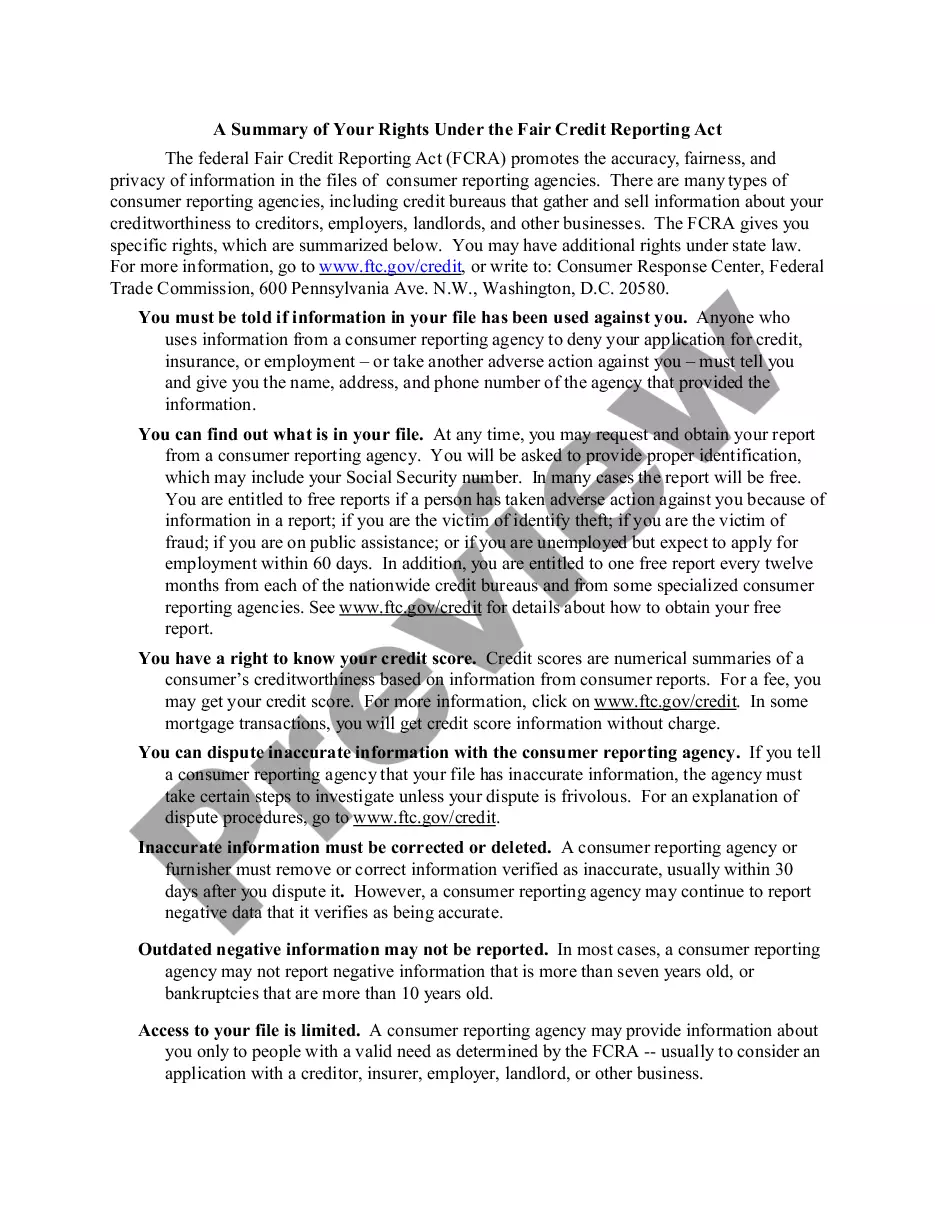

The Fair Credit Reporting Act (FCRA),15 U.S.C. 1681-1681y, requires that this notice be

provided to inform users of consumer reports of their legal obligations. The first section of this summary sets forth the responsibilities imposed by the FCRA on all users of consumer reports. The subsequent sections discuss the duties of users of reports that contain specific types of information, or that are used for certain purposes, and the legal consequences of violations.

Vermont Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA

Instant download

Description

Free preview

How to fill out Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA?

Discovering the right legal document format can be quite a have difficulties. Of course, there are a variety of layouts accessible on the Internet, but how would you discover the legal develop you will need? Take advantage of the US Legal Forms site. The services delivers thousands of layouts, for example the Vermont Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA, that you can use for enterprise and private demands. Every one of the types are examined by specialists and fulfill federal and state demands.

When you are already signed up, log in for your accounts and click the Download button to find the Vermont Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA. Utilize your accounts to check from the legal types you have acquired earlier. Proceed to the My Forms tab of the accounts and obtain one more version of the document you will need.

When you are a brand new consumer of US Legal Forms, allow me to share straightforward recommendations so that you can stick to:

- Very first, make certain you have chosen the right develop to your area/region. You can check out the form while using Review button and look at the form information to ensure this is the right one for you.

- In case the develop fails to fulfill your expectations, make use of the Seach area to get the right develop.

- When you are certain that the form would work, select the Get now button to find the develop.

- Select the rates strategy you would like and type in the necessary information and facts. Make your accounts and purchase the transaction using your PayPal accounts or bank card.

- Opt for the document file format and down load the legal document format for your device.

- Complete, edit and printing and sign the received Vermont Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA.

US Legal Forms is definitely the largest collection of legal types for which you will find various document layouts. Take advantage of the company to down load skillfully-made documents that stick to state demands.

Form popularity

FAQ

Examples of permissible purposes include subpoenas or court orders, written instructions from the consumer, credit transactions with a consumer, employment purposes with written authorization from a consumer, insurance underwriting purposes, tenant screening, and national security investigations.

Under the Fair Credit Reporting Act (FCRA), potential lenders are required to provide you with an adverse action notice when they deny you credit based on information in your credit report.

Their duties include conducting a reasonable investigation of your dispute, correcting any inaccurate information, or even removing the disputed debt from your credit reports. A credit reporting agency or creditor can also fall short of its duties in a number of other ways.

Disclosures to consumers. (a) Every consumer reporting agency shall, upon request and proper identification of any consumer, clearly and accurately disclose to the consumer: (1) The nature and substance of all information (except medical information) in its files on the consumer at the time of the request.

A creditor must notify the applicant of adverse action within: 30 days after receiving a complete credit application. 30 days after receiving an incomplete credit application. 30 days after taking action on an existing credit account.

The FCRA gives you the right to be told if information in your credit file is used against you to deny your application for credit, employment or insurance. The FCRA also gives you the right to request and access all the information a consumer reporting agency has about you (this is called "file disclosure").

Most Frequent Violations of the Fair Credit Reporting Act A user of your information fails to notify you about a negative decision based on your credit report. Failure to notify you of your right to obtain a free credit report. Failure to notify you of the results of an investigation into a debt dispute.

If you take adverse action against a consumer based on information in a consumer report, you must tell the consumer. The most common type of adverse action is a denial of credit. Adverse action is defined in the Equal Credit Opportunity Act and the FCRA to include: a denial or revocation of credit.

The Fair Credit Reporting Act (FCRA) is designed to protect the privacy of consumer report information ? sometimes informally called ?credit reports? ? and to guarantee that information supplied by consumer reporting agencies (CRAs) is as accurate as possible.