Virginia Installments Fixed Rate Promissory Note Secured by Commercial Real Estate

Overview of this form

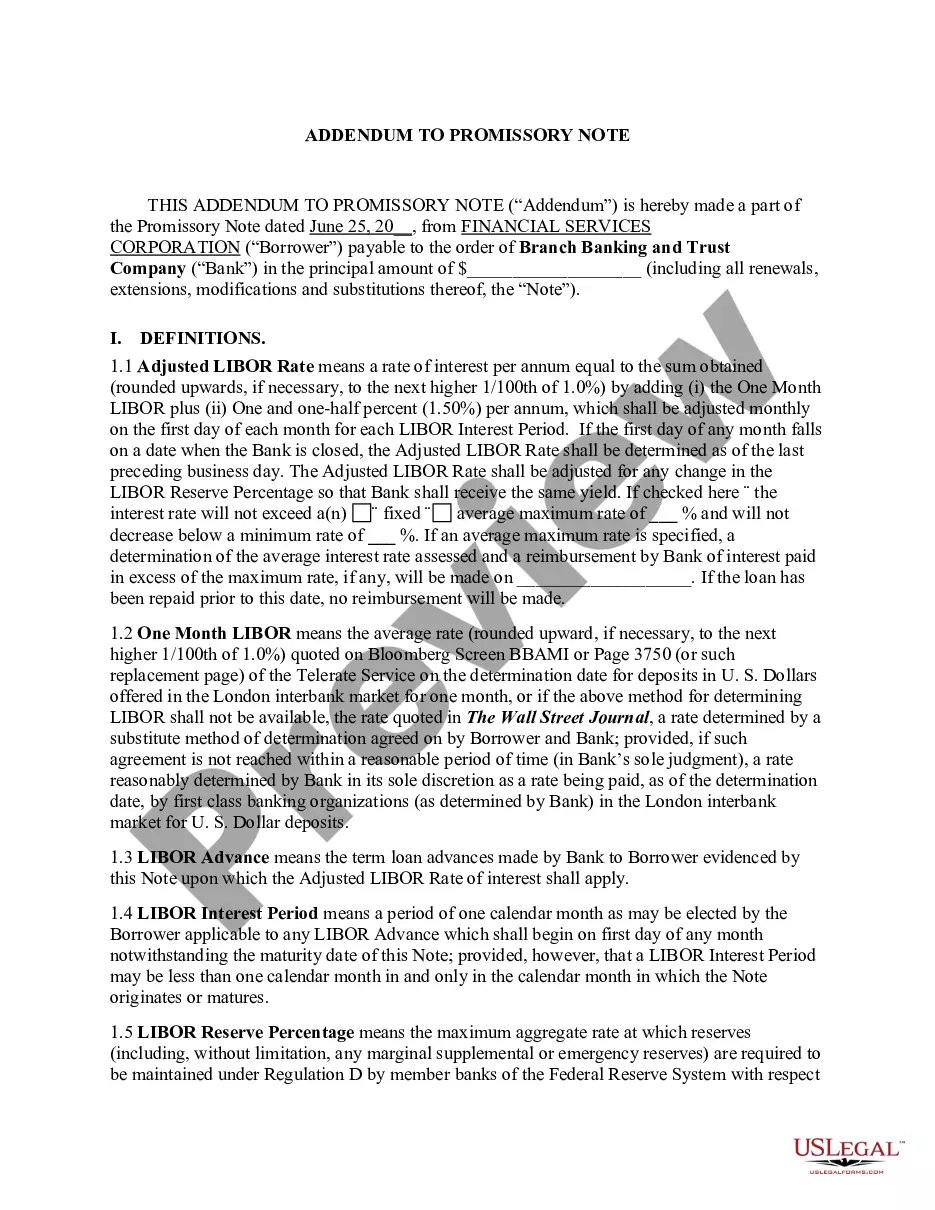

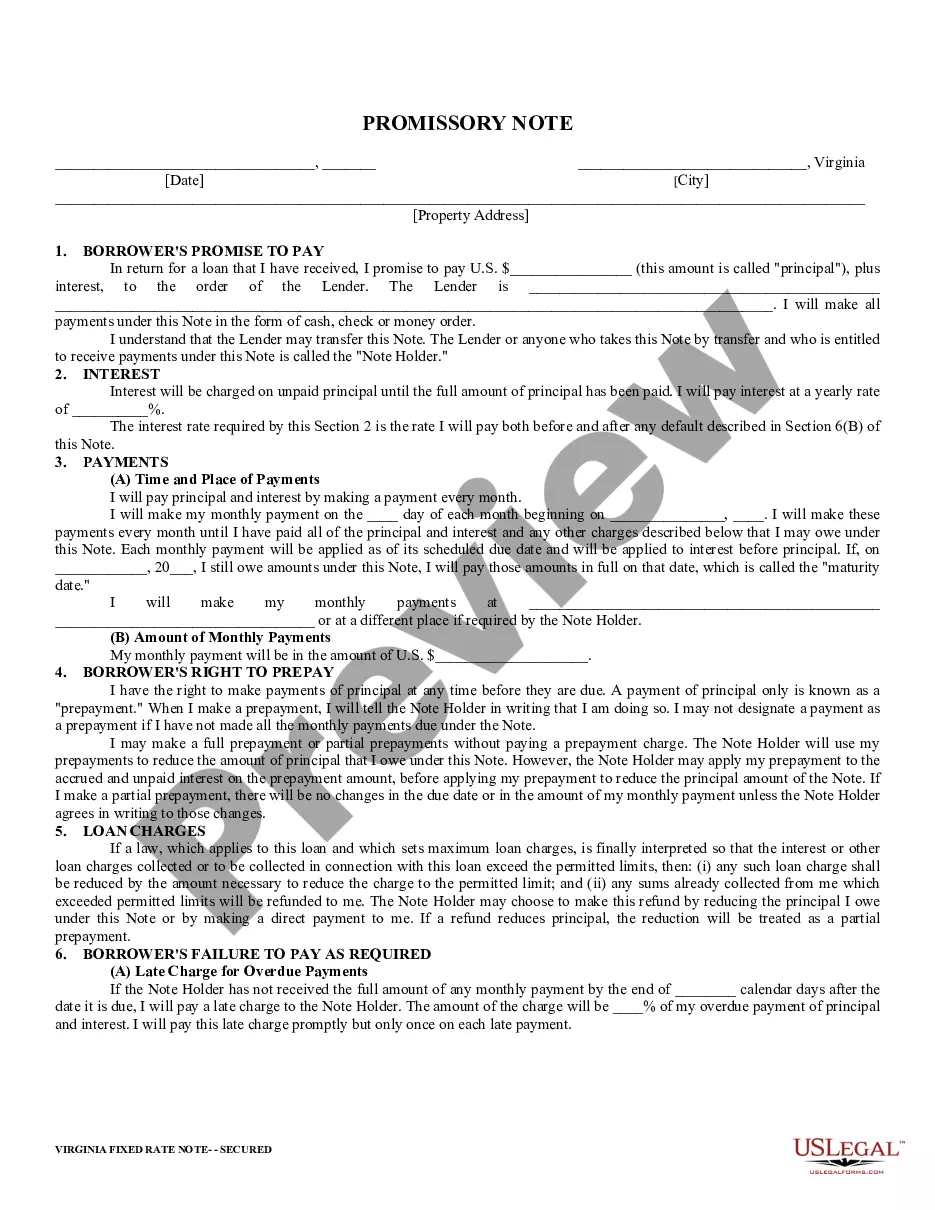

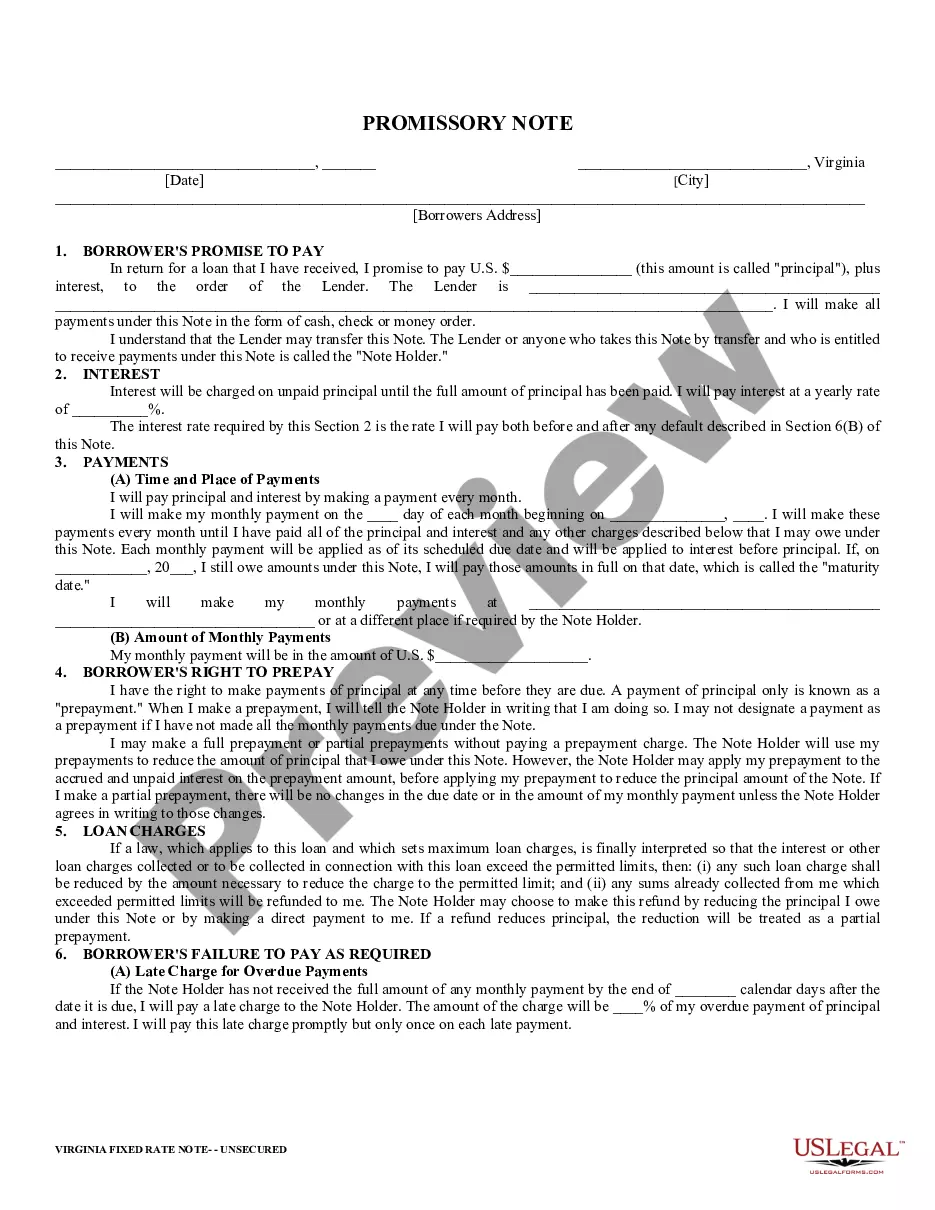

The Virginia Installments Fixed Rate Promissory Note Secured by Commercial Real Estate is a legal document used to outline the terms of a loan secured by commercial property. This form specifies the borrower's promise to repay the amount borrowed, detailing the principal and interest rates, payment schedule, and the repercussions of default. Unlike unsecured promissory notes, this form provides lenders with the assurance that they have a claim to the property should the borrower fail to meet their obligations.

Key parts of this document

- Borrowerâs promise to pay the principal amount plus interest.

- Details of the interest rate and how it is applied.

- Schedule for monthly payments and maturity date.

- Rights regarding prepayment and related penalties.

- Procedures for addressing late payments and defaults.

- Secured nature of the note via a mortgage or deed of trust.

When to use this form

This form is relevant when an individual or entity is borrowing money and intends to use commercial real estate as collateral. It should be utilized when the terms of the loan include a fixed interest rate and structured payments over time. For example, if a business owner needs to finance property renovations or expansion and seeks to secure the loan against the real estate, this promissory note is the appropriate document to use.

Intended users of this form

- Business owners looking for financing secured by commercial property.

- Individuals involved in real estate transactions requiring formal loan agreements.

- Lenders, including banks or private investors, providing loans against commercial real estate.

- Any parties needing a clear record of the loan terms for legal purposes.

How to prepare this document

- Fill in the date and the full legal names of the borrower(s).

- Specify the principal loan amount and the interest rate.

- Detail the monthly payment amount and the payment schedule.

- Select a prepayment option and include initial next to the chosen provision.

- Provide the borrower's address, including city, state, and zip code.

- Ensure the form is signed and dated by the borrower(s) and notarized if required.

Does this document require notarization?

Yes, this form must be notarized to be legally valid. US Legal Forms offers integrated online notarization services that are available 24/7, allowing you to complete the notarization securely via video call without the need for travel.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to read the terms thoroughly before signing.

- Not filling in all required fields, such as loan amount and interest rate.

- Assuming that prepayment terms are flexible without confirming details with the lender.

- Overlooking the necessity of notarization if required by state law.

Benefits of using this form online

- Convenience of immediate access to legal documentation.

- Editable fields allow customization according to specific needs.

- Reliability provided by templates drafted by licensed attorneys.

- Easy download options for quick retrieval and storage.

Looking for another form?

Form popularity

FAQ

What Is a Promissory Note? A promissory note is a financial instrument that contains a written promise by one party (the note's issuer or maker) to pay another party (the note's payee) a definite sum of money, either on demand or at a specified future date.

Whether a promissory note is a security is one of the most vexatious issues in US securities laws.In general, under the Securities Acts, promissory notes are defined as securities, but notes with a maturity of 9 months or less are not securities.

When a loan changes hands, the promissory note is endorsed (signed over) to the new owner of the loan. In some cases, the note is endorsed in blank which makes it a bearer instrument under Article 3 of the Uniform Commercial Code. So, any party that possesses the note has the legal authority to enforce it.

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

The individual who promises to pay is the maker, and the person to whom payment is promised is called the payee or holder. If signed by the maker, a promissory note is a negotiable instrument.

A promissory note can be secured with a pledge of collateral, which is something of value that can be seized if a borrower defaults.

A promissory note is a contract, a binding agreement that someone will pay your business a sum of money. However under some circumstances if the note has been altered, it wasn't correctly written, or if you don't have the right to claim the debt then, the contract becomes null and void.

Promissory notes are a valuable legal tool that any individual can use to legally bind another individual to an agreement for purchasing goods or borrowing money. A well-executed promissory note has the full effect of law behind it and is legally binding on both parties.

The lender holds the promissory note while the loan is being repaid, then the note is marked as paid and returned to the borrower when the loan is satisfied. Promissory notes aren't the same as mortgages, but the two often go hand in hand when someone is buying a home.