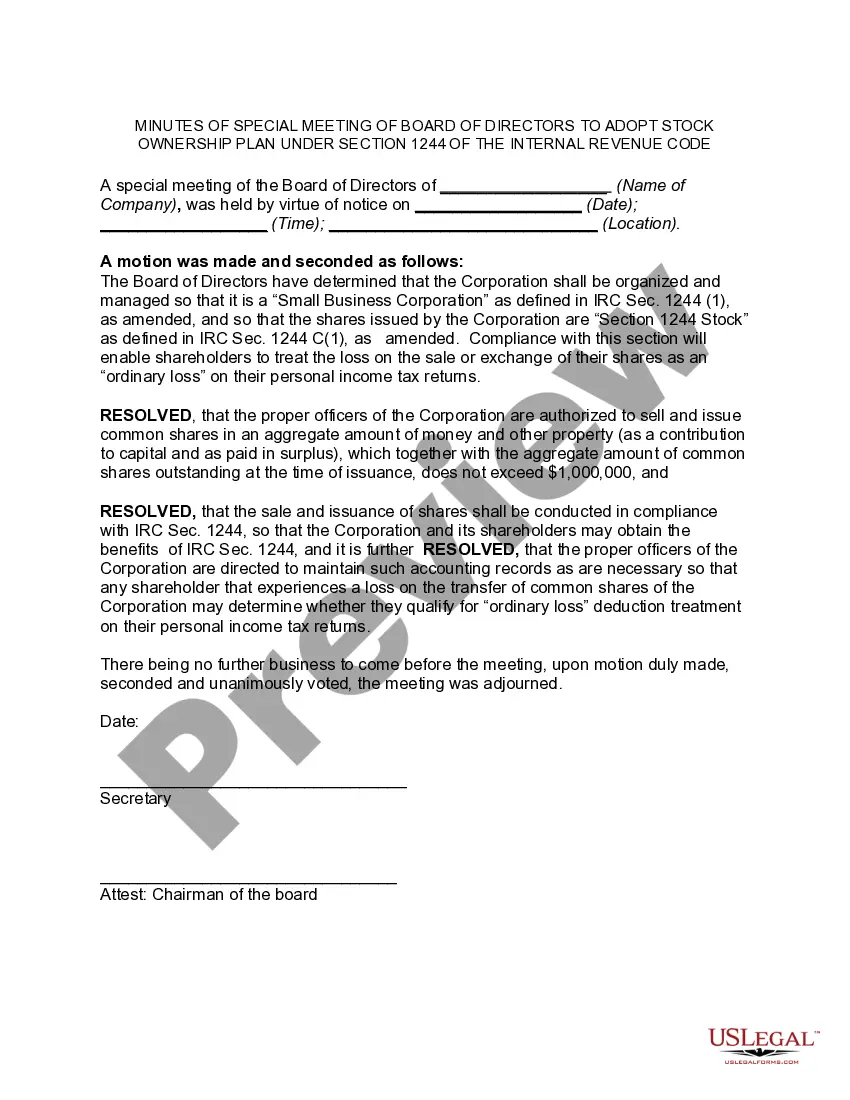

Washington Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code

Description

to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code")

to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code")

How to fill out Minutes Of Special Meeting Of The Board Of Directors Of (Name Of Corporation) To Adopt Stock Ownership Plan Under Section 1244 Of The Internal Revenue Code?

If you need to download, fill out, or print authorized file templates, utilize US Legal Forms, the largest collection of lawful forms available online.

Leverage the site's straightforward and user-friendly search functionality to find the documents you require.

A range of templates for commercial and individual purposes are categorized by types and states, or search keywords.

Step 4. After you have located the form you need, click the Purchase now button. Choose your preferred pricing plan and enter your details to sign up for an account.

Step 5. Complete the purchase. You can use your Visa, MasterCard, or PayPal account to finalize the transaction.

- Use US Legal Forms to acquire the Washington Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code with just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and click the Obtain button to access the Washington Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code.

- You can also access forms you've previously submitted electronically from the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the steps below.

- Step 1. Ensure you have chosen the form for the correct city/state.

- Step 2. Utilize the Review feature to review the contents of the form. Don't forget to check the description.

- Step 3. If you are unsatisfied with the form, use the Search field at the top of the screen to find other forms within the legal form template.

Form popularity

FAQ

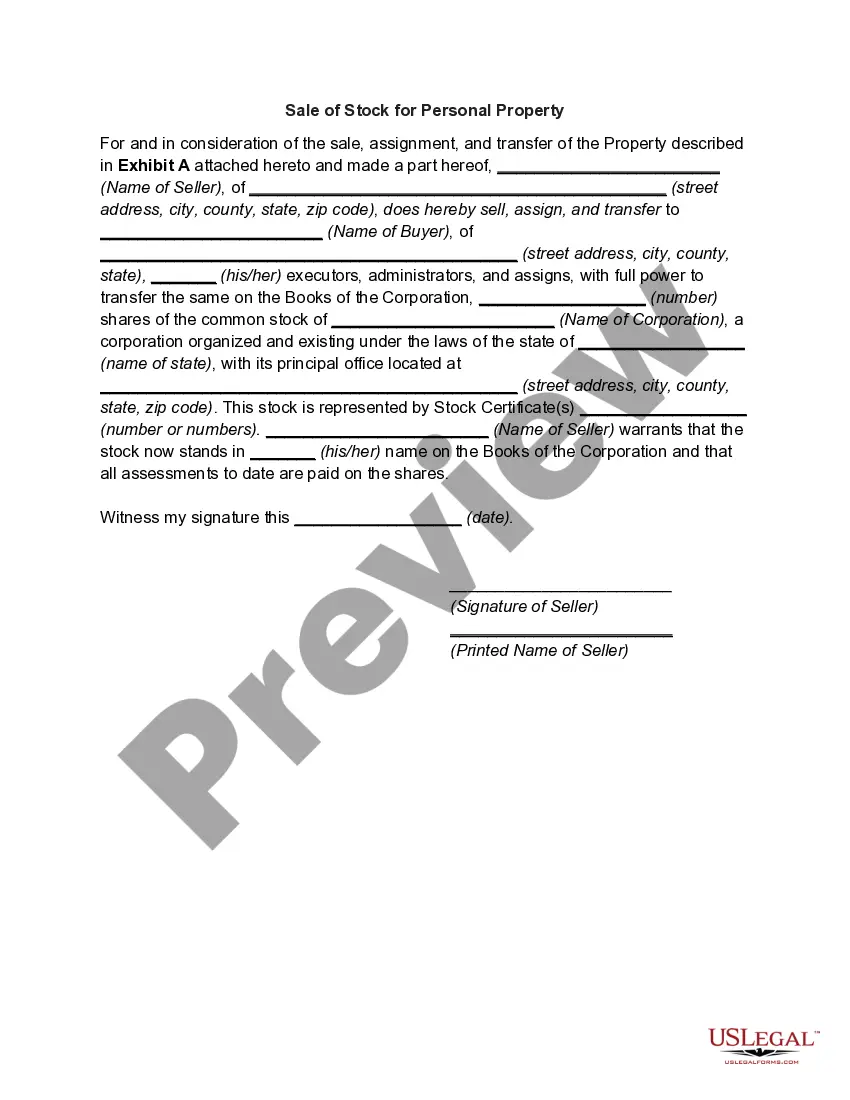

The determination of whether stock qualifies as Section 1244 stock is made at the time of issuance. Section 1244 stock is common or preferred stock issued for money or other property by a domestic small business corporation (which can be a C or S corporation) that meets a gross receipts test.

To qualify under Section 1244, these five requirements must be adhered to:The stock must be acquired in exchange for cash or property contributed to the corporation.The corporation must issue the stock directly to the investors.The corporation must be an actual, operating company.More items...?

HW: How are gains from the sale of § 1244 stock treated? losses? The general rule is that shareholders receive capital gain or loss treatment upon the sale or exchange of stock. However, it is possible to receive an ordinary loss deduction if the loss is sustained on small business stock (A§ 1244 stock).

Section 1244 of the Internal Revenue Code is the small business stock provision enacted to allow shareholders of domestic small business corporations to deduct a loss on the disposal of such stock as an ordinary loss rather than as a capital loss, which is limited to only $3,000 annually.

1244 losses are allowed for NOL purposes without being limited by nonbusiness income. An annual limitation is imposed on the amount of Sec. 1244 ordinary loss that is deductible. The maximum deductible loss is $50,000 per year ($100,000 if a joint return is filed) (Sec.

Qualifying for Section 1244 StockThe stock must be issued by U.S. corporations and can be either a common or preferred stock.The corporation's aggregate capital must not have exceeded $1 million when the stock was issued and the corporation cannot derive more than 50% of its income from passive investments.More items...

1244(b)). Any loss in excess of the limit is a capital loss, subject to the capital loss rules. Thus, if the potential loss exceeds the $50,000 (or $100,000) limit, the stock should be disposed of in more than one year to maximize the ordinary loss treatment.

Under Section 1244, an individual stockholder of a corporation can claim an ordinary (rather than capital) loss of up to $50,000 per year (or $100,000 for on a joint return) from the sale or worthlessness of Section 1244 stock. For most stockholders, an ordinary loss is much more beneficial than a capital loss.

Section 1244 of the Internal Revenue Code allows eligible shareholders of domestic small business corporations to deduct a loss on the disposal of such stock as an ordinary loss rather than a capital loss. Eligible investors include individuals, partnerships and LLCs taxed as partnerships.