Washington Notice of Adverse Action - Non-Employment - Due to Credit Report

Description

How to fill out Notice Of Adverse Action - Non-Employment - Due To Credit Report?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a selection of legal document templates that you can download or create.

By using the website, you can find thousands of forms for business and personal purposes, organized by categories, states, or keywords.

You can access the latest versions of forms such as the Washington Notice of Adverse Action - Non-Employment - Due to Credit Report in just a few minutes.

Review the form description to confirm you have chosen the right form.

If the form does not meet your needs, utilize the Search area at the top of the screen to find one that does.

- If you already hold a membership, sign in and download the Washington Notice of Adverse Action - Non-Employment - Due to Credit Report from the US Legal Forms library.

- The Download button will appear on each form you view.

- You can access all previously saved forms in the My documents tab of your account.

- To use US Legal Forms for the first time, here are simple instructions to get started.

- Ensure you have selected the correct form for your city/state.

- Click the Preview button to review the form`s content.

Form popularity

FAQ

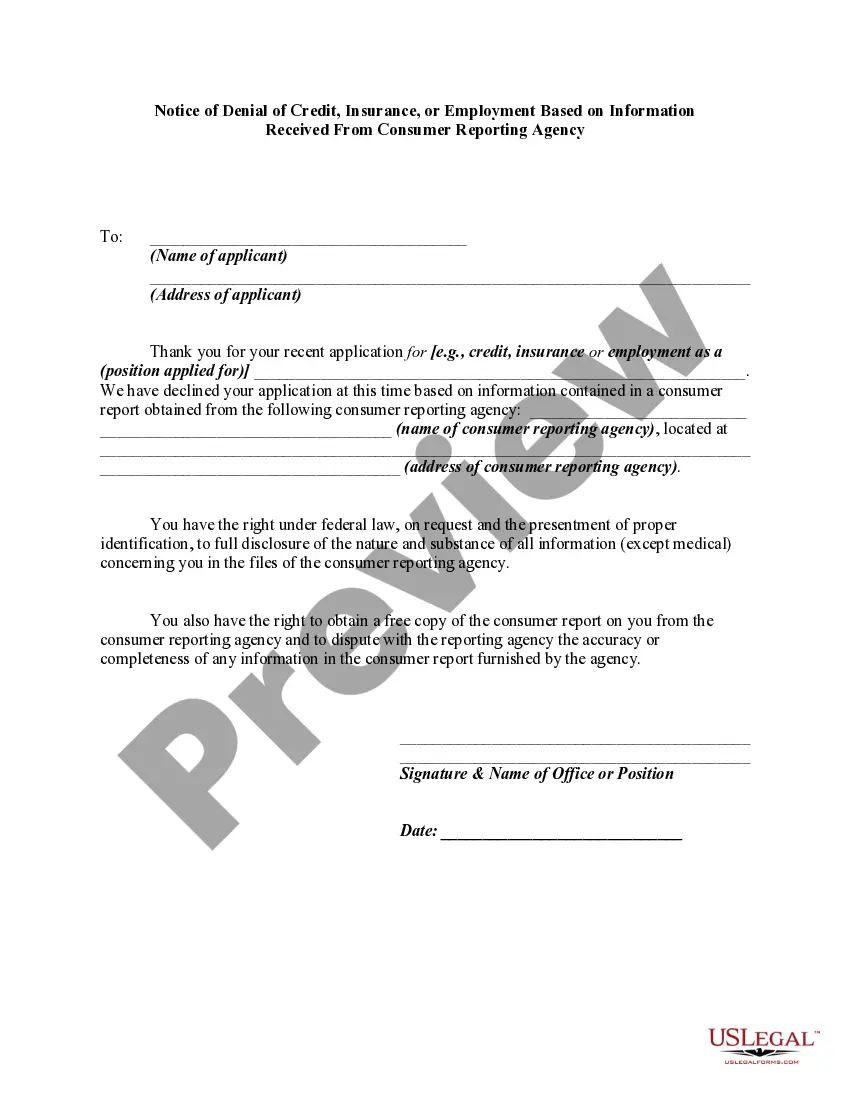

Adverse action is defined in the Equal Credit Opportunity Act and the FCRA to include: a denial or revocation of credit. a refusal to grant credit in the amount or terms requested. a negative change in account terms in connection with an unfavorable review of a consumer's account 5 U.S.C.

An adverse action notice will not hurt your credit score or show up on your credit report. However, if the creditor pulls a hard credit inquiry, this may temporarily lower your scoreand all hard inquiries remain on your credit report for two years.

If you deny a consumer credit based on information in a consumer report, you must provide an adverse action notice to the consumer. if you grant credit, but on less favorable terms based on information in a consumer report, you must provide a risk-based pricing notice.

It must include information about the credit bureau used, an explanation of the specific reasons for the adverse action, a notice of the consumer's right to a free credit report and to dispute its accuracy and the consumer's credit score.

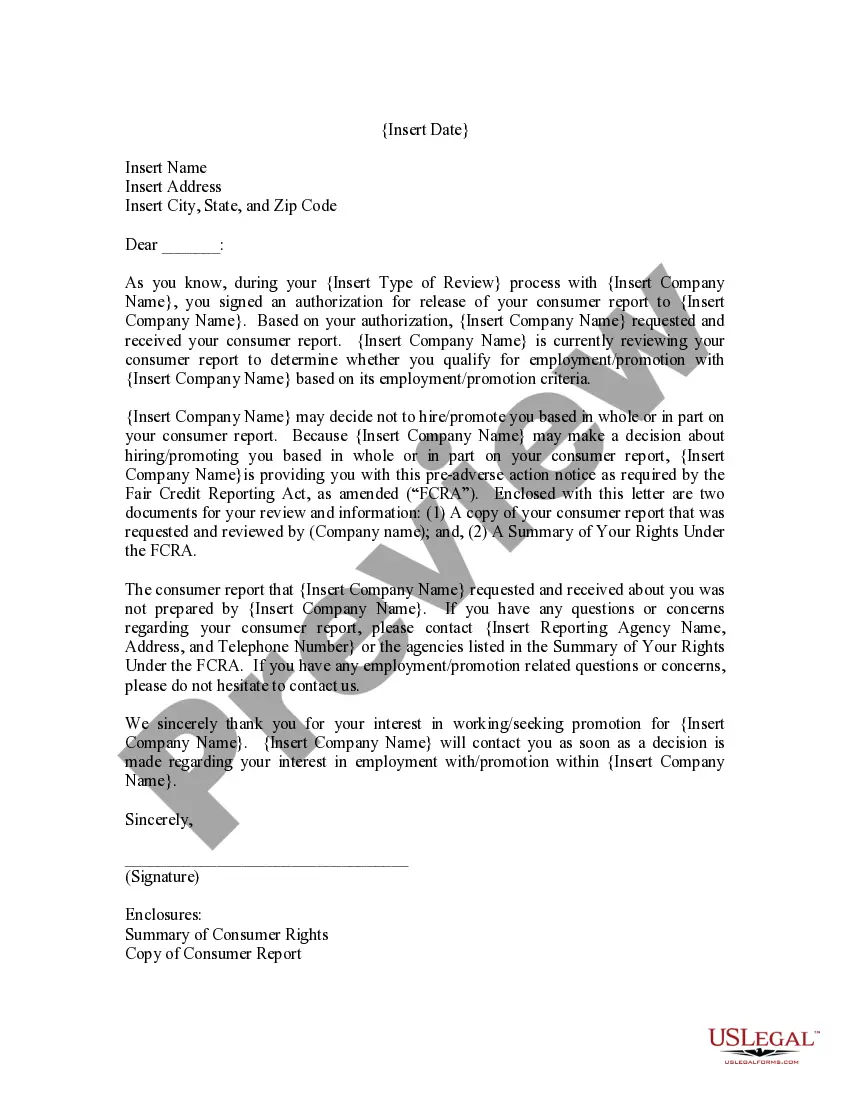

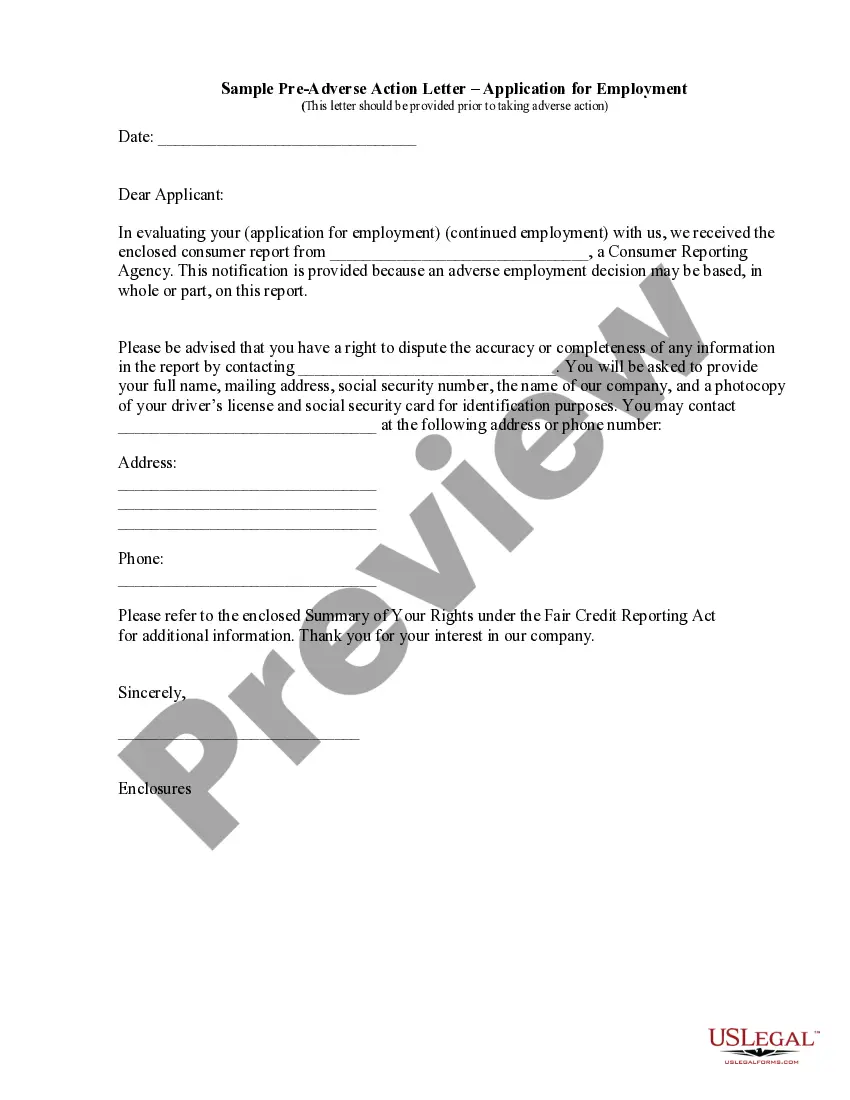

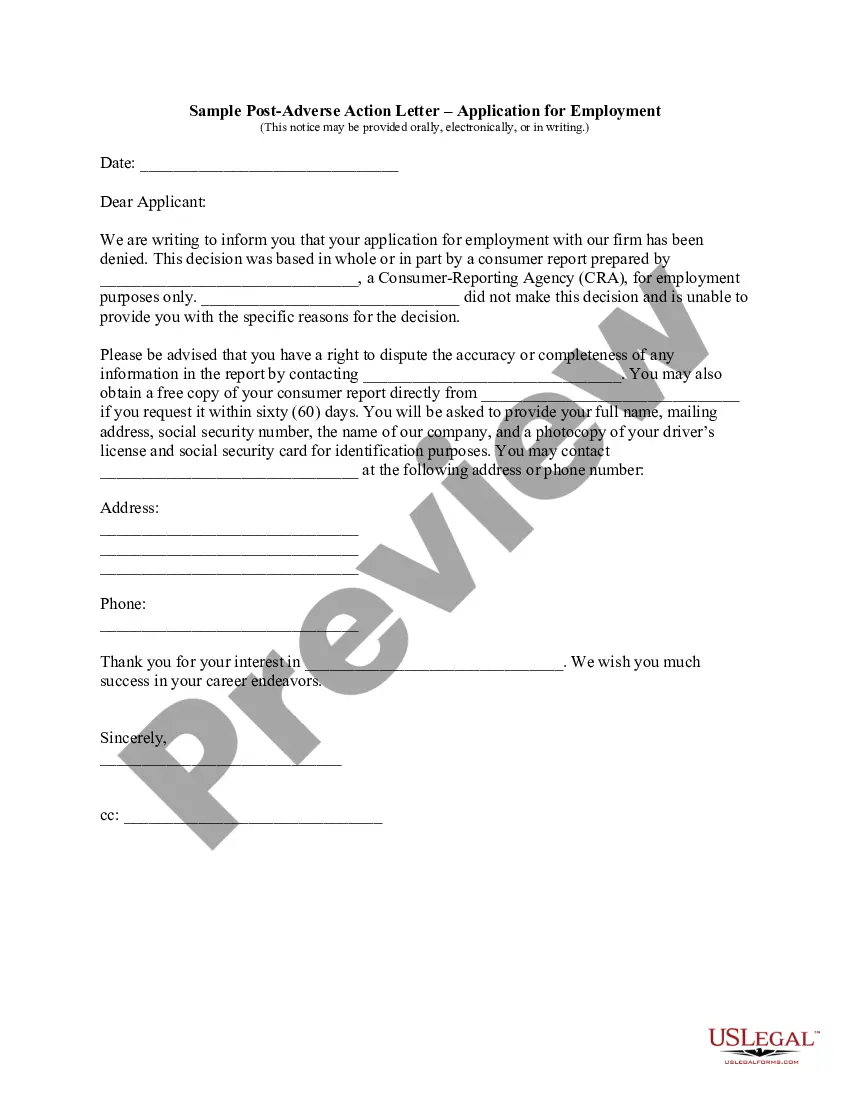

An adverse action notice is to inform you that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should indicate which credit reporting agency was used, and how to contact them.

A creditor must notify the applicant of adverse action within: 30 days after receiving a complete credit application. 30 days after receiving an incomplete credit application. 30 days after taking action on an existing credit account.

An adverse action notice is to inform you that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should indicate which credit reporting agency was used, and how to contact them.

A consumer applies to the credit card issuer for a credit card. The card issuer obtains a credit score for the consumer. The consumer's credit score is 700. Since the consumer's 700 credit score falls below the 720 cutoff score, the credit card issuer must provide a risk-based pricing notice to the consumer.

30 days after receiving an incomplete credit application; 30 days after taking action on an existing credit account; 90 days after making a counteroffer to an application for credit if the applicant does not accept the counteroffer.

The first part of the 30-day rule requires creditors to provide notification of their credit decision within 30 days after receiving a completed application concerning the creditor's approval of, or counteroffer to, or adverse action on the application. While this is a mouthful to say, it really isn't that difficult.