Indemnification of Surety

About this form

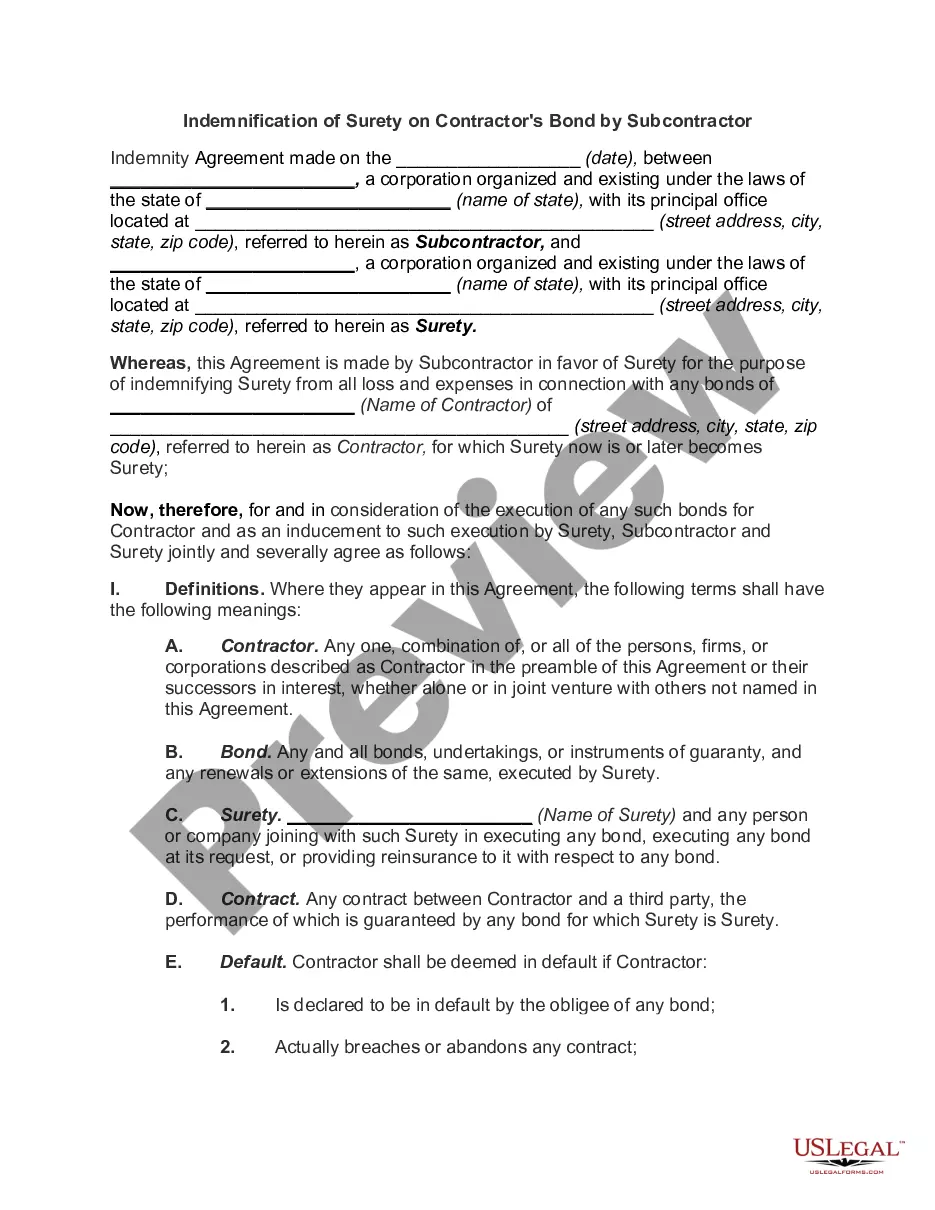

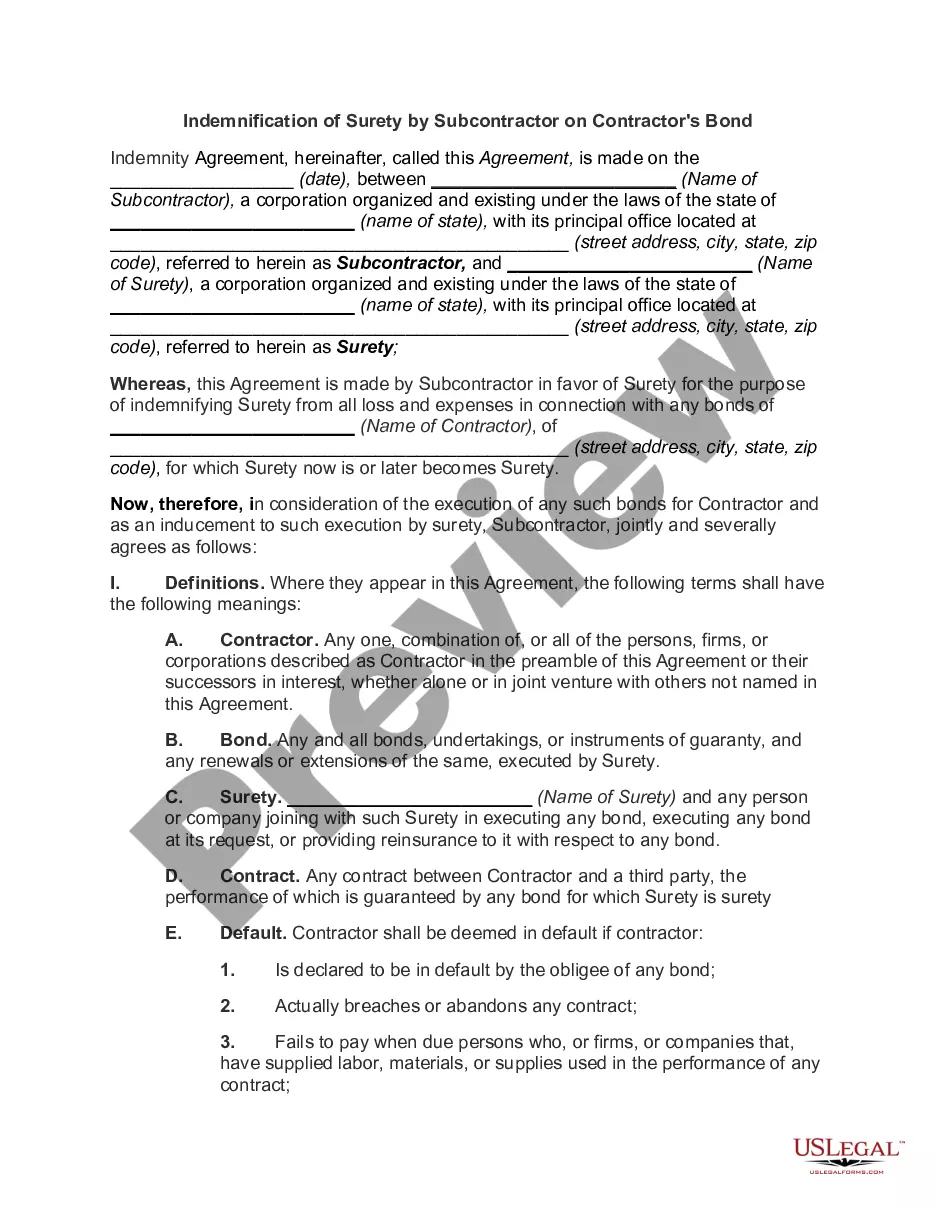

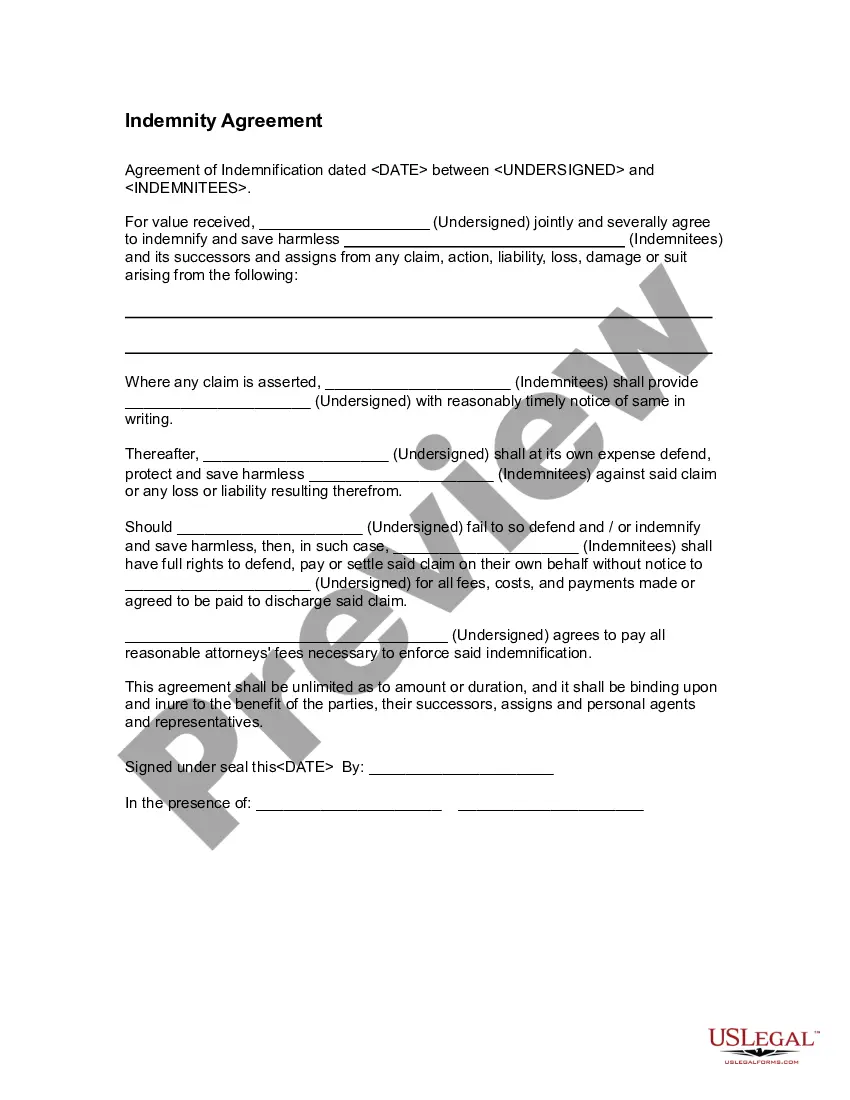

The Indemnification of Surety form is a legal agreement that establishes the responsibilities of an indemnitor to indemnify a surety and an indemnitee for any losses or liabilities incurred from suretyship duties. This form is crucial in situations where one party acts as a guarantor for the debts of another, ensuring that the indemnitee is protected in the event that the principal debtor defaults on their obligations. By outlining the terms of indemnity, this form helps clarify the roles and liabilities involved, differing from simple guarantees or surety agreements in its structured commitment to compensation for possible damages or losses.

Key components of this form

- Date and names of the indemnitor, indemnitee, and surety.

- Indemnity clauses stating obligations of the indemnitor to cover losses.

- Waiver of rights to claim any property as exempt from liabilities.

- Indemnitor's obligations regarding payment for incurred costs.

- Notice requirements and procedures for any cancellation of the agreement.

- Governing law and arbitration terms in case of disputes.

When to use this form

This form should be used when a principal debtor requires a surety to guarantee their obligations, and there is a need for a clear indemnity agreement to protect the surety from potential losses. It's often employed in construction contracts, financial transactions, or any situation involving a surety bond where the indemnitee may face claims or liabilities due to the actions of the indemnitor.

Who needs this form

- Corporations acting as indemnitors seeking to protect sureties and indemnitees.

- Individuals or organizations acting as sureties for another party's obligations.

- Legal professionals assisting clients in drafting indemnity agreements.

- Businesses involved in contractual obligations where suretyship is required.

How to prepare this document

- Identify the date and full names of the indemnitor, indemnitee, and surety.

- Provide detailed addresses for each party involved in the agreement.

- Fill in the indemnity amounts and specify liabilities that are to be covered.

- Ensure all parties sign and date the document, acknowledging their consent to the terms.

- Keep a copy of the signed form for your records and future reference.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, obtaining notarization can enhance the document's credibility and may be necessary for certain transactions or in particular jurisdictions.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include the correct legal names and addresses of all parties.

- Not specifying the indemnity amount, leading to ambiguity in liability coverage.

- Omitting signatures or dates, which can invalidate the agreement.

- Ignoring state-specific laws that may impact the enforceability of the agreement.

Benefits of using this form online

- Instant access to a customizable, professionally drafted indemnity agreement.

- Convenient downloading and printing options for immediate use.

- Editable fields allow for personalization to meet specific needs.

- Guidance throughout the completion process ensures accuracy and completeness.

Looking for another form?

Form popularity

FAQ

In short, indemnity compels a party to compensate another party. Regarding a surety bond, this means that the obligee has the legal right to collect from the surety if the principal of the bond fails to uphold their end of the bond.

The surety, otherwise known as the insurance company providing the bond, guarantees to the obligee that the principal will fulfill an obligation or perform as required by the underlying contract.

While the bond itself is created by the obligee, an indemnity is a separate agreement that the surety requires the principal to sign prior to issuing the bond that guarantees the principal is responsible for repaying any money paid by the surety in the process of settling a claim.

Surety bonds are a useful service, but not the same thing as professional liability insurance, also known as errors and omissions (E&O) insurance. You may need both surety bonds and professional liability insurance to safeguard your business.

Insurance pays on behalf of you; surety bonds are just a guarantee of payment to another party. The primary difference between a surety bond and insurance is that insurance will pay for losses in a claim, whereas a bonding company will guarantee your obligations are fulfilled.