Alaska Living Trust

Living Trusts help manage assets during and after life. Attorney-drafted templates are quick and easy to complete.

Similar documents: key differences

- Revocable Trust vs. Irrevocable Trust — Revocable trusts can be changed by the grantor, while irrevocable trusts cannot.

- Grantor Trust vs. Non-Grantor Trust — Grantor trusts allow the original owner to retain control, whereas non-grantor trusts do not.

- Family Trust vs. Living Trust — Family trusts are specifically for family assets, while living trusts can encompass any assets.

- Joint Living Trust vs. Individual Living Trust — Joint trusts are for two or more individuals, while individual trusts are for one person.

Search for more forms

Types of Living trusts forms

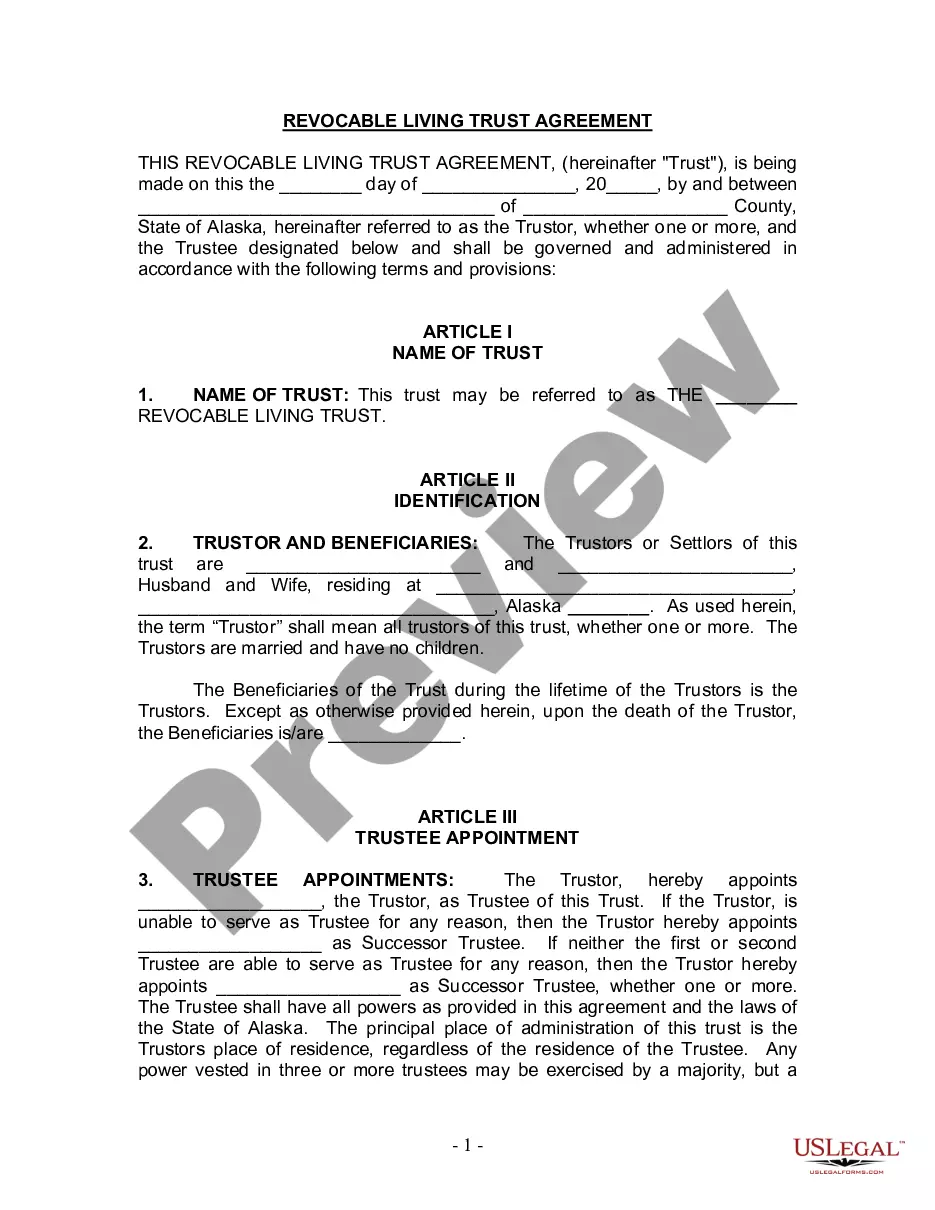

Revocable for Married Couple

Create a flexible estate plan that lets married couples manage and transfer their assets easily and efficiently.

Husband and Wife with No Children

Create a flexible estate plan that protects your assets and ensures your wishes are honored during your lifetime and after.

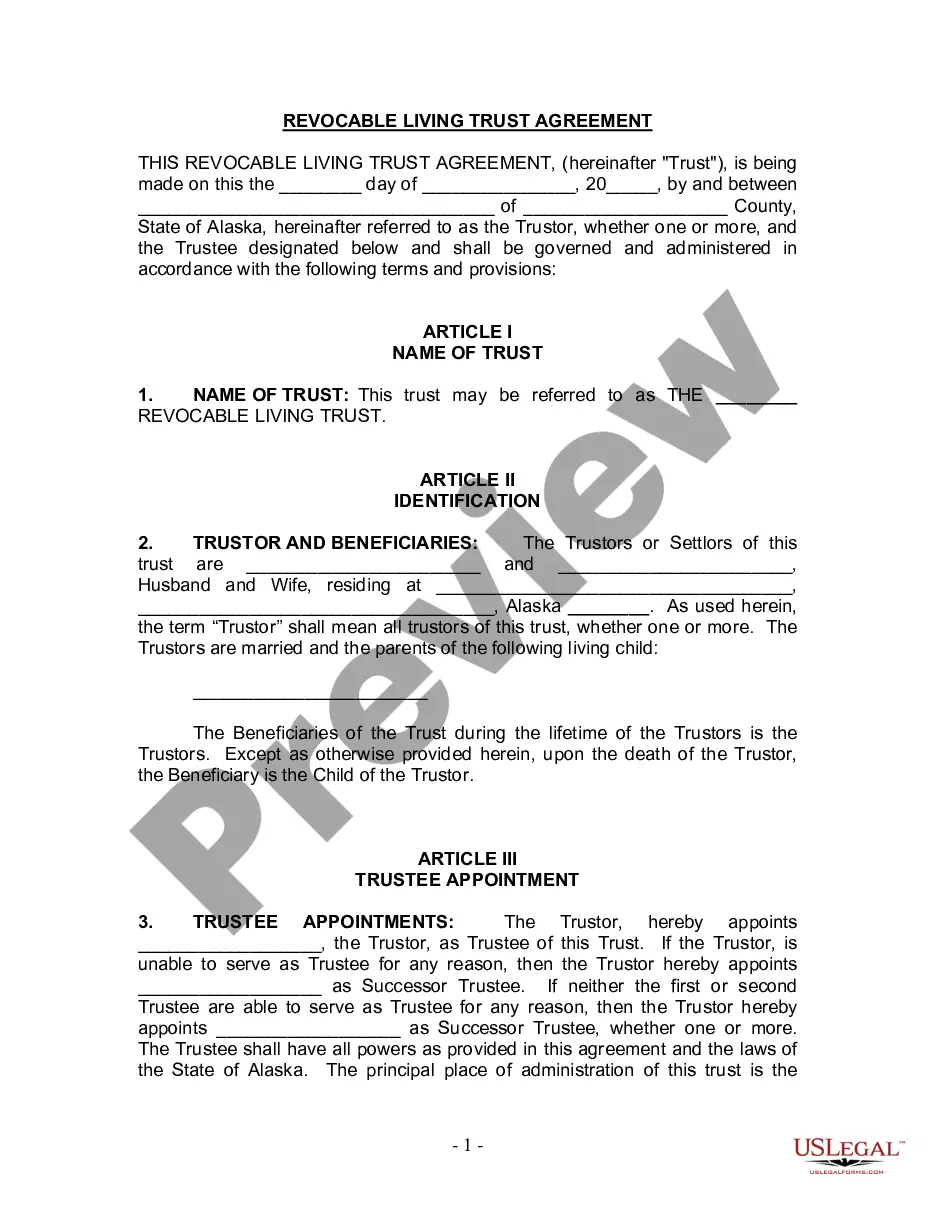

Living Trust for Husband and Wife with Children

Create a revocable living trust to manage your assets and provide for your minor and adult children after your passing.

Husband and Wife with One Child

Establish a trust to manage and protect assets for a couple and their child, ensuring smooth asset distribution upon death.

Revocable for Single Person

Establish a flexible estate plan that you can modify anytime, making it ideal for individuals managing their own assets.

Living Trust - Basic Revocable

Create a personalized estate plan that allows you to manage and distribute your assets during your lifetime and after your passing.

Irrevocable

Ensure your assets are managed without court involvement during incapacity or after death.

Assignment

Effectively transfer assets into a living trust to manage estate planning and avoid probate.

Individual, Who Is Single, Divorced

Create a revocable living trust to manage your assets and provide for your children after your passing.

Financial Account Transfer

Transfer financial accounts into a living trust to avoid probate and ensure smooth asset management for your beneficiaries.

Letter to Lienholder

Notify lienholders about property transfers to a trust, ensuring proper record updates.

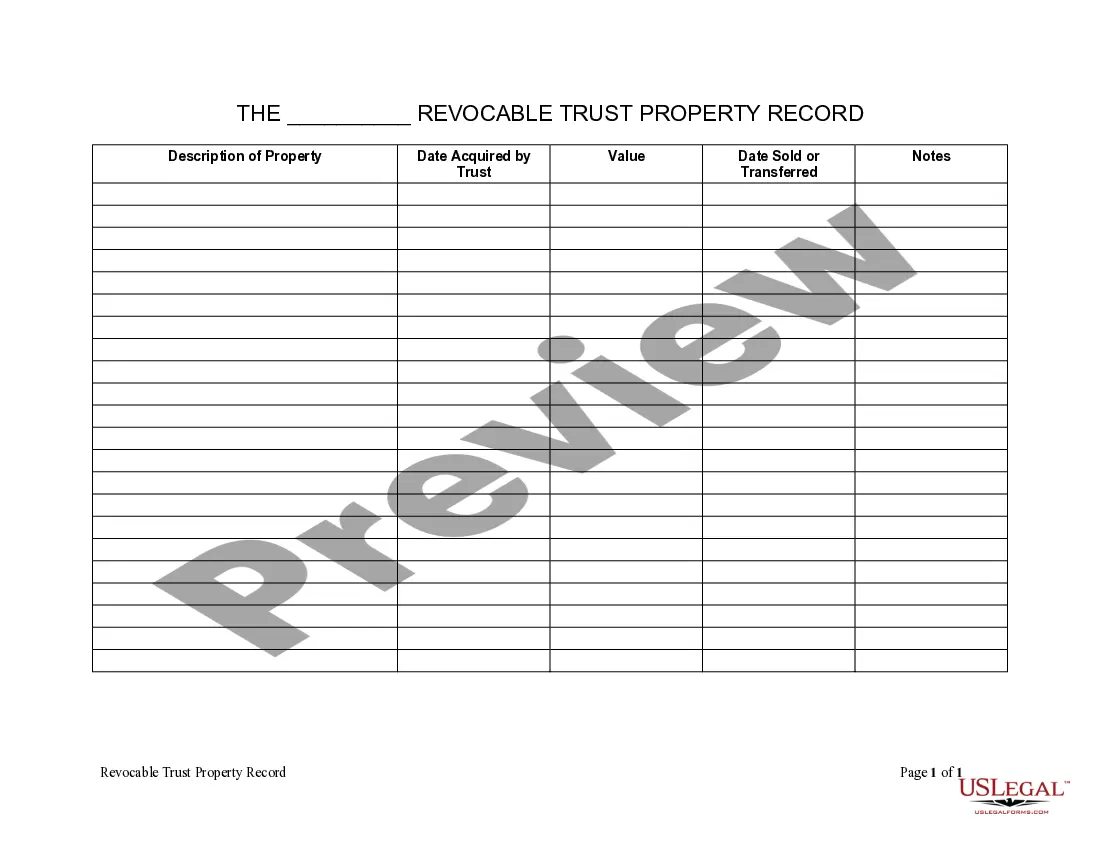

Property Record

Keep an organized record of property held in a living trust for easy management and transfer.

Individual as Single, Divorced

Establish a personalized living trust to manage your assets during your lifetime and specify distribution after death, ideal for individuals without children.

Amendment

Make important changes to a living trust, ensuring your estate plan reflects your current wishes and circumstances.

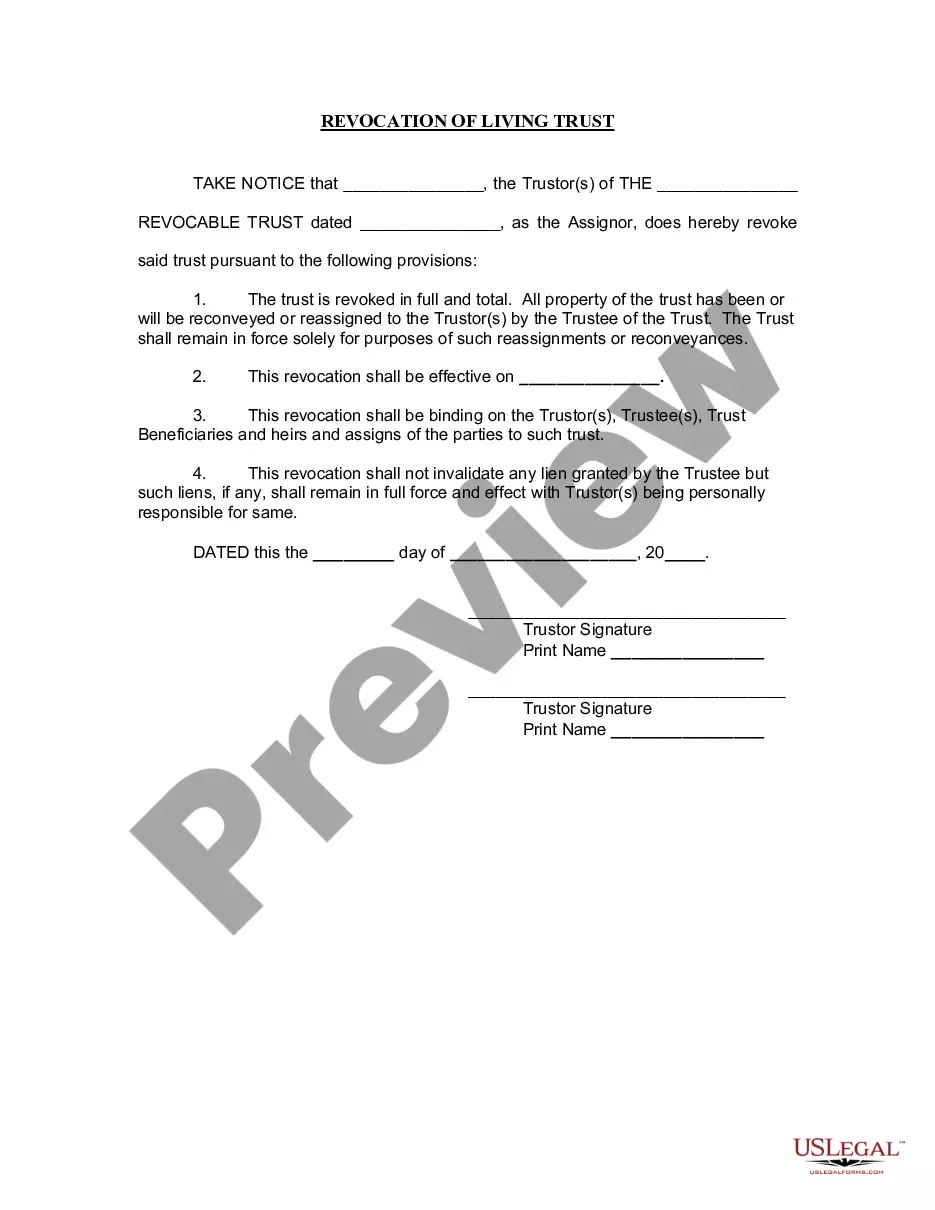

Revocation

Use this document to formally revoke a living trust, ensuring all assets are returned to the trustor.

Common Alaska Living Trust documents

- Revocable Living Trust — establishes a trust that can be modified during the grantor's lifetime.

- Amendment to Living Trust — updates terms of an existing trust without creating a new one.

- Revocation of Living Trust — formally cancels a previously established trust.

- Living Trust Agreement — outlines the terms and conditions of the trust.

- Declaration of Trust — states the existence of the trust and its terms.

FAQs

A trust can complement a will by managing assets during life and after death.

Without a plan, state laws will dictate asset distribution, which may not align with your wishes.

It's wise to review your plan every few years or after major life events.

Beneficiary designations can override trust instructions, so it's important to coordinate them.

Yes, you can appoint different individuals for financial and healthcare decisions.

Key legal points

- Living Trusts can help avoid probate, saving time and money.

- They provide flexibility in asset management during the grantor's lifetime.

- Assets in a Living Trust are managed by a trustee.

- Living Trusts can be amended or revoked at any time by the grantor.

- Beneficiaries receive assets directly from the trust upon the grantor's death.

How to get started

Begin effortlessly with these steps.

- Find a template or package that fits your situation.

- Review the description, preview, and signing requirements.

- Get full access with a subscription.

- Complete it in the online editor.

- Export or send: download, email, USPS mail, notarize online, or send for e-signature.

Practical tip

Consider setting up a revocable trust first to maintain flexibility in managing your assets.