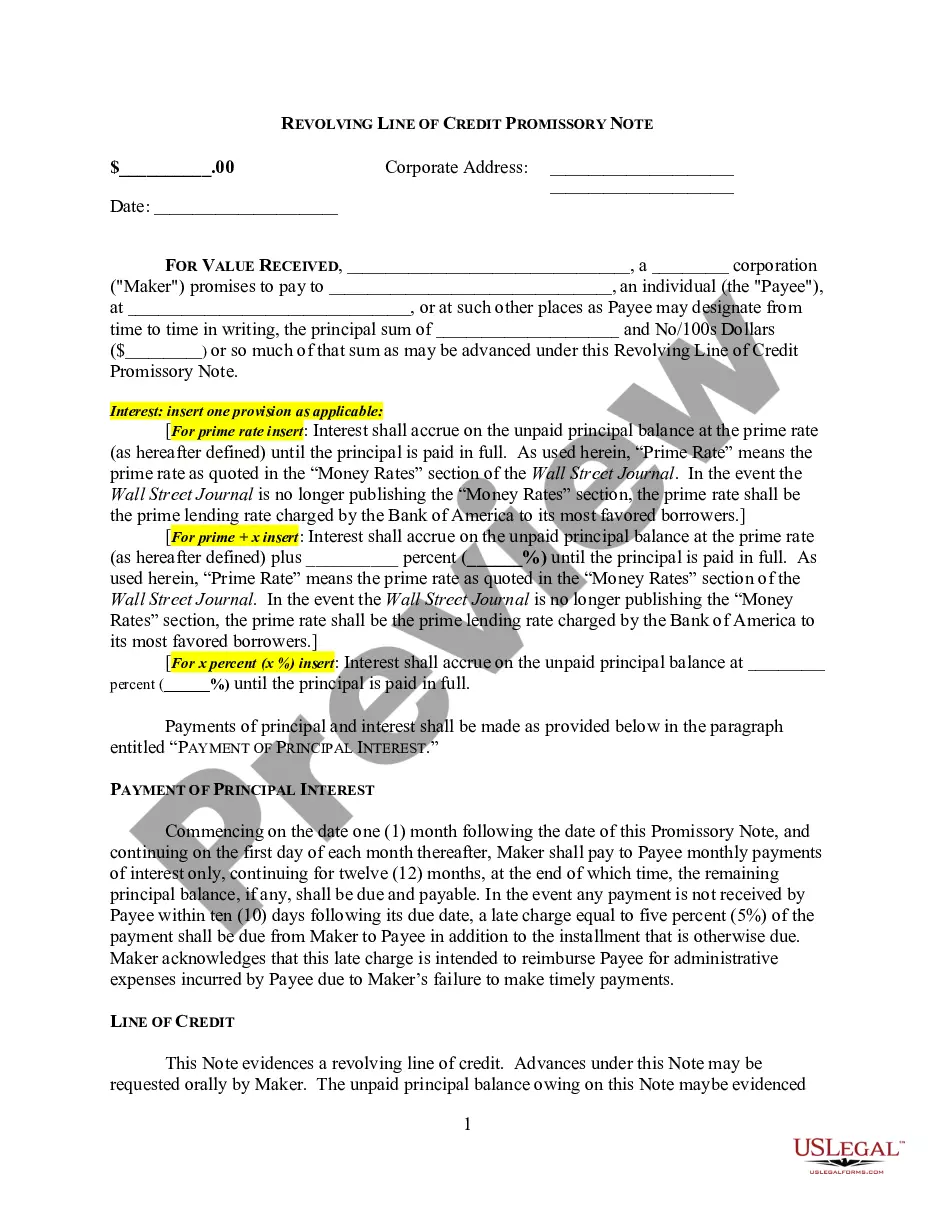

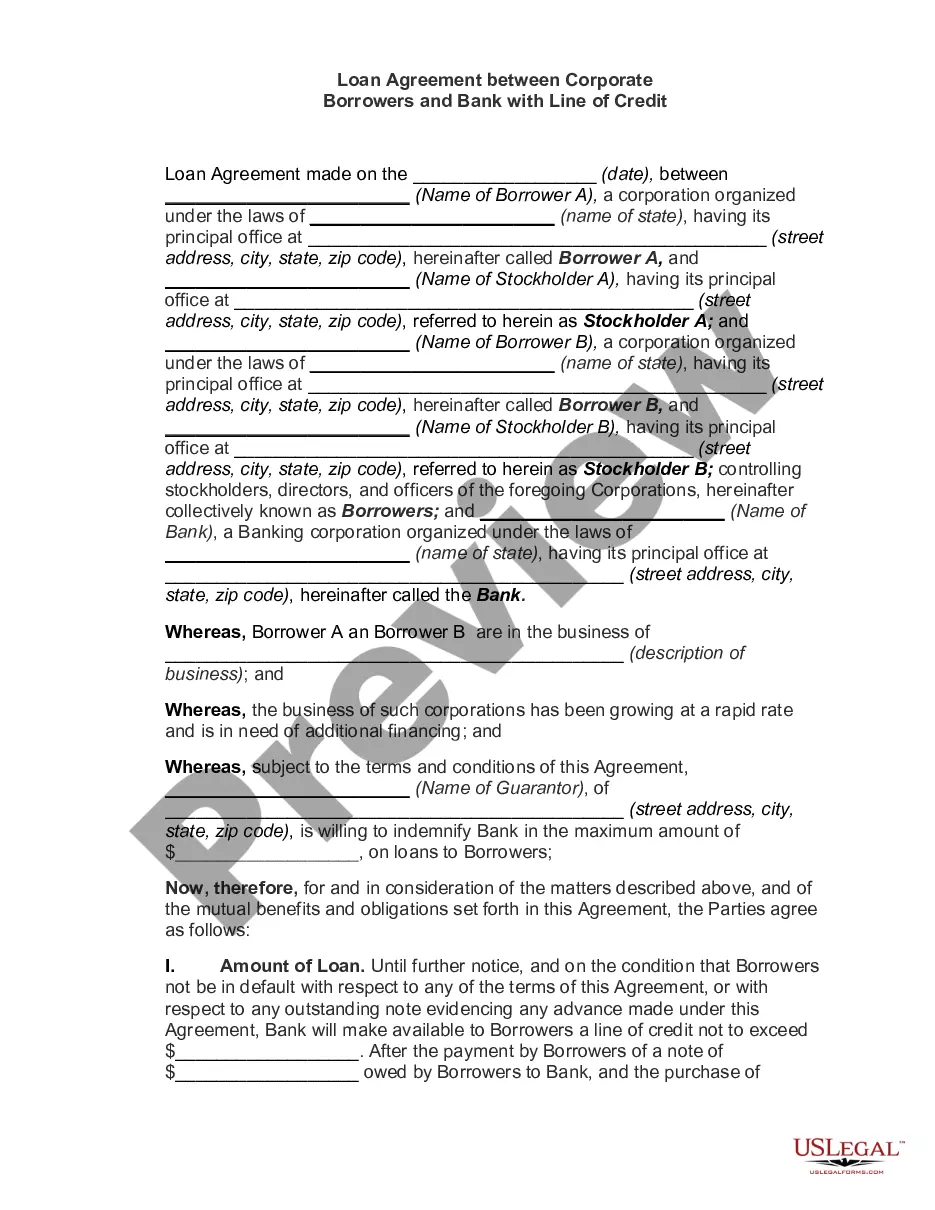

This form is a secured Line of Credit Promissory Note. The form provides that the borrower will repay all sums to the lender, with interest. The agreement also provides that if the borrower defaults, the lender may declare that the entire balance is immediately due.

Virginia Line of Credit Promissory Note

Category:

State:

Multi-State

Control #:

US-01776-NT

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Line Of Credit Promissory Note?

Have you been in a position in which you need files for possibly enterprise or specific purposes almost every day time? There are a lot of authorized record themes accessible on the Internet, but getting versions you can rely on isn`t effortless. US Legal Forms provides a huge number of develop themes, much like the Virginia Line of Credit Promissory Note, which can be composed to meet federal and state specifications.

In case you are presently informed about US Legal Forms website and also have an account, simply log in. After that, you may obtain the Virginia Line of Credit Promissory Note design.

If you do not offer an bank account and want to begin using US Legal Forms, follow these steps:

- Obtain the develop you want and make sure it is to the correct area/area.

- Utilize the Preview button to check the form.

- Read the outline to actually have chosen the right develop.

- If the develop isn`t what you are seeking, take advantage of the Search discipline to discover the develop that fits your needs and specifications.

- If you discover the correct develop, click on Buy now.

- Choose the pricing prepare you need, complete the desired information to generate your bank account, and pay money for the order making use of your PayPal or credit card.

- Pick a practical document structure and obtain your backup.

Locate all of the record themes you have bought in the My Forms menu. You can get a additional backup of Virginia Line of Credit Promissory Note anytime, if necessary. Just select the essential develop to obtain or print out the record design.

Use US Legal Forms, by far the most extensive selection of authorized forms, to save lots of time and prevent faults. The support provides professionally manufactured authorized record themes that can be used for a range of purposes. Generate an account on US Legal Forms and initiate creating your way of life easier.

Form popularity

FAQ

Promissory notes may also be referred to as an IOU, a loan agreement, or just a note. It's a legal lending document that says the borrower promises to repay to the lender a certain amount of money in a certain time frame. This kind of document is legally enforceable and creates a legal obligation to repay the loan.

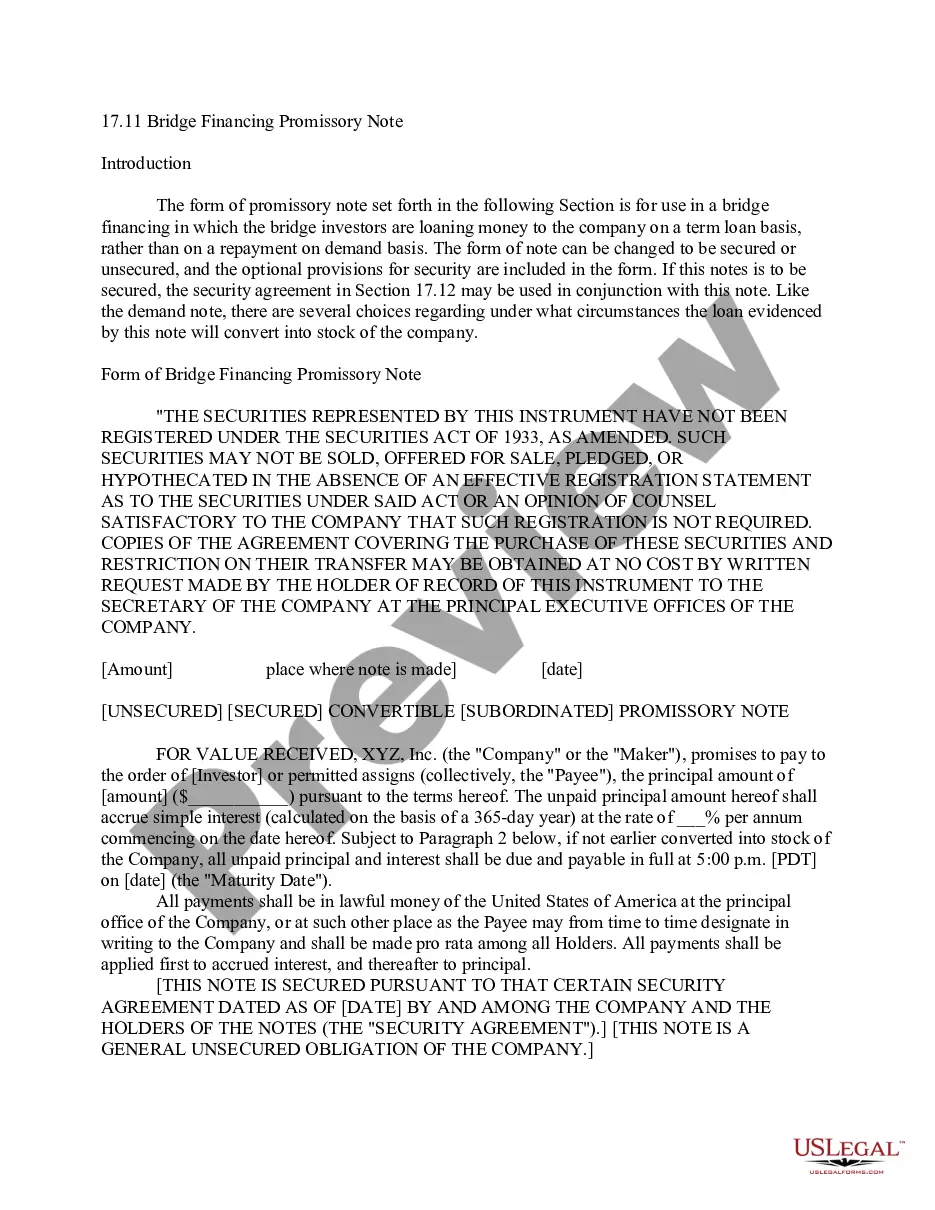

A form of promissory note to be used to evidence advances under an uncommitted line of credit when the lender uses a line of credit confirmation letter instead of a separate line of credit agreement and the parties are not contemplating a negotiable instrument.

A form of debt instrument, a promissory note represents a written promise on the part of the issuer to pay back another party.

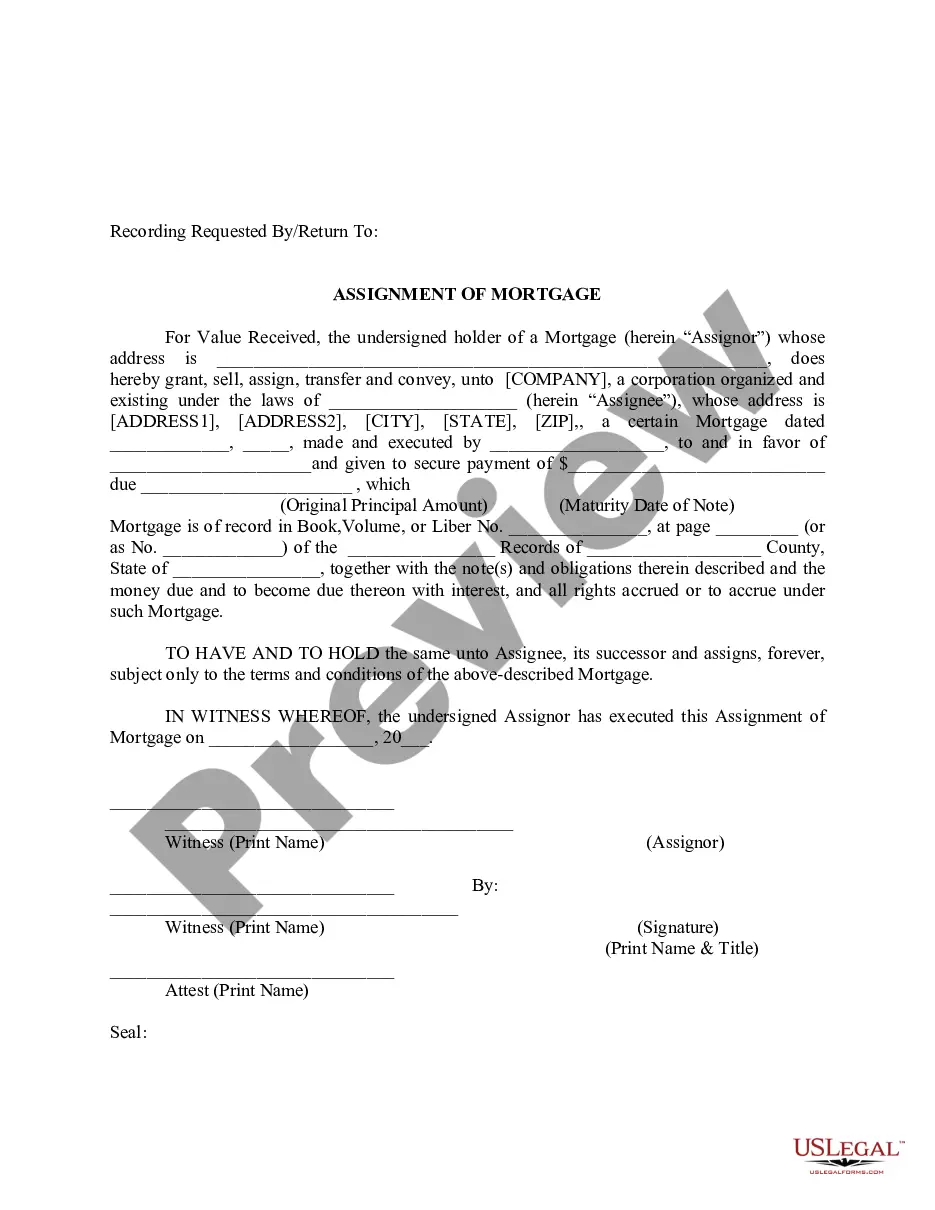

Unlike a deed of trust or mortgage, the promissory note is typically not recorded in the county land records (except in a few states like Florida). Instead, the lender holds on to this document until the amount borrowed is repaid.

Promissory Notes and Your Credit Reports However, only traditional lenders and investment firms typically report such information to credit reporting agencies. Therefore, information about a promissory note may never appear on your credit reports.

Although it is legally enforceable, a promissory note is less formal than a loan agreement and is suitable where smaller sums of money are involved. However, its terms - which can include a specific date of repayment, interest rate and repayment schedule - are more certain than those of an IOU.

These payments are subject to taxation. Also, whenever interest is earned, paid, or forgiven on a promissory note, it will affect income tax for both lenders and borrowers. Estate Tax: The value of inherited promissory notes is typically included in the estate and is subject to estate taxation rules.

Reporting to a Credit Bureau Is an Involved Process A promissory note default can affect a borrower's credit rating if the promissory note holder has the ability to report the deficiency to the various credit reporting agencies.

Rule #5 - In order to pay off the debt, or what is called "discharging the debt"; all one has to do is write/ (or create) your own certified promissory note (a negotiable instrument under Uniform Commercial Code (UCC) Section 3- 104 paragraph (e)), with your signature on the promissory note in the amount of the ...

Promissory notes may also be referred to as an IOU, a loan agreement, or just a note. It's a legal lending document that says the borrower promises to repay to the lender a certain amount of money in a certain time frame. This kind of document is legally enforceable and creates a legal obligation to repay the loan.