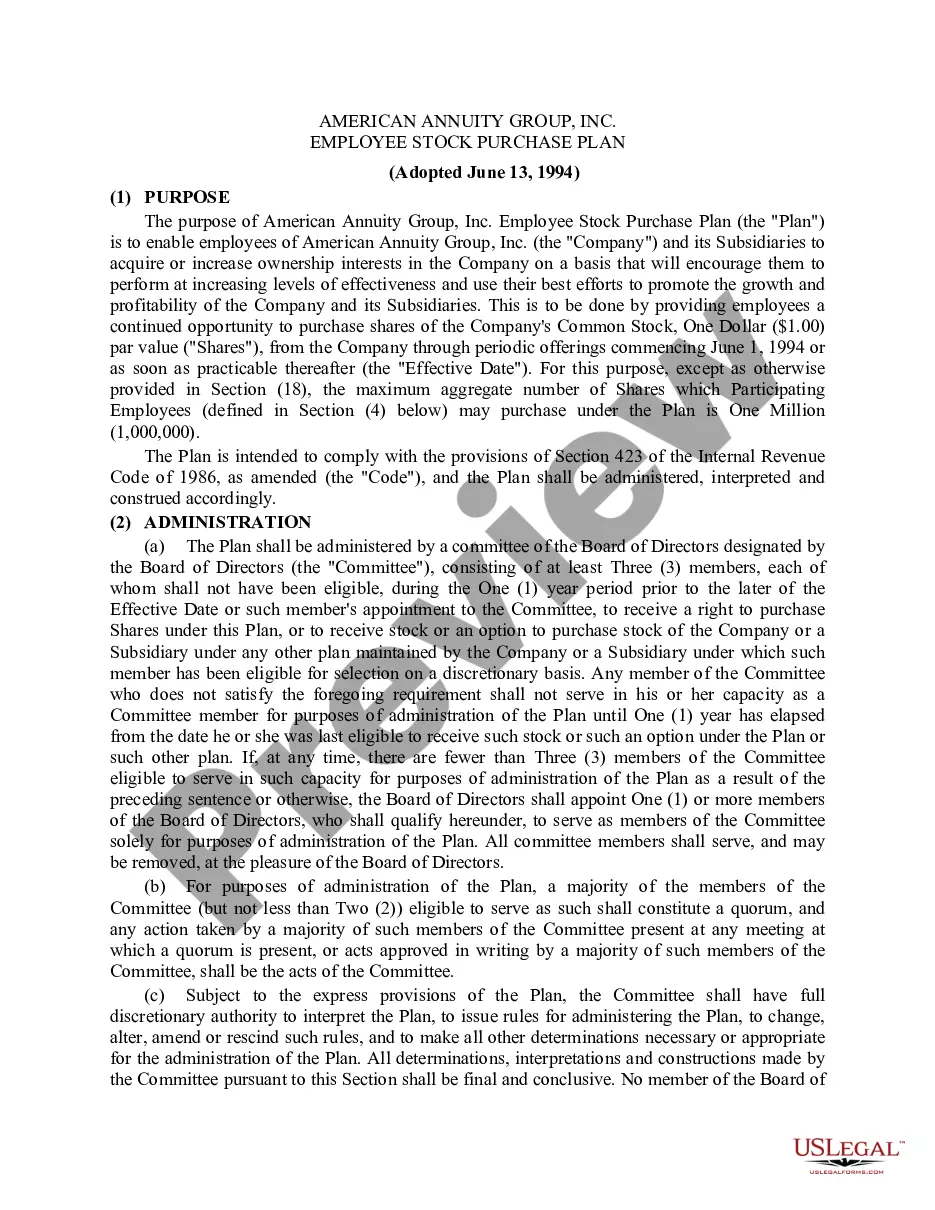

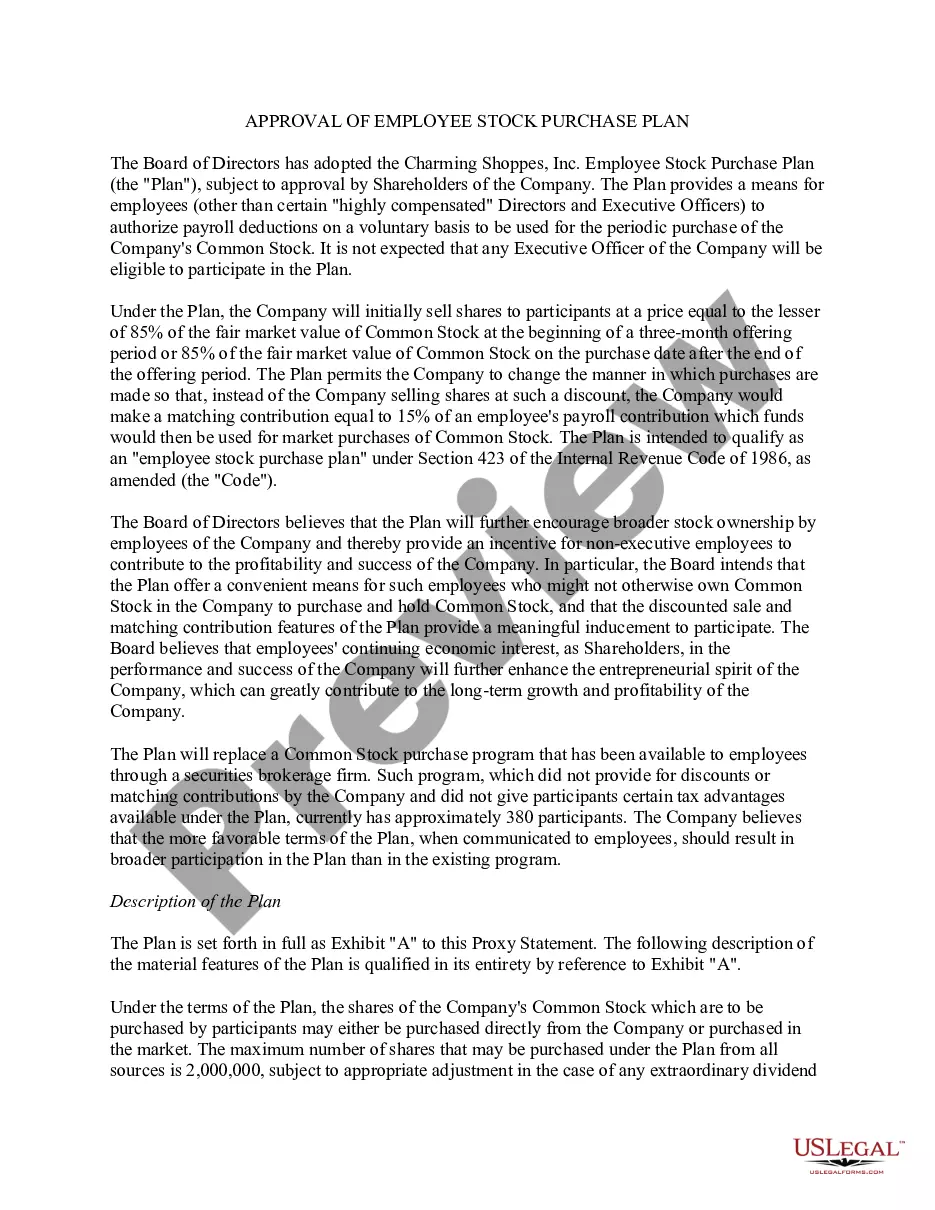

19-119 19-119 . . . Employee Stock Purchase Plan under which each employee can contribute from 1% to 10% of earnings through payroll deductions, and contributions are credited to account maintained on behalf of each employee by brokerage firm designated as custodian under Plan. So long as Plan is operated as "discount plan", corporation will sell shares directly to custodian at a price equal to lesser of 85% of fair market value of common stock at beginning of offering period or 85% of fair market value of common stock on purchase date. If Board designates Plan as a "matching plan", such discounted sales by corporation would be discontinued, but corporation instead would make matching contribution equal to 15% of employees' payroll contributions to be used by custodian to make market purchases of common stock at or promptly after purchase date

Utah Employee Stock Purchase Plan of Charming Shoppes, Inc.

Category:

State:

Multi-State

Control #:

US-CC-19-119

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Employee Stock Purchase Plan Of Charming Shoppes, Inc.?

US Legal Forms - one of the greatest libraries of legitimate types in the USA - gives a variety of legitimate record layouts you may down load or print out. Using the website, you will get a large number of types for enterprise and personal functions, sorted by types, suggests, or keywords and phrases.You can get the most recent variations of types just like the Utah Employee Stock Purchase Plan of Charming Shoppes, Inc. within minutes.

If you currently have a monthly subscription, log in and down load Utah Employee Stock Purchase Plan of Charming Shoppes, Inc. through the US Legal Forms catalogue. The Acquire switch can look on every single type you look at. You have accessibility to all previously delivered electronically types in the My Forms tab of your own bank account.

If you want to use US Legal Forms initially, here are easy recommendations to get you started:

- Ensure you have picked out the right type for your personal area/state. Click the Review switch to examine the form`s information. Read the type explanation to ensure that you have selected the appropriate type.

- In case the type does not suit your requirements, utilize the Search area on top of the display screen to get the one that does.

- In case you are content with the shape, affirm your selection by visiting the Purchase now switch. Then, opt for the costs program you like and offer your qualifications to sign up for the bank account.

- Process the purchase. Make use of your credit card or PayPal bank account to accomplish the purchase.

- Choose the format and down load the shape in your device.

- Make modifications. Fill up, change and print out and indicator the delivered electronically Utah Employee Stock Purchase Plan of Charming Shoppes, Inc..

Each and every template you included in your bank account lacks an expiration day and it is yours eternally. So, in order to down load or print out another version, just proceed to the My Forms area and click on in the type you need.

Gain access to the Utah Employee Stock Purchase Plan of Charming Shoppes, Inc. with US Legal Forms, one of the most considerable catalogue of legitimate record layouts. Use a large number of professional and status-certain layouts that fulfill your organization or personal needs and requirements.

Form popularity

FAQ

Employees who elect to participate in a qualified ESPP are typically able to take advantage of some tax benefits, as the discount is not recognized as taxable income until the stock is sold. When you sell the stock, the discount you received when you bought it may be taxable as income.

The ESOP vs 401K Plan With a 401(k), the employer's contributions are tax-deferred, meaning that the money is taken out of each paycheck before taxes, and those wages are not taxed until withdrawal. Whereas with an ESOP, employees also do not pay taxes on the shares in their account until distribution.

In this situation, you sell your ESPP shares more than one year after purchasing them, but less than two years after the offering date. This is a disqualifying disposition because you sold the stock less than two years after the offering (grant) date.

Disadvantages of Employee Stock Purchase Plans Ensuring the ESPP follows security and tax law guidelines can be challenging. A large amount of HR functions goes into administering the stock purchase plan. There are legal, tax, and administrative issues that go into setting up the plan.

A: Yes. You may withdraw from the ESPP by notifying Fidelity and completing a withdrawal election. When you withdraw, all of the contributions accumulated in your account will be returned to you as soon as administratively possible and you will not be able to make any further contributions during that offering period.

How much should I put in an employee stock purchase plan? You can contribute 1% to 15% of your salary, up to the $25,000 IRS limit per calendar year. The more disposable income you have, the more you can afford to put in an employee stock purchase plan. Employees contribute through payroll deductions.

An employee stock purchase plan (or ESPP) can be a very valuable benefit. In general, if your employer offers an ESPP, we think you should participate at the level you can comfortably afford and then sell the shares as soon as you can.

An ESPP is a program in which employees can purchase company stock at a discounted price. Income or loss from the sale of shares you purchased through an ESPP is generally taxed as a capital gain or loss, though there are holding period requirements.