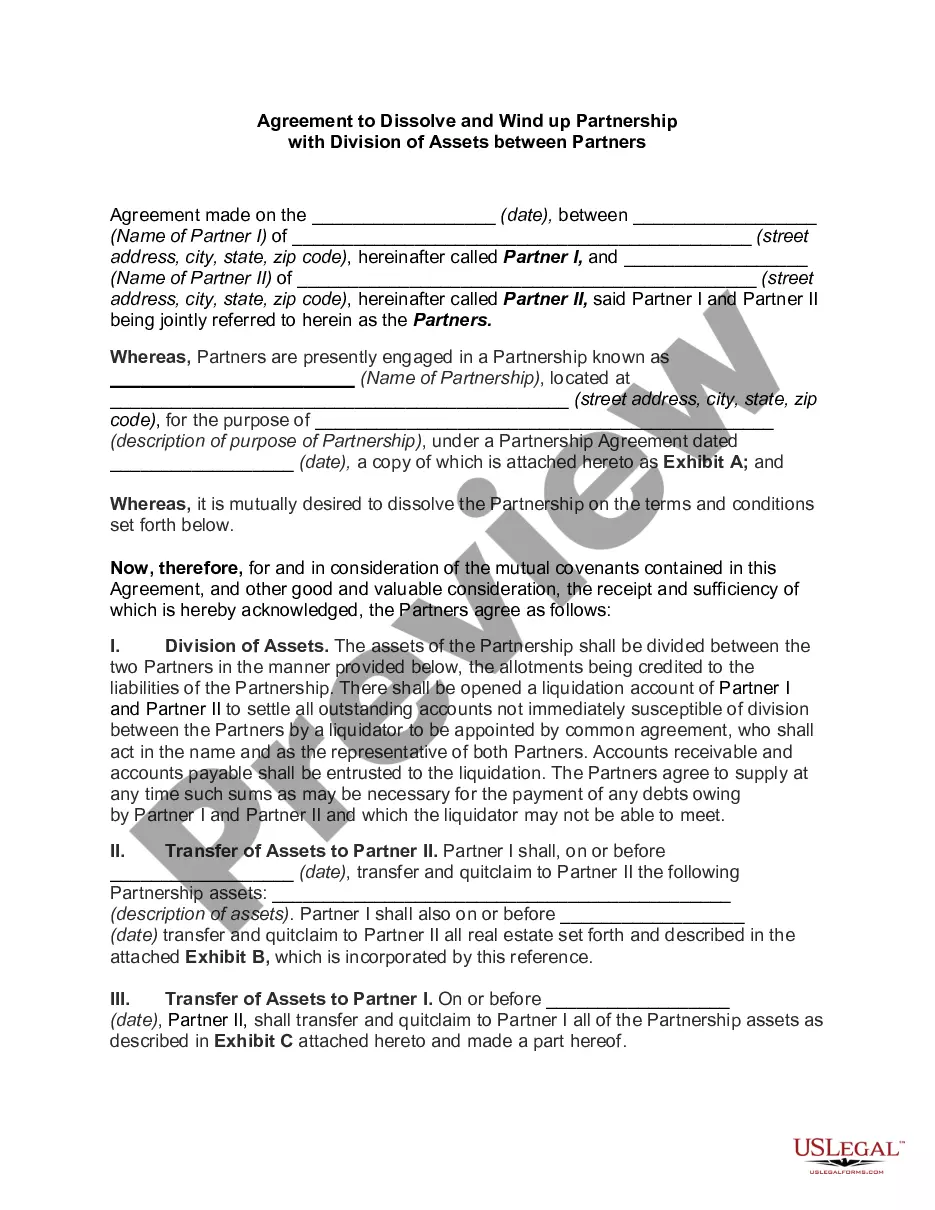

Washington Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner

Description

How to fill out Agreement To Dissolve And Wind Up Partnership Between Surviving Partners And Estate Of Deceased Partner?

If you seek to complete, acquire, or generate sanctioned document templates, utilize US Legal Forms, the most extensive collection of legal forms accessible online.

Employ the site’s simple and user-friendly search to locate the documents you need.

Numerous templates for business and personal purposes are organized by categories and states, or keywords.

Step 5. Process the payment. You can use your Visa or Mastercard or PayPal account to complete the transaction.

Step 6. Select the format of the legal form and download it to your device.Step 7. Complete, modify, and print or sign the Washington Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner.

- Utilize US Legal Forms to obtain the Washington Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner with just a few clicks.

- If you are already a US Legal Forms customer, Log In to your account and click the Download option to retrieve the Washington Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner.

- You can also access forms you previously acquired in the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the guidelines below.

- Step 1. Ensure you have selected the form for your correct city/state.

- Step 2. Use the Review option to examine the form’s contents. Remember to read the description.

- Step 3. If you are dissatisfied with the type, use the Search field at the top of the screen to find alternative versions of the legal form template.

- Step 4. Once you have found the form you need, click the Buy now option. Choose the pricing option you prefer and enter your details to register for an account.

Form popularity

FAQ

Winding up a partnership business is a procedure that distributes, or liquidates, any remaining property of the partnership and any assets that remain after the dissolution of the partnership business. Only those partners that remain with the partnership have the right to partnership assets in the wind up process.

A liquidating partner is a partner who is appointed to settle the accounts, collect the assets, adjust the claims and pay the debts of a dissolving or insolvent firm. A liquidating partner will be responsible for selling and distributing assets and settling debts in a partnership that is in the process of liquidation.

Most legislation states that the partnership will end upon the death or bankruptcy of any partner. If your partner dies, you will then owe your partner's estate their share of the partnership that accrues at the date of their death.

If it was death that had caused the end of the partnership, then the monies are paid out in equal shares to the surviving ex-partners and the deceased's estate. When all the partners are living there may be room to negotiate, but when one of them dies, the options disappear, especially if the beneficiaries are minors.

The death of a partner in a two-person partnership will terminate the partnership for federal tax purposes if it results in the partnership's immediately winding up its business (Sec. 708(b)(1)(A)). If this occurs, the partnership's tax year closes on the partner's date of death.

A general partnership is one in which all of the partners have the ability to actively manage or control the business. This means that every owner has authority to make decisions about how the business is run as well as the authority to make legally binding decisions.

Section 37 of the UPA provides that unless otherwise agreed, the partners who have not wrongfully dissolved the partnership or the legal representative of the last surviving solvent partner have the right to wind up the partnership affairs, provided, however, that any partner, his legal representative, or his assignee

The death of a partner or the unauthorized transfer of ownership of his share in the partnership in case there is a limitation to this effect results in the dissolution thereof. In other words, any change in the composition of the partnership, unless so allowed, will result in the dissolution thereof.

When a partner in a partnership dies, the basic position under the Partnership Act 1890 is that the partnership is dissolved: 'Subject to any agreement between the partners, every partnership is dissolved as regards all the partners by the death2026 of any partner.

Keeping it successful is even harder, and coping with the death of a partner may be the hardest situation of all. When that happens, your deceased partner's share in the business usually passes to a surviving spouse, either by terms of a will or simply by default as the primary heir.