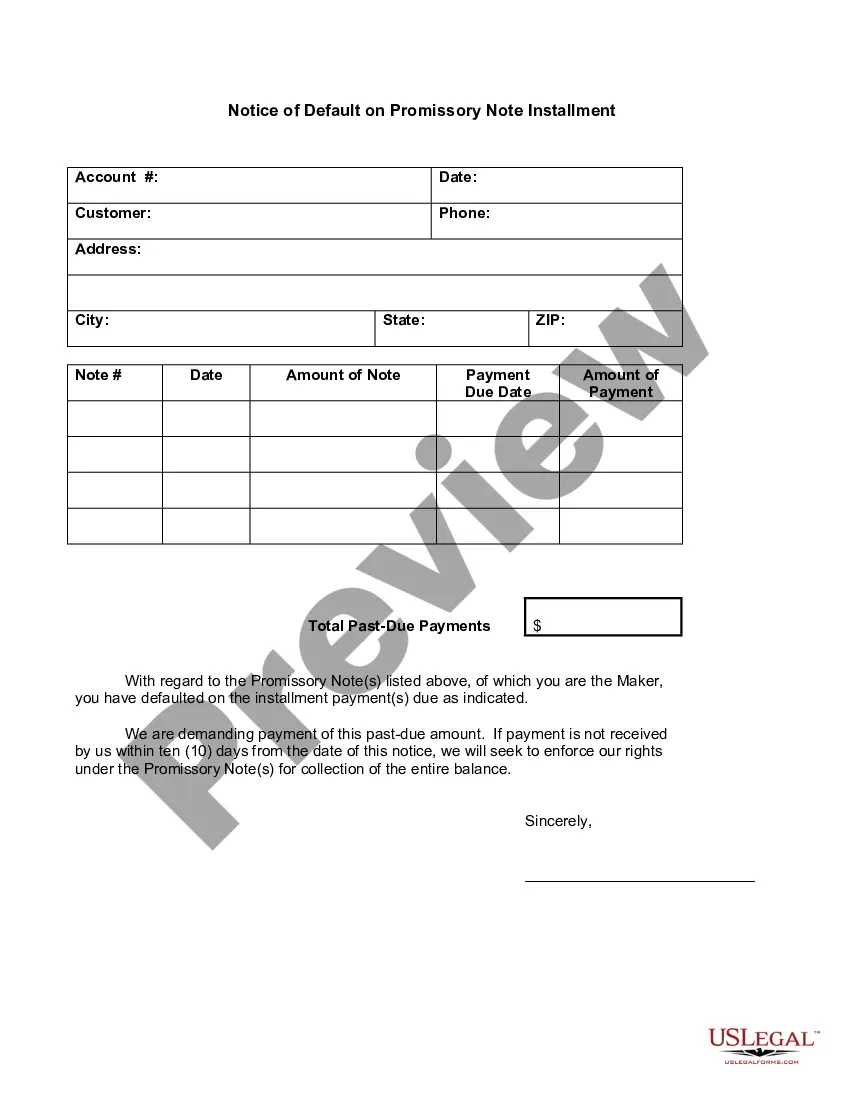

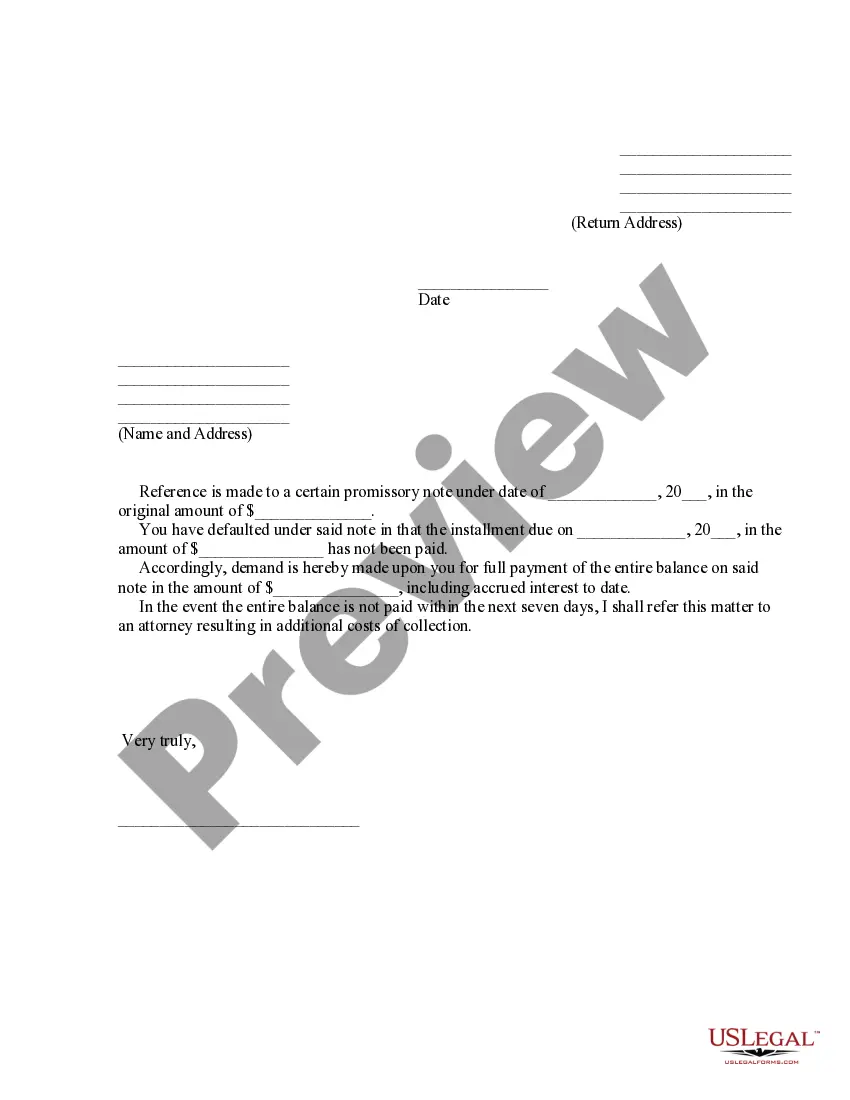

This form is a notice of a failure to make a required payment when due pursuant to a promissory note. The form also contains a warning to the breaching party that legal action will be taken unless the breach is remedied on or before a certain date. This form is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a notice in a particular jurisdiction.

Vermont Notice of Default in Payment Due on Promissory Note

Category:

State:

Multi-State

Control #:

US-01652BG

Format:

Word;

Rich Text

Instant download

Description

How to fill out Notice Of Default In Payment Due On Promissory Note?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a range of legal document templates that you can purchase or print.

By using the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the latest versions of documents such as the Vermont Notice of Default in Payment Due on Promissory Note in moments.

If you currently have a monthly subscription, Log In and obtain the Vermont Notice of Default in Payment Due on Promissory Note from the US Legal Forms collection. The Acquire option will be available on each form you view. You can access all previously downloaded forms from the My documents tab of your account.

Each document you add to your account does not expire and belongs to you indefinitely. So, if you need to download or print another copy, simply go to the My documents section and click on the form you want.

Access the Vermont Notice of Default in Payment Due on Promissory Note with US Legal Forms, one of the most extensive collections of legal document templates. Utilize a vast assortment of professional and state-specific templates that meet your business or personal needs and requirements.

- Ensure you have selected the correct form for your city/state. Click the Review button to check the form's details. Review the form summary to confirm that you selected the right form.

- If the form does not meet your requirements, utilize the Search box at the top of the page to find one that does.

- If you are satisfied with the form, validate your selection by clicking on the Buy now button. Then, choose the payment plan you prefer and provide your information to create an account.

- Process the transaction. Use your credit card or PayPal account to complete the transaction.

- Select the format and download the form on your device.

- Make modifications. Fill out, edit, print, and sign the downloaded Vermont Notice of Default in Payment Due on Promissory Note.

Form popularity

FAQ

A notice of default on a promissory note is a formal notification issued when a borrower fails to make required payments. This document informs the borrower of their default status, typically prompting them to respond or rectify the situation. In Vermont, receiving a Vermont Notice of Default in Payment Due on Promissory Note is a critical step in the legal process of foreclosure.

A promissory note is generally enforceable if it meets specific legal criteria. It must include essential terms such as the amount, payment schedule, and signatures. However, if payments are missed, you may need to issue a Vermont Notice of Default in Payment Due on Promissory Note to assert your legal rights and pursue the debt.

When someone defaults on a promissory note, your first step should be to issue a Vermont Notice of Default in Payment Due on Promissory Note. This notice informs the borrower of their default status and outlines options for remedy. Afterward, assess your next steps, which could include negotiation, restructuring the debt, or initiating foreclosure proceedings.

Yes, you can foreclose on a promissory note if the borrower defaults. Typically, this process begins with a Vermont Notice of Default in Payment Due on Promissory Note, which formally informs the borrower of their missed payments. Following this, you may proceed with foreclosure in accordance with Vermont laws, ensuring all steps are properly documented.

To foreclose on a promissory note, you must first review the terms of your agreement. If the borrower has defaulted, begin by issuing a Vermont Notice of Default in Payment Due on Promissory Note. This document notifies the borrower of their failure to make payments and outlines steps for foreclosure, ensuring you follow the legal process required in Vermont.

When you default on a promissory note, it means you have failed to make a required payment by the due date. In the context of the Vermont Notice of Default in Payment Due on Promissory Note, this default can lead to legal action if the lender decides to enforce their rights. Understanding this process is crucial, as it aids in knowing your obligations and possible repercussions. For those facing this situation, US Legal Forms offers resources to help navigate the complexities of a default.

The timeline for foreclosure in Vermont can vary based on several factors. Generally, the process may take between six months to a year after a Vermont Notice of Default in Payment Due on Promissory Note is issued. Delays can occur due to court schedules, the property's condition, or if the borrower contests the foreclosure. It's essential to stay informed about the process and consider tools like US Legal Forms to help navigate your legal options effectively.

Defaulting on a promissory note, such as receiving a Vermont Notice of Default in Payment Due on Promissory Note, can lead to serious consequences. You may face legal actions from the lender, which could result in court judgments or even foreclosure on secured property. To avoid such situations, consider consulting with a legal expert or using the resources available on USLegalForms to understand your options and rights in dealing with default.