Term Loan Agreement

Understanding this form

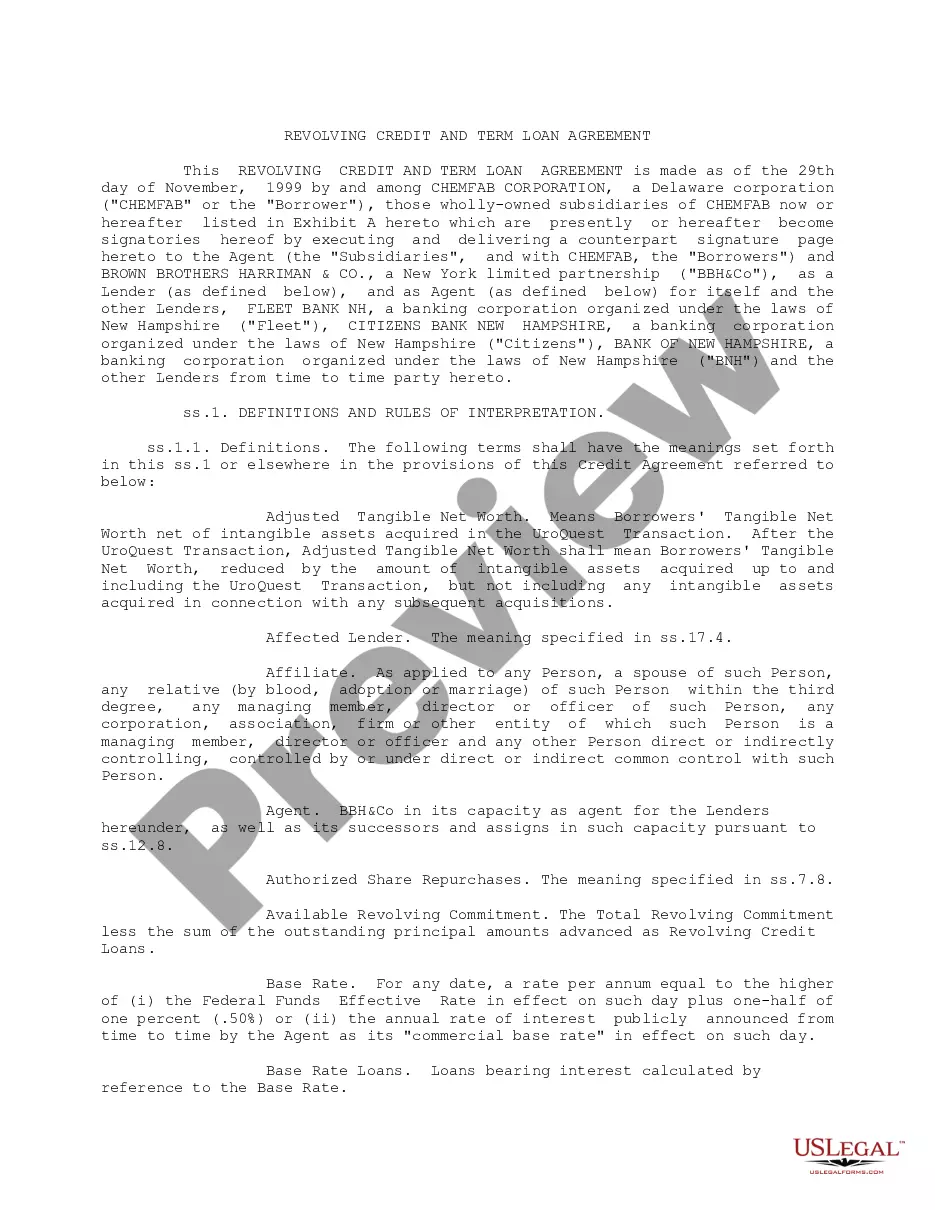

The Term Loan Agreement is a legal document that outlines the terms and conditions under which a borrower receives a loan from one or more lenders. This specific modification, known as the First Modification of Amended and Restated Term Loan Agreement, allows for adjustments to an existing loan agreement, such as changes to the loan amount, payment schedule, and parties involved. It is essential for those who need to amend a previously established loan deal, differentiating it from initial loan agreements, which serve as the original contract for borrowing funds.

- Parties involved: Identification of the borrower, lenders, and the agent managing the loan.

- Amendments to terms: Specific changes to the loan amount and repayment conditions.

- Payment provisions: Instructions on how and when payments must be made.

- Representations and warranties: Assurances provided by the borrower regarding their capacity to enter the agreement.

- Conditions precedent: Requirements that must be fulfilled for the modification to be effective.

When to use this form

This form should be used when a borrower and lender agree to modify existing loan terms. Common situations for this include adjusting payment amounts, altering the interest rate, or changing the due dates. It is also relevant when new lenders are involved in an existing loan agreement, ensuring that all parties are aware of their rights and obligations after the modification.

Who this form is for

Eligible users of this form include:

- Borrowers who need to revise existing loan agreements.

- Lenders seeking to update terms in response to changing financial circumstances.

- Businesses involved in loan agreements that require modifications for growth, refinancing, or restructuring.

- Financial institutions providing loans and needing to formalize amendments.

Completing this form step by step

To complete this form, follow these steps:

- Identify all parties involved, including the borrower, existing lenders, and new lenders.

- Clearly state the amendments to be made to the loan agreement, including new loan amounts and terms.

- Provide accurate payment details, including specific due dates and amounts.

- Include any necessary certifications, resolutions, and approvals from involved parties.

- Ensure all parties sign and date the document to validate the modification.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, it is advisable to verify local regulations to ensure compliance. US Legal Forms provides integrated online notarization options for added convenience, allowing users to complete the process securely via video call, twenty-four hours a day.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

- Failing to include all necessary parties in the agreement.

- Neglecting to update payment provisions correctly according to the new terms.

- Not obtaining the required approvals or corporate authorizations from all entities involved.

- Disregarding the need for signatures from all parties to formalize the modification.

Advantages of online completion

- Using this form online allows for easy access to standard legal language and formats.

- The document can be quickly customized to fit specific needs, ensuring accuracy.

- It provides a reliable way to amend loan agreements with built-in legal protections.

- Users can save time and avoid potential legal pitfalls with professional templates.

Legal use & context

- The form serves as a binding agreement between parties, enforceable under contract law.

- It clarifies the obligations and rights of both borrower and lenders to prevent misunderstandings.

- This modification enables the inclusion of new parties and changes to the financial terms.

Quick recap

- The Term Loan Agreement is crucial for documenting any modifications to loan terms.

- Proper completion and execution ensure clarity among involved parties.

- Utilizing online resources for form completion enhances accessibility and accuracy.

Looking for another form?

Form popularity

FAQ

For a personal loan agreement to be enforceable, it must be documented in writing and signed by both parties. You may choose to keep a copy in your county recorder's office if you wish, though it's not legally necessary. It's sufficient for both parties to keep their own copy, ideally in a safe place.

D) Example of Term Loan A term loan is a type of advance that comes with a fixed duration for repayment, a fixed amount as loan, a repayment schedule as well as a pre-determined interest rate. A borrower can opt for a fixed or floating rate of interest for repayment of the advance.

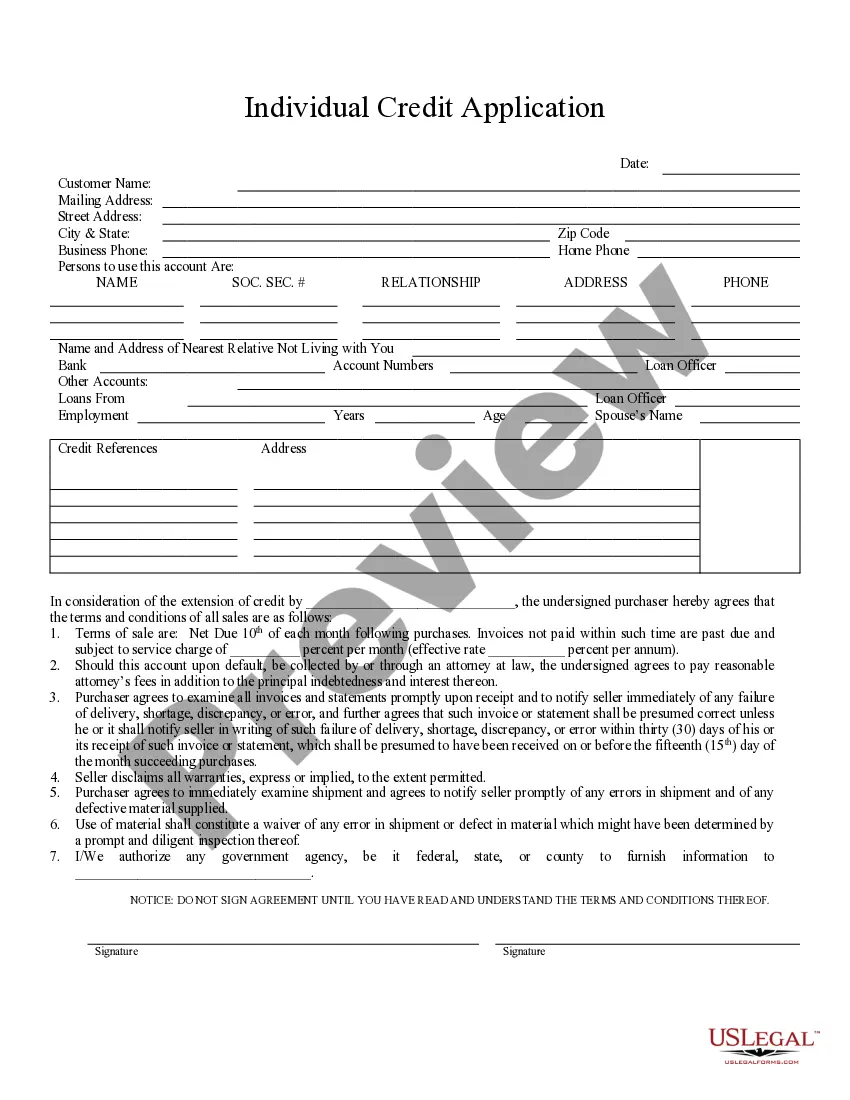

Loan agreements are binding contracts between two or more parties to formalize a loan process.Loan agreements typically include covenants, value of collateral involved, guarantees, interest rate terms and the duration over which it must be repaid.

Come up with a schedule for repayment. Use a family contract template that includes a repayment schedule. Set and interest rate. Put your agreement in writing. Keep payment records.

Identity of the Parties. The names of the lender and borrower need to be stated. Date of the Agreement. Interest Rate. Repayment Terms. Default provisions. Signatures. Choice of Law. Severability.

Starting the Document. Write the date at the top of the page. Write the Terms of the Loan. State the purpose of the personal payment agreement and the terms for returning the money. Date the Document. Statement of Agreement. Sign the Document. Record the Document.

Look for a sample template online which you can use as a guide for when you are drafting your document. Open a word processing software and start formatting your document. Identify the parties who are involved in the loan. Write your consideration to make your loan valid.

The most basic loan agreement is commonly called an "IOU." These are typically used between friends or relatives for small amounts of money, and simply state the dollar amount that is owed. They do not usually say when payment is due, nor include any interest provisions.

State the purpose for the loan. #Set forth the amount and terms of the loan. Your agreement should clearly state the amount of money you're lending your friend, the interest rate, and the total amount your friend will pay you back.