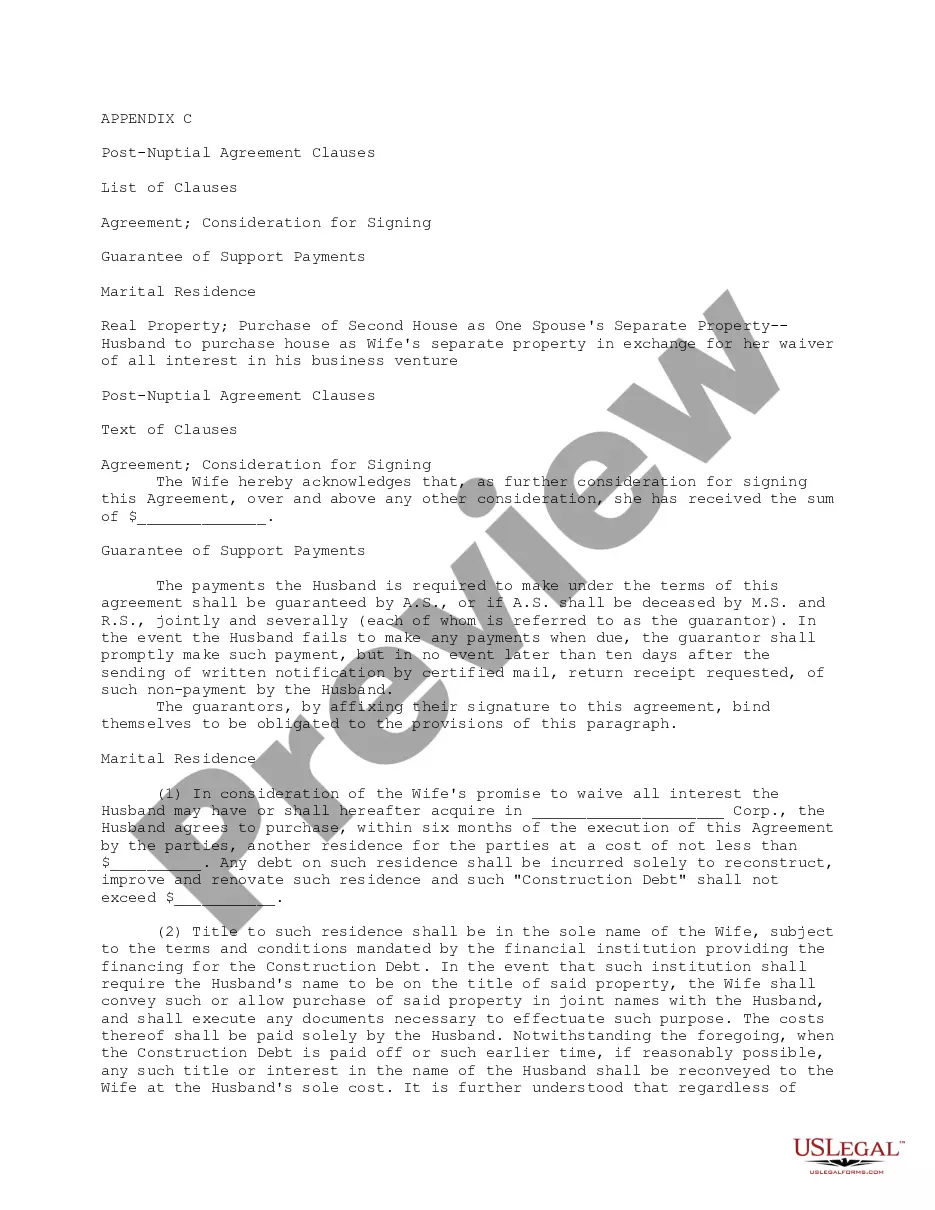

This form is a post-nuptial agreement between husband and wife. A post-nuptial agreement is a written contract executed after a couple gets married, to settle the couple's affairs and assets in the event of a separation or divorce. Like the contents of a prenuptial agreement, it can vary widely, but commonly includes provisions for division of property and spousal support in the event of divorce, death of one of the spouses, or breakup of marriage.

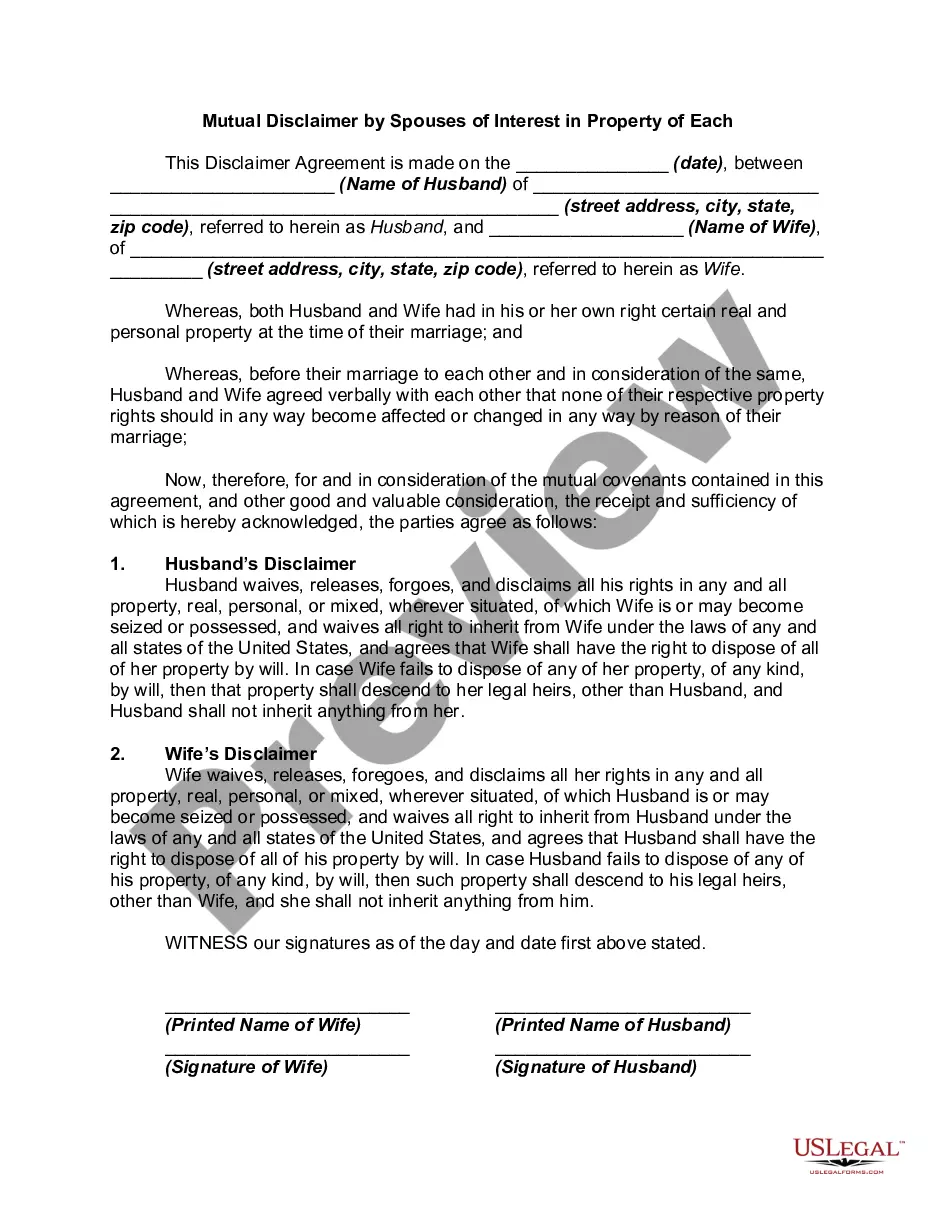

Virgin Islands Spouses' Mutual Disclaimer of Interest in each Other's Property with Provision for Use of Family Residence by one Spouse

Instant download

Description

Free preview

How to fill out Spouses' Mutual Disclaimer Of Interest In Each Other's Property With Provision For Use Of Family Residence By One Spouse?

You have the capacity to spend hours online searching for the authentic document template that meets the state and federal requirements you require.

US Legal Forms offers thousands of legal forms that can be vetted by professionals.

You can easily download or print the Virgin Islands Spouses' Mutual Disclaimer of Interest in Each Other's Property with Provision for Use of Family Residence by one Spouse from the service.

You can obtain and print thousands of document templates using the US Legal Forms site, which offers the largest assortment of legal forms. Utilize professional and state-specific templates to address your business or personal requirements.

- If you already possess a US Legal Forms account, you may Log In and click the Obtain button.

- Next, you can complete, modify, print, or sign the Virgin Islands Spouses' Mutual Disclaimer of Interest in Each Other's Property with Provision for Use of Family Residence by one Spouse.

- Every legal document template you acquire is yours permanently.

- To obtain another copy of a purchased form, visit the My documents tab and click the corresponding button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct document template for the area/city of your choice.

- Read the form description to ensure you have chosen the right form.

Form popularity

FAQ

You're eligible for the exclusion if you have owned and used your home as your main home for a period aggregating at least two years out of the five years prior to its date of sale. You can meet the ownership and use tests during different 2-year periods.

Which of the following rules must be met for a taxpayer to be able to exclude the gain on the sale of a personal residence? A. The taxpayer must have used the property as their principal residence for a total of two or more years during the five year period prior to the sale.

Capital gains should not be more than the investment amount. If only a portion of gains were reinvested, an exemption under capital gain would be applicable only on the amount that was reinvested. Specified assets must be held for at least 36 months.

An NRFC is generally taxable at 25% final withholding tax (FWT) and at 12% final withholding value-added tax (FWVAT). It is vital that you, as the withholding agent, perform your role, as the Bureau of Internal Revenue (BIR) can run after you, and not after the NRFC, to check up on your withholding tax compliance.

A portion of the gain from the sale of a principal residence can be excluded when the taxpayer fails to meet the requirements for full exclusion of gain (i.e., the ownership and use requirements or the one-sale-in-two-years requirement) when the primary reason for selling or exchanging the principal residence was a

As a general rule, wages earned by nonresident aliens for services performed outside of the United States for any employer are foreign source income and therefore are not subject to reporting and withholding of U.S. federal income tax.

The 2-out-of-five-year rule is a rule that states that you must have lived in your home for a minimum of two out of the last five years before the date of sale. However, these two years don't have to be consecutive and you don't have to live there on the date of the sale.

Non-resident citizens and aliens, whether or not resident in the Philippines, are taxed only on income from sources within the Philippines. Rates of tax on income of aliens, resident or not, depend on the nature of their income (i.e. compensation income, income subject to final tax, or other income).

A nonresident alien is an individual who is not a U.S. citizen or a resident alien.

To claim the FEIE you must file Form 2555. You're a government employee Unfortunately, U.S. government employees cannot claim this foreign income exclusion. You failed to calculate the FEIE correctly If you calculate your FEIE incorrectly you won't get the correct amount excluded.