Washington Breakdown of Savings for Budget and Emergency Fund

Description

How to fill out Breakdown Of Savings For Budget And Emergency Fund?

Are you in a circumstance where you need paperwork for business or personal needs every day.

There are numerous legal document templates available online, but locating trustworthy ones isn't simple.

US Legal Forms offers a vast array of form templates, such as the Washington Overview of Savings for Budget and Emergency Fund, designed to comply with both federal and state regulations.

Choose a convenient document format and download your copy.

Access all the document templates you have purchased in the My documents section. You can download another copy of the Washington Overview of Savings for Budget and Emergency Fund whenever needed. Just select the required form to download or print the template.

Utilize US Legal Forms, the most extensive collection of legal forms, to save time and avoid errors. This service offers professionally crafted legal document templates that can be used for various purposes. Create an account on US Legal Forms and begin simplifying your life.

- If you are already acquainted with the US Legal Forms website and possess an account, simply Log In.

- After that, you can download the Washington Overview of Savings for Budget and Emergency Fund template.

- If you do not have an account and wish to begin using US Legal Forms, take these steps.

- Find the form you need and ensure it is for your specific city/county.

- Use the Review button to inspect the document.

- Look at the description to confirm that you have selected the correct form.

- If the form isn't what you're looking for, utilize the Search field to locate the document that fits your needs and requirements.

- Once you find the appropriate form, click Buy now.

- Choose the pricing plan you want, enter the required information to create your account, and pay for your order using your PayPal or credit card.

Form popularity

FAQ

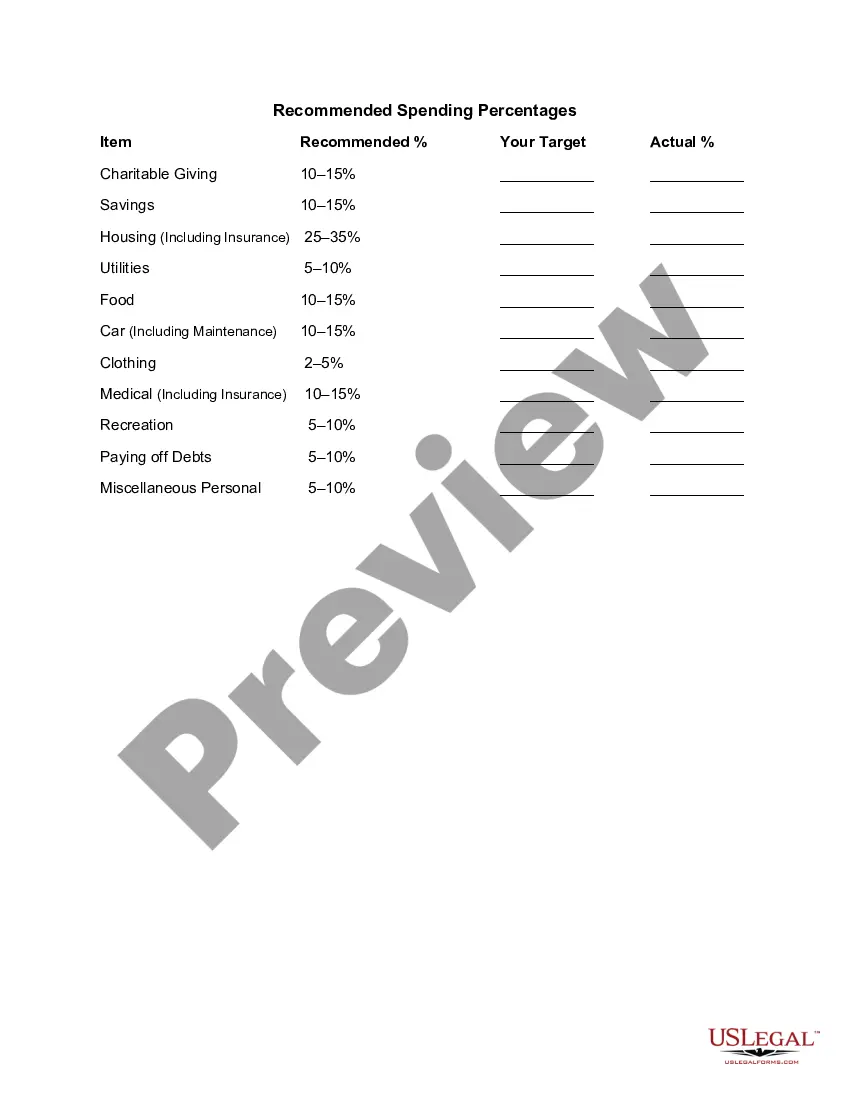

Financial experts agree that a fully-funded emergency fund should be between three and six months of living expenses.

The 70/30 rule in finance allows us to spend, save, and invest. It's simple. Divide the monthly take-home pay by 70% for monthly expenses, and 30% is subdivided into 20% savings (including debt), 10% to tithing, donation, investment, or retirement.

The 70/30 method is a budgeting technique to help you allocate your money, Kia says. Put simply, each month, 70% of the money that you earn will be your spending money, including essentials like bills and rent as well as luxuries, and 30% of the money you earn will go towards your savings.

The 50/30/20 rule is an easy budgeting method that can help you to manage your money effectively, simply and sustainably. The basic rule of thumb is to divide your monthly after-tax income into three spending categories: 50% for needs, 30% for wants and 20% for savings or paying off debt.

70% is for monthly expenses (anything you spend money on). 20% goes into savings, unless you have pressing debt (see below for my definition), in which case it goes toward debt first. 10% goes to donation/tithing, or investments, retirement, saving for college, etc.

If you have consumer debt, I recommend saving a starter emergency fund of $1,000 first. Then, once you're out of debt, it's time to beef up that amount and save three to six months of expenses in a fully funded emergency fund.

It's all about your personal expenses Those include things like rent or mortgage payments, utilities, healthcare expenses, and food. If your monthly essentials come to $2,500 a month, and you're comfortable with a four-month emergency fund, then you should be set with a $10,000 savings account balance.

Most experts believe you should have enough money in your emergency fund to cover at least 3 to 6 months' worth of living expenses.

While the size of your emergency fund will vary depending on your lifestyle, monthly costs, income, and dependents, the rule of thumb is to put away at least three to six months' worth of expenses.

Senator Elizabeth Warren popularized the so-called "50/20/30 budget rule" (sometimes labeled "50-30-20") in her book, All Your Worth: The Ultimate Lifetime Money Plan. The basic rule is to divide up after-tax income and allocate it to spend: 50% on needs, 30% on wants, and socking away 20% to savings.