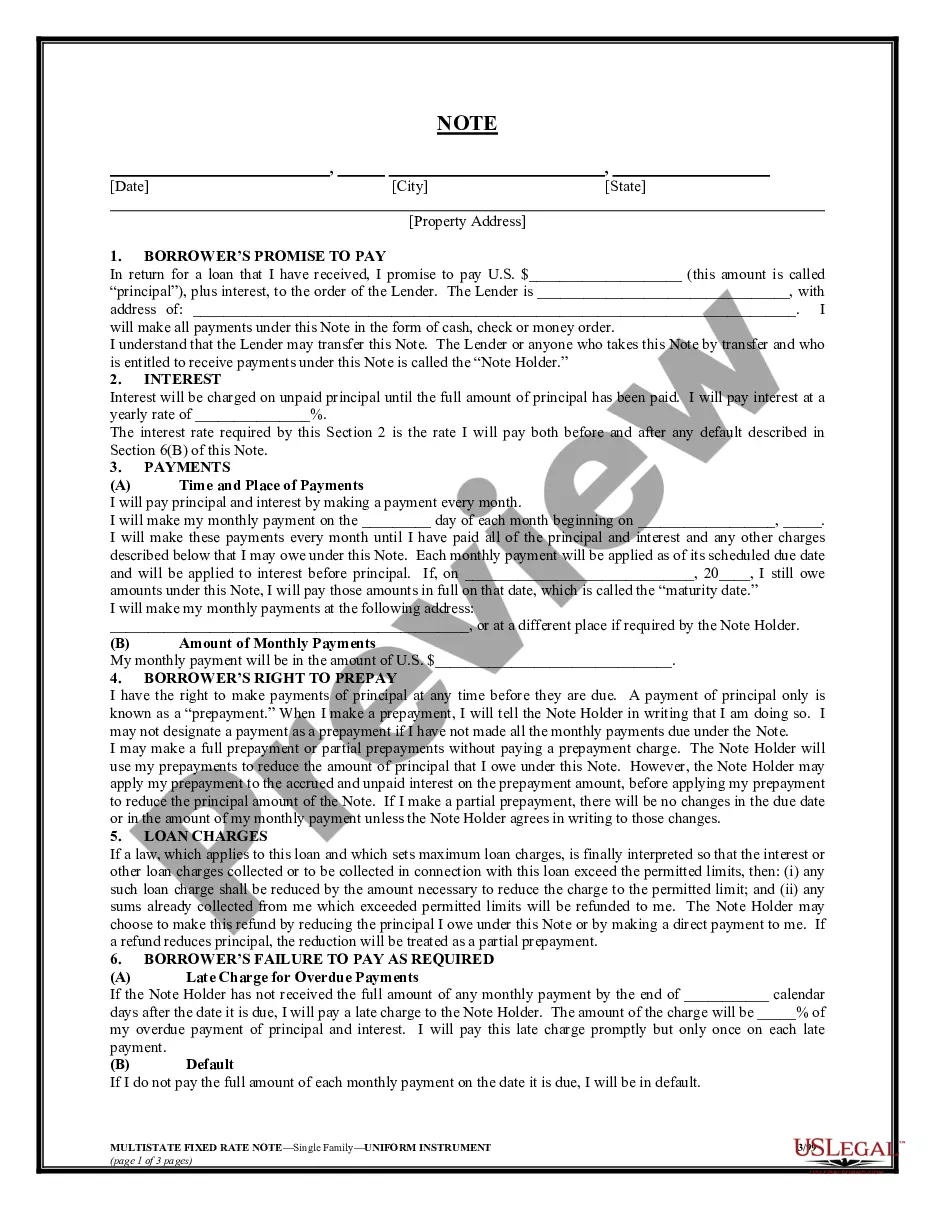

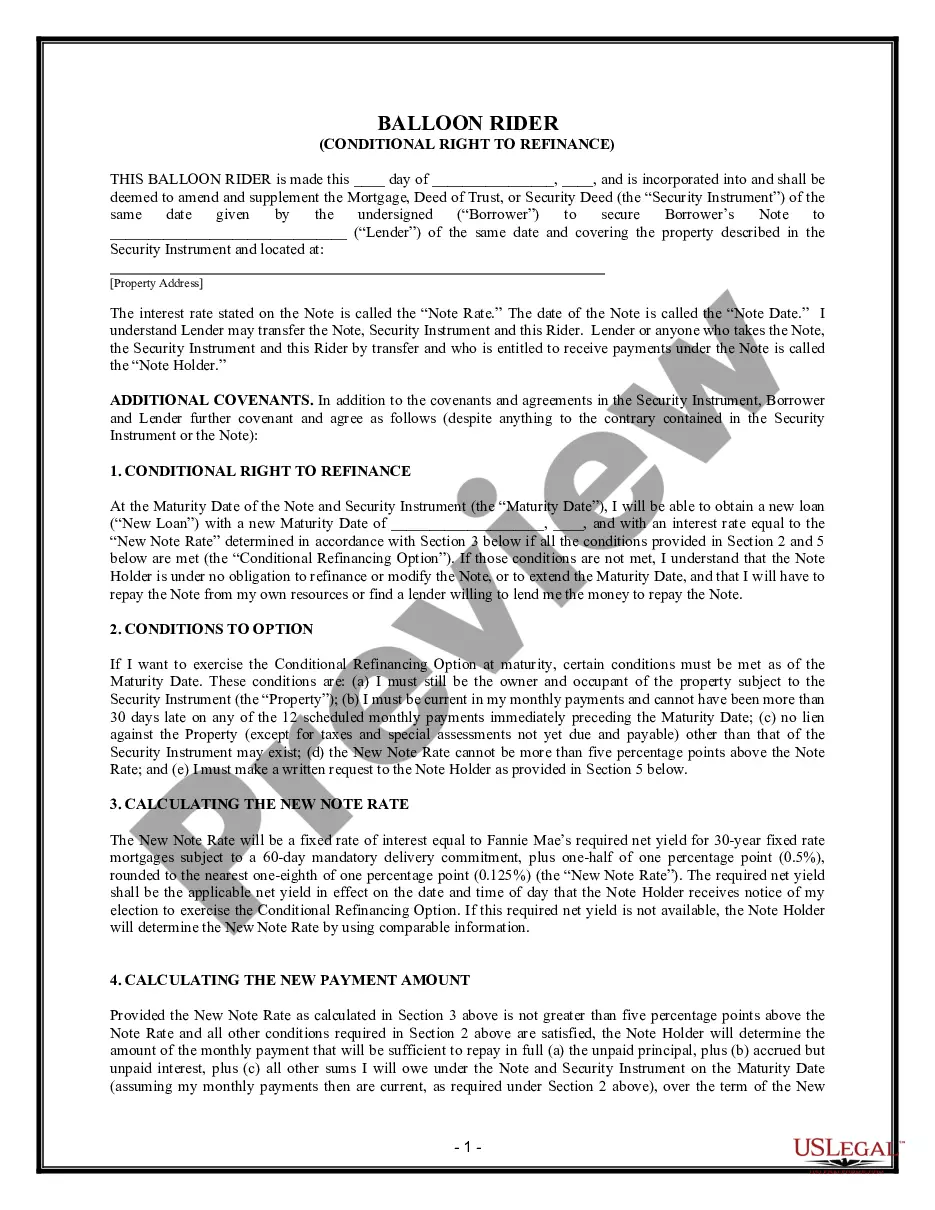

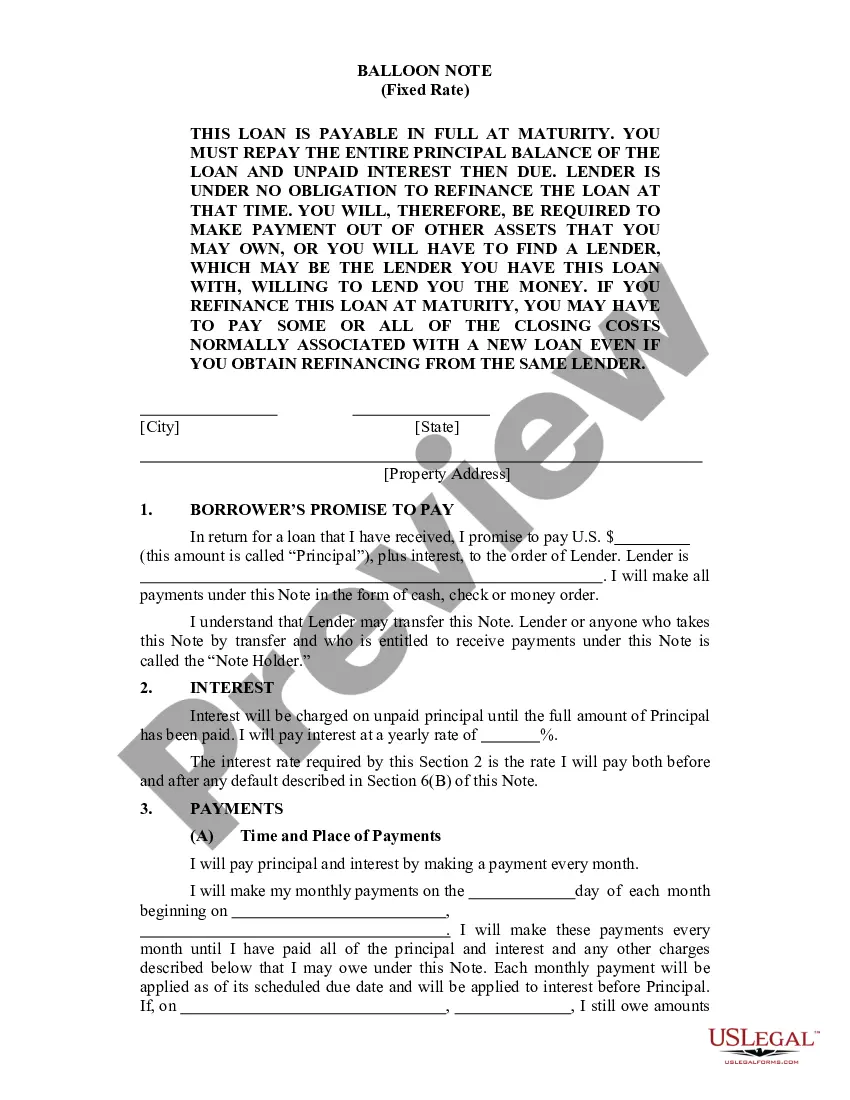

Multistate Balloon Note Addendum - Single Family

Understanding this form

The Multistate Balloon Note Addendum - Single Family is a legal document that serves as an addendum to a balloon note, specifically for single-family properties. This form allows borrowers to have a conditional right to refinance their loan at maturity under certain conditions. Unlike standard loan agreements, this addendum provides options for borrowers to modify their payment terms when their loan reaches its maturity date, thus offering flexibility that can assist in financial planning.

Form components explained

- Conditional refinancing option at the maturity date of the balloon note.

- Requirements that must be met to exercise the refinancing option, such as ownership and payment history.

- Calculation of the new interest rate based on market conditions and Fannie Mae's required yields.

- Specification of the new payment amount based on the adjusted interest rate and outstanding principal.

- Notification process and deadlines for exercising the refinancing option.

When this form is needed

This form is ideal for individuals who have taken out a balloon note for a single-family home and are approaching the maturity date of their loan. It is particularly useful for those who anticipate needing to refinance their loan to manage payments or avoid a lump-sum payment at maturity. Use this addendum if you seek to ensure a smoother transition to a new loan with potentially favorable terms, assuming you meet the required conditions.

Who needs this form

- Homeowners with a balloon note on their single-family property.

- Borrowers seeking to refinance their existing balloon note at maturity.

- Individuals aiming to clarify terms with their lender regarding refinancing options.

Steps to complete this form

- Identify the date of the addendum and fill out the required details.

- Enter the names of the borrower and lender as specified.

- Detail the conditions required to exercise the refinancing option, including ownership and payment status.

- Calculate the new note rate based on the conditions outlined.

- Sign and date the addendum to acknowledge acceptance of its terms.

Notarization requirements for this form

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to meet the specified conditions prior to the maturity date.

- Not communicating with the lender in the required time frame.

- Incorrectly calculating the new note rate or monthly payments.

- Omitting essential details when providing property or financial information.

Why complete this form online

- Convenient access to necessary legal documents without the need for in-person appointments.

- Editable templates that allow customization to fit specific situations.

- Reliable legal language drafted by licensed attorneys to ensure compliance.

Looking for another form?

Form popularity

FAQ

Since you'll be required to make a large payment at the end of the loan, balloon mortgages generally aren't a good idea for the average homebuyer. Your finances or life plans may not turn out how you predict. Balloon loans are also not widely available.

Generally, a balloon payment is more than two times the loan's average monthly payment, and often it can be tens of thousands of dollars. Most balloon loans require one large payment that pays off your remaining balance at the end of the loan term.

Balloon mortgages should come with a lower interest rate than either fixed-rate or adjustable-rate mortgages, making them a cheaper loan for the right consumers. Those consumers who plan to live in a home for only a short period of time, might do well to take out a balloon mortgage.

You also may qualify for a larger loan amount with a balloon mortgage than you would if you got an adjustable-rate or fixed-rate mortgage. Additionally, this type of mortgage may be beneficial if you plan on selling your home before the balloon payment is due; and you think you'll make a profit on the home.

Balloon mortgage cons Pay a large amount at once. The downside of low monthly payments is that you have to pay a huge sum at the end of your balloon mortgage term.High risk. There are several risks associated with a balloon mortgage.Difficult to refinance.Hard to find.

A balloon payment is a type of loan with lower monthly payments during the initial period and one larger-than-usual payment at the end of the term. They can be attractive, but risky, options for borrowers.

People who expect to stay in their home for only a short period of time may opt for a balloon mortgage. It comes with low monthly payments and a much lower overall cost, since it is paid off in a few years rather than in 20 or 30 years like a conventional mortgage.

If you can't make the balloon payment, the lender can foreclose on your home. This could seriously impact your credit, making it more difficult to get a mortgage or even rent a home in the future. Avoiding foreclosure might require selling the home to cover the balloon payment.