Articles Supplementary - classifying Preferred Stock as Cumulative Convertible Preferred Stock

Understanding this form

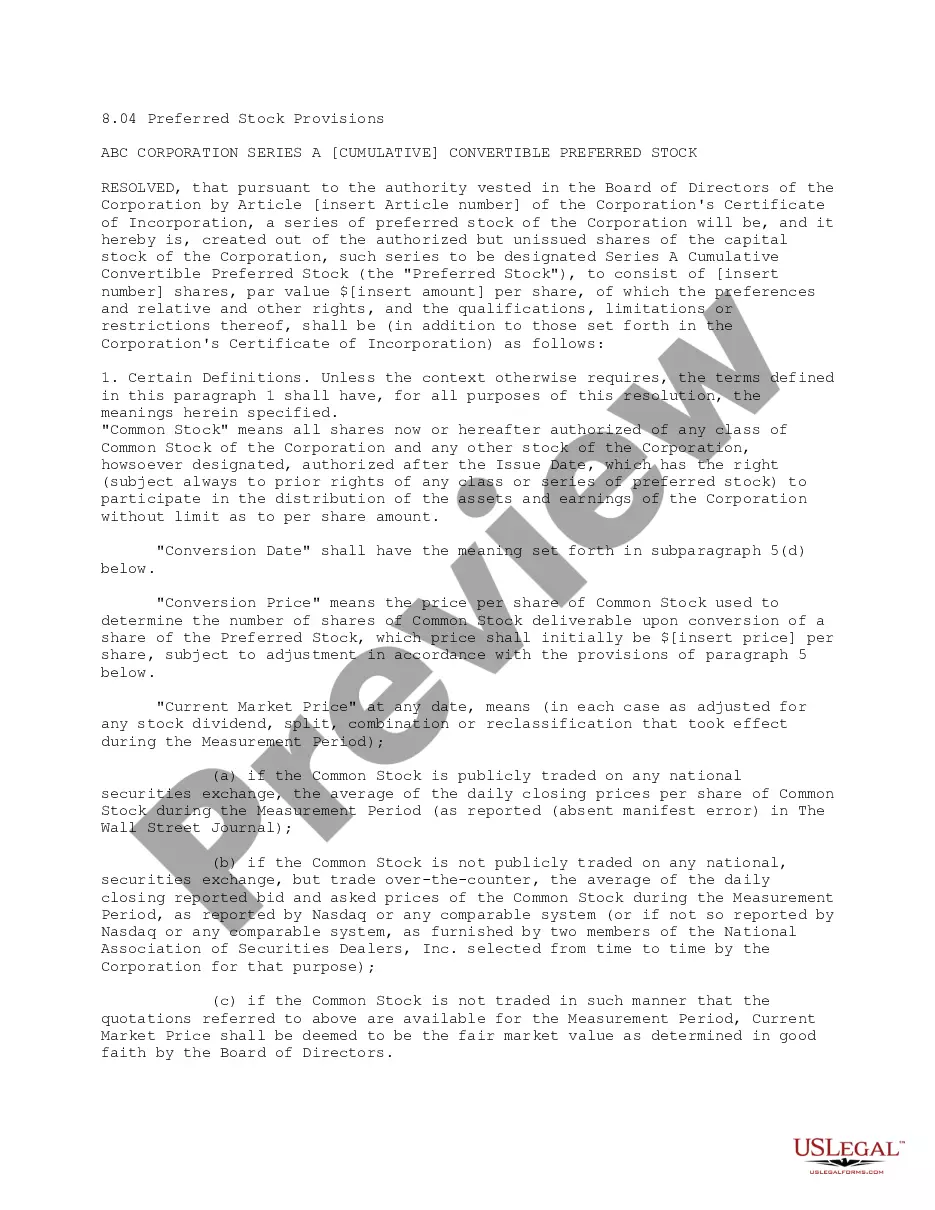

The Articles Supplementary for classifying Preferred Stock as Cumulative Convertible Preferred Stock is a legal document used by corporations to specify the rights, preferences, and limitations of a new series of preferred stock. This form, unlike standard stock issuance documents, details how the preferred shares function, including their cumulative dividends and conversion rights, distinguishing them from other types of stock. This is essential for corporate governance and to inform shareholders of their rights.

Form components explained

- Designation and amount of shares: Specifies the number of shares and their designation as Series B Cumulative Convertible Preferred Stock.

- Dividends: Outlines how and when dividends are accrued and paid to shareholders.

- Liquidation preference: Details the order of payment in the event of a company liquidation.

- Redemption rights: Lists conditions under which the corporation can redeem these preferred shares.

- Voting rights: Explains the circumstances under which preferred stockholders have voting rights.

When to use this document

This form is required when a corporation elects to create a new series of preferred stock with unique attributes, such as cumulative dividends and convertibility into common stock. It is commonly used during corporate restructuring, issuance of new shares to raise capital, or integration into financing agreements where specific shareholder rights need formal acknowledgment.

Intended users of this form

- Corporate officers and directors looking to issue new shares of preferred stock.

- Legal representatives involved in corporate governance matters.

- Corporations organized in Maryland or those whose governing documents reflect Maryland law.

Completing this form step by step

- Identify the corporation and state of incorporation at the beginning of the form.

- Specify the total number of shares being classified and their designation.

- Detail the terms for dividends, including rates, payment dates, and conditions.

- Outline the liquidation preferences and any specific rights associated with the shares.

- Ensure that the document is signed by the corporate officers as required for formal approval.

Notarization guidance

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to provide all necessary information about dividend rights and preferences.

- Not including the governing law provisions specific to Maryland corporate laws.

- Omitting signatures or dates from the corporate officers, making the document invalid.

Why complete this form online

- Immediate access to a professionally drafted document tailored to meet legal standards.

- Editable template allows customization to fit the specific needs of the corporation.

- Availability of legal support and resources during the completion process.

Legal use & context

- The Articles Supplementary legally establishes the rights of shareholders and is essential for maintaining corporate governance.

- Failure to complete this form correctly may hinder the ability to issue preferred stock or affect shareholder rights.

- This document assists in avoiding disputes regarding preferring stock characteristics in the future.

What to keep in mind

- The Articles Supplementary is crucial for defining the terms related to a new series of preferred stock.

- Understanding the rights and privileges associated with preferred stock is vital for compliance and good corporate governance.

- Using this form correctly can prevent future disputes with investors and clarify stockholder rights.

Looking for another form?

Form popularity

FAQ

Find the dividend rate for the cumulative preferred stock. Multiply the dividend percentage rate by the par value to find the dollar amount of the dividend per share. Check the company's annual and quarterly reports to see if any cumulative preferred stock dividends have not been paid.

Find the dividend rate for the cumulative preferred stock. Multiply the dividend percentage rate by the par value to find the dollar amount of the dividend per share. Check the company's annual and quarterly reports to see if any cumulative preferred stock dividends have not been paid.

Preferred shares usually pay cumulative dividends, but not always.

Accounting for Cash Dividends When Only Common Stock Is Issued. The journal entry to record the declaration of the cash dividends involves a decrease (debit) to Retained Earnings (a stockholders' equity account) and an increase (credit) to Cash Dividends Payable (a liability account).

Cumulative preferred dividends go from being a balance sheet footnote to a recognized liability when your board of directors declares a dividend. The dividends are accounted for in the Dividends Payable account in the current liabilities section on the balance sheet.

Multiply the number of missed quarterly preferred dividend payments by the company's quarterly dividend payment. Continuing the same example, $1.50 x 5 = $7.50. This figure represents the cumulative dividend per share of preferred stock owed by the company.

Due to this lower cost of capital, most companies' preferred stock offerings are issued with the cumulative feature. Generally, only blue-chip companies with strong dividend histories can issue non-cumulative preferred stock without increasing the cost of capital.

It sports the name preferred because its owners receive dividends before the owners of common stock. On a classified balance sheet, a company separates accounts into classifications, or subsections, within the main sections. Preferred stock is classified as part of capital stock in the stockholders' equity section.