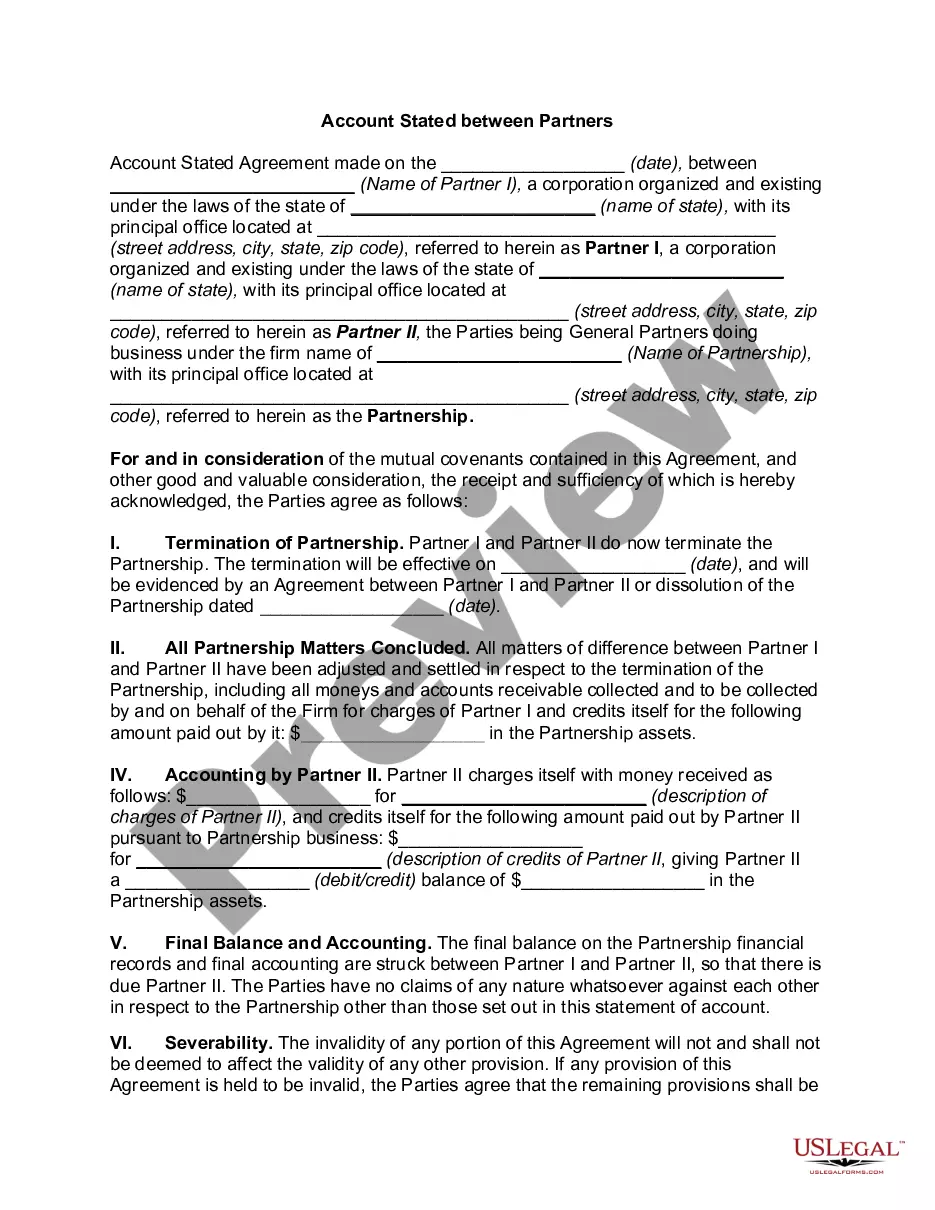

Virginia Account Stated Between Partners and Termination of Partnership

Description

How to fill out Account Stated Between Partners And Termination Of Partnership?

You may invest hours on the Internet attempting to find the legitimate record template that meets the state and federal requirements you will need. US Legal Forms gives a huge number of legitimate forms that are evaluated by professionals. You can actually download or printing the Virginia Account Stated Between Partners and Termination of Partnership from your support.

If you already have a US Legal Forms accounts, you are able to log in and click on the Down load option. After that, you are able to total, revise, printing, or indicator the Virginia Account Stated Between Partners and Termination of Partnership. Every single legitimate record template you purchase is your own property eternally. To have yet another duplicate associated with a bought type, visit the My Forms tab and click on the related option.

If you work with the US Legal Forms website the first time, keep to the simple guidelines below:

- Initial, be sure that you have selected the best record template for that area/town of your liking. See the type description to ensure you have selected the appropriate type. If readily available, take advantage of the Preview option to check throughout the record template too.

- If you wish to locate yet another model of your type, take advantage of the Lookup area to get the template that meets your needs and requirements.

- Once you have identified the template you want, click on Buy now to carry on.

- Select the prices program you want, type your qualifications, and sign up for an account on US Legal Forms.

- Comprehensive the deal. You should use your charge card or PayPal accounts to cover the legitimate type.

- Select the file format of your record and download it to your product.

- Make alterations to your record if possible. You may total, revise and indicator and printing Virginia Account Stated Between Partners and Termination of Partnership.

Down load and printing a huge number of record themes making use of the US Legal Forms website, that provides the largest collection of legitimate forms. Use professional and express-particular themes to take on your small business or specific demands.

Form popularity

FAQ

When a partnership dissolves, the individuals involved are no longer partners in a legal sense, but the partnership continues until all debts are settled, the legal existence of the business is terminated and the remaining assets of the company have been distributed.

Ending a partnership can feel like ending a marriage ? and become just as complicated and contentious. It's always preferable to have a partnership agreement in place that details an exit strategy. But when one doesn't exist, a skilled business advisor can help guide you through the process.

This happens when all of its operations are truly discontinued and no part of the business is carried on by any of its partners. When this happens, the partnership has to dissolve and cease being a partnership for state law purposes. Its assets must be liquidated, so its debts can be paid.

Your Secretary of State's office or website should have information on the process of partner dissolution, any relevant termination fees and required forms. File a statement of dissolution with your state. This process can take up to 90 days. Notify all of your customers, clients and suppliers directly.

The limited partnership's termination involves the same three steps as in a general partnership: (1) dissolution, (2) winding up, and (3) termination.

While both words are concerned with the end of a business partnership, dissolution refers to the process itself, and usually to the departure (or death) of one or more individuals from the entity, while termination refers to the cessation of all operations, including the disposal of all assets.

A deed of dissolution of partnership sets out the terms on which the partners of a partnership agree to dissolve the partnership.

5 Key Steps in Dissolving a Partnership Review your partnership agreement. While some partnerships don't require a formal or written agreement, most partners choose to have one anyway for protection. ... Discuss with other partners. ... File dissolution papers. ... Notify others. ... Settle and close out all accounts.