The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use.

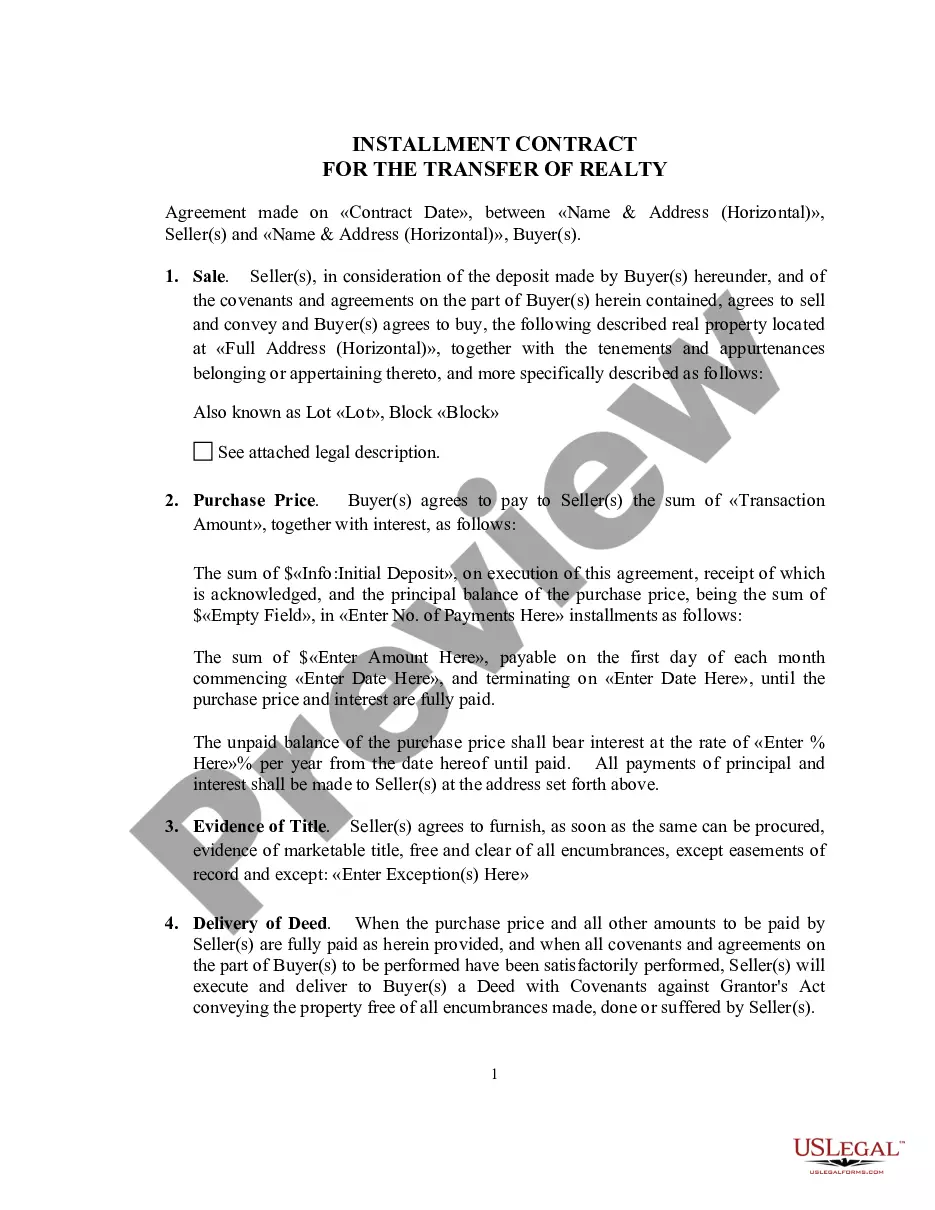

Closed-end transactions involve a fixed amount to be paid back over a period of time such as a note or a retail installment contract.

Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Category:

State:

Multi-State

Control #:

US-02514BG

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures?

If you desire to finalize, acquire, or create lawful document templates, utilize US Legal Forms, the most extensive collection of legal forms available online.

Employ the site's straightforward and user-friendly search feature to locate the documents you require. Various templates for corporate and personal purposes are organized by categories and states, or keywords.

Utilize US Legal Forms to find the Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures within a few clicks.

Step 5. Process the transaction. You may use your credit card or PayPal account to complete the payment.

Step 6. Choose the format of the legal form and download it to your device. Step 7. Fill out, modify, and print or sign the Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

- If you are presently a US Legal Forms member, Log In to your account and click on the Download button to obtain the Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

- You may also access forms you previously saved from the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the steps below.

- Step 1. Ensure you have selected the form for the appropriate city/state.

- Step 2. Use the Preview option to review the form's details. Remember to read through the information.

- Step 3. If you are dissatisfied with the form, utilize the Search area at the top of the screen to find other templates in the legal form template.

- Step 4. After you have located the form you need, click on the Purchase now button. Choose the pricing plan you prefer and enter your details to register for an account.

Form popularity

FAQ

For open-end loans, such as lines of credit, specific disclosures must include details about the terms of the credit, including interest rates and fees. While the focus here is on Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, it's essential to note that open-end loans demand additional clarity. Consumers should understand the ongoing costs and repayment terms to make informed decisions. Clear disclosures enable better financial planning and management.

Contract disclosures must be provided to the consumer at the time of the transaction or before they finalize the agreement. It's crucial that consumers receive these Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures in a clear and timely manner. This allows them to fully understand the terms, conditions, and costs involved. By ensuring transparency in disclosure, you enhance trust in the lending process.

Under the Truth in Lending Act, lenders must disclose critical information clearly and concisely. This includes the annual percentage rate (APR), finance charges, payment schedule, and total costs to the borrower. These disclosures aim to provide transparency to consumers, ensuring they understand the terms of credit. If you need information about Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, USLegalForms can help simplify the process.

The Truth in Lending Act primarily targets consumer credit, so it does not apply to commercial loans. This regulation focuses on transactions made for personal, family, or household purposes. Therefore, if you're seeking information about Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, keep in mind that these standards do not extend to commercial lending. For more insights tailored to your needs, consider exploring options on the USLegalForms platform.

If you suspect a violation of the Truth in Lending Act, the first step is to gather all relevant documentation related to the alleged violation. Next, you may consider contacting the lender to discuss the issue directly. If the situation does not resolve, filing a complaint with the Consumer Financial Protection Bureau (CFPB) is often an effective way to seek redress. An experienced platform like uslegalforms can provide templates for formal complaints to address these issues.

Under the Truth in Lending Act, retail businesses must provide clear and understandable disclosures regarding credit terms. This includes detailing the annual percentage rate, payment terms, and total costs of credit, ensuring customers make informed decisions. Adhering to the Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures helps businesses uphold transparency and improve customer trust.

Utah Code 70C 2 101 addresses the definitions and scope related to consumer credit agreements. It lays the groundwork for understanding the rights and responsibilities of both lenders and borrowers. Compliance with this code is essential as it relates directly to the Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

Utah Code 70C 3 101 details the requirements for servicing consumer credit transactions. It includes crucial provisions that protect consumers and ensure they receive accurate information about their loans. This section complements the Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, underscoring the importance of transparency in lending practices.

In Utah, aggravated kidnapping is a serious offense that can result in severe penalties. The law specifies that a conviction for aggravated kidnapping may lead to a minimum prison sentence of 15 years. While this topic is not directly related to the Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, understanding legal implications is vital for everyone.

The Commercial Financing Registration and Disclosure Act is designed to regulate commercial financing options in Utah. It requires lenders to register and provide transparent disclosures about their financing products. By adhering to the Act, businesses can ensure they meet the Utah General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.