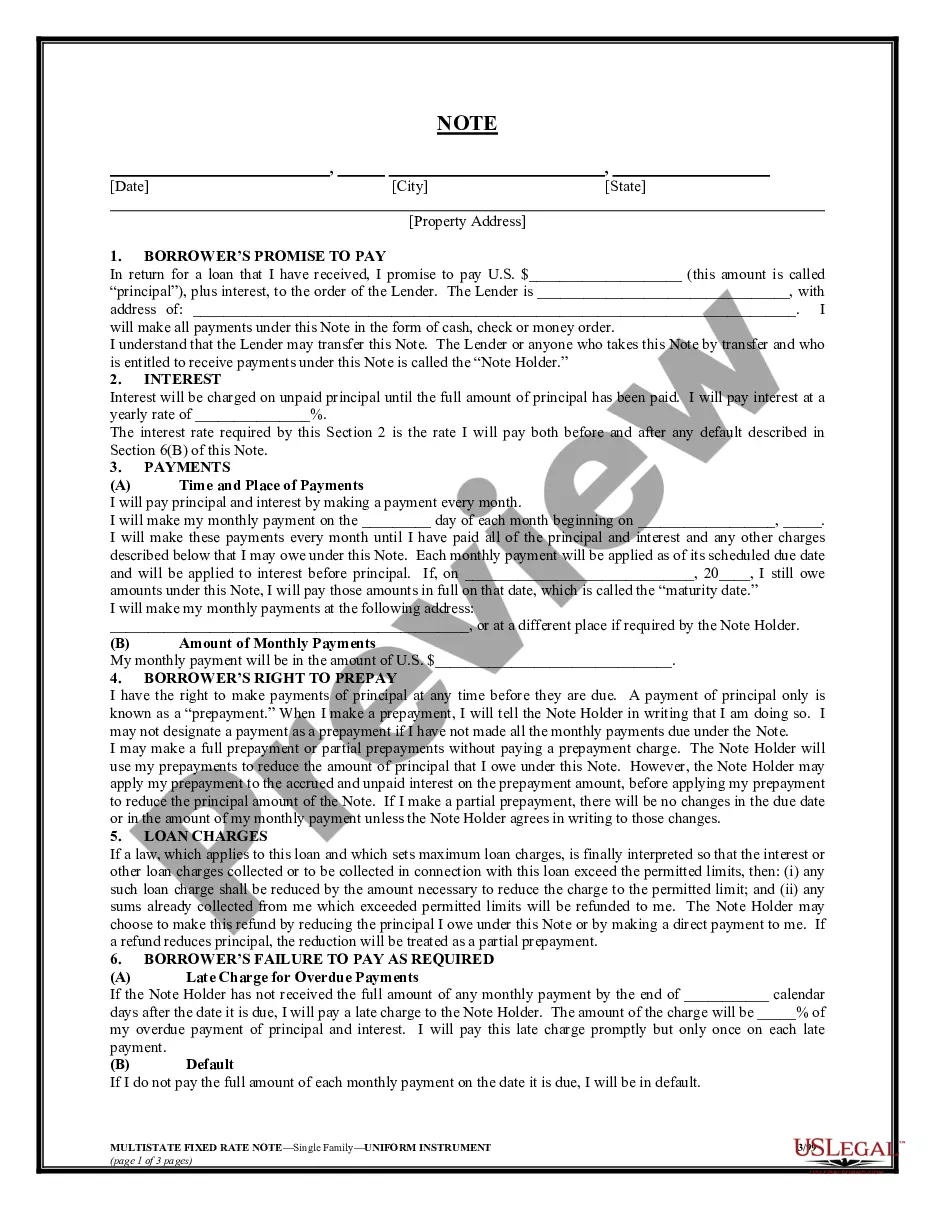

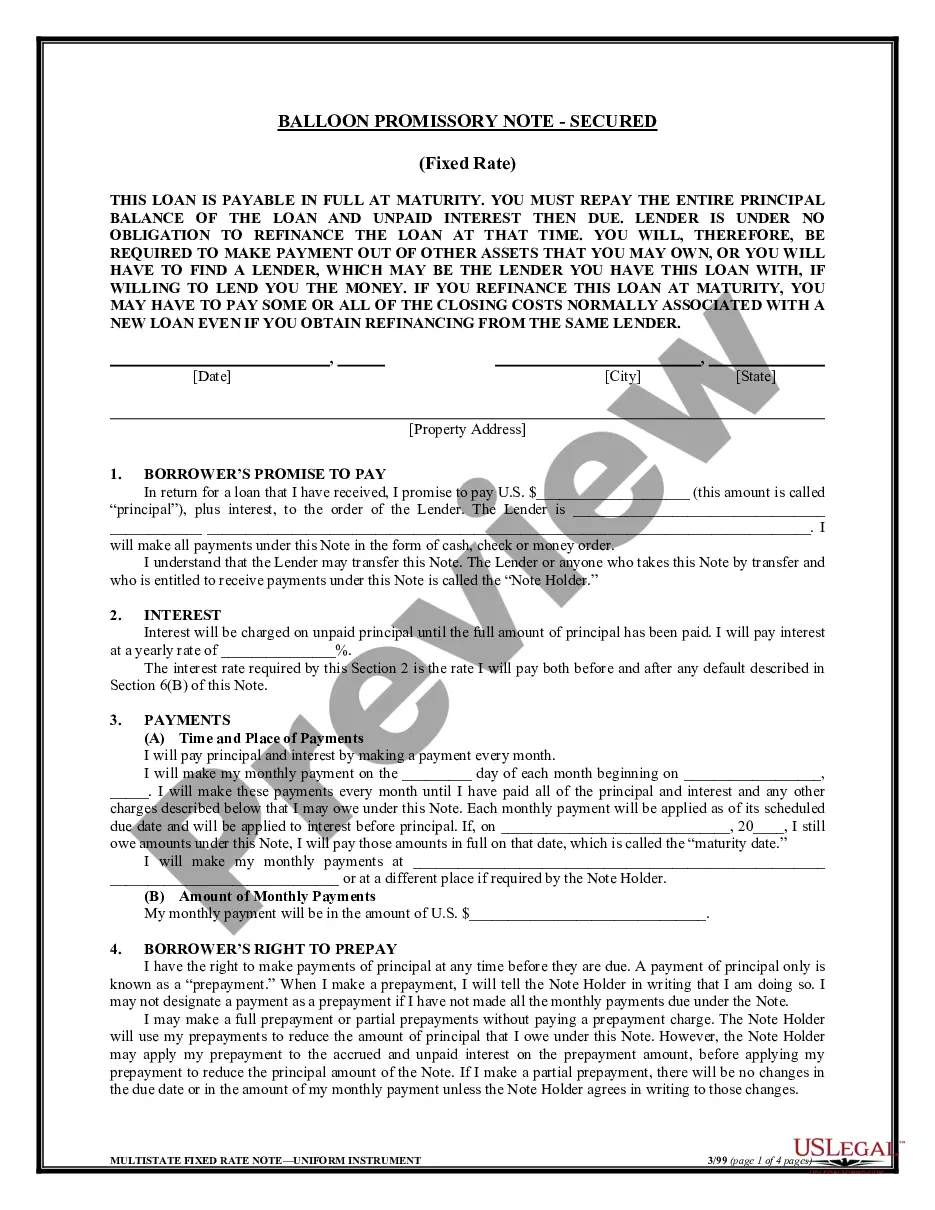

This form is a promissory note. See preview below.

Cook Illinois Promissory Note

Category:

State:

Illinois

County:

Cook

Control #:

IL-17074-MH

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Illinois Promissory Note?

We continually aim to reduce or evade legal complications when handling intricate legal or financial matters.

To achieve this, we seek legal assistance, which is typically quite costly.

Nevertheless, not all legal issues are equally intricate; many can be managed independently.

US Legal Forms is an online repository of current DIY legal templates ranging from wills and powers of attorney to articles of incorporation and requests for dissolution.

Simply Log In to your account and click the Get button next to it. If you have lost the document, you can always retrieve it again from the My documents tab. The process is equally straightforward for newcomers to the site! You can create your account in a matter of minutes. Ensure that the Cook Illinois Promissory Note complies with the laws and regulations of your state and locality. Additionally, it is essential to review the form's description (if available), and if you notice any mismatches with what you initially sought, look for another template. Once you've confirmed that the Cook Illinois Promissory Note meets your needs, you can select a subscription plan and proceed to payment. You can then download the document in any preferred file format. For more than 24 years, we have assisted millions of individuals by providing customizable and current legal forms. Take advantage of US Legal Forms today to conserve time and resources!

- Our collection enables you to manage your affairs independently without needing an attorney's services.

- We offer access to legal document templates that are not always readily available.

- Our templates are specific to states and regions, greatly simplifying the search process.

- Utilize US Legal Forms anytime you require to obtain and download the Cook Illinois Promissory Note or any other document swiftly and securely.

Form popularity

FAQ

Several factors can render a Cook Illinois Promissory Note unenforceable, such as missing signatures, unclear terms, or violations of state laws. Additionally, if the note involves illegal activity or lacks consideration, it may not hold up in court. Understanding these pitfalls is vital; thus, seeking guidance from uslegalforms can help you create a valid and powerful promissory note. This proactive approach can save you legal troubles down the line.

The enforceability of a Cook Illinois Promissory Note largely depends on its compliance with legal standards. Generally, notes that include clear terms and are signed by both parties have a good chance of being enforced in court. It's important to keep accurate records and follow through on terms outlined in the note. To minimize risk, using resources like uslegalforms helps you craft a comprehensive promissory note that meets all legal requirements.

A Cook Illinois Promissory Note is generally a strong legal document when properly created and executed. Courts typically uphold valid promissory notes that meet necessary requirements, such as clear terms and mutual consent. However, the enforceability can depend on specific circumstances, including proper documentation and adherence to state laws. When you draft a promissory note, using platforms like uslegalforms ensures you have the correct structure to support its legality.

In Illinois, a Cook Illinois Promissory Note does not necessarily need to be notarized to be valid. However, notarization can add an extra layer of security and help in case of disputes. It's advisable to consider notary services for enhanced legal protection.

The conditions of a Cook Illinois Promissory Note typically include the repayment schedule, interest rate, and default consequences. It's important to outline any collateral, if applicable, as this can affect repayment terms. Clear conditions help prevent misunderstandings later.

For a Cook Illinois Promissory Note to be valid, it must include the names of the parties involved, the amount loaned, and the repayment terms. Additionally, it must be signed by the borrower. If these key elements are missing, the note may not hold up in court.

You typically file a Cook Illinois Promissory Note with the county recorder’s office where the property or transaction is located. Recording your note creates a public record, which can prevent future claims against your rights. Some individuals may choose to keep it in a safe place, but recording provides essential legal protection. Using uslegalforms can help streamline the filing process with accurate templates and resources.

To report a Cook Illinois Promissory Note on your taxes, you'll need to include any interest income earned from the note on your annual return. For lenders, this interest is typically reported on Schedule B of Form 1040. If you sold the note, there may be additional reporting requirements related to capital gains. Understanding your tax obligations can help you avoid potential issues down the line.

Reporting a Cook Illinois Promissory Note on your tax return requires you to disclose any interest income received. If you are the lender, the interest you earn is considered taxable income. You will need to report this income on Schedule B, which is part of Form 1040. It’s always wise to consult with a tax professional to ensure you correctly report your income.

A Cook Illinois Promissory Note does not need to be recorded to be valid, but recording can provide additional benefits. When you file your promissory note with the appropriate office, it establishes a public record, helping to protect your interests. This can be especially important in cases where disputes arise. Ultimately, whether to record your note depends on your specific needs and circumstances.