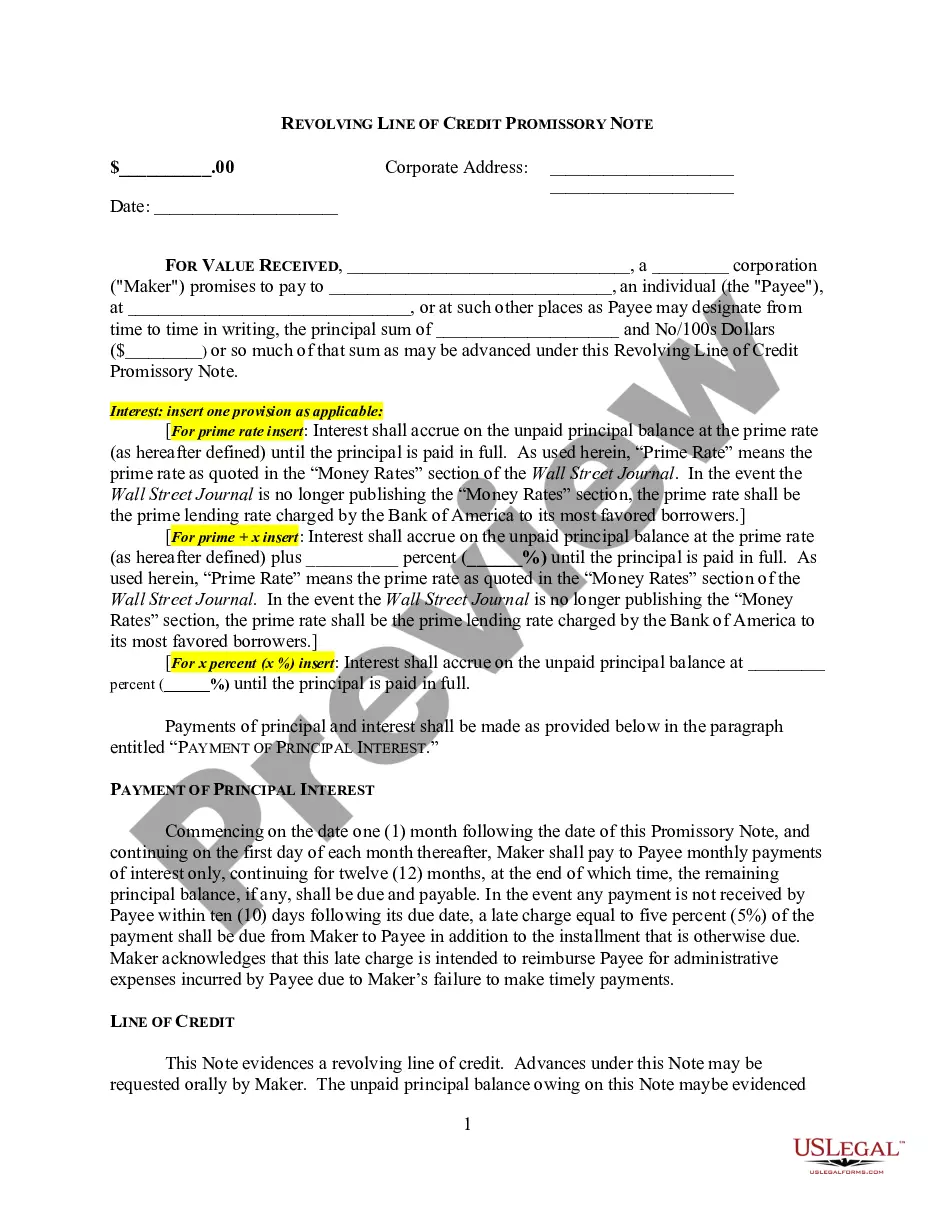

Revolving Credit Agreement

What is this form?

A revolving credit agreement is a legal document that establishes a line of credit between a buyer and a seller, enabling purchases and cash advances within a specified limit. Unlike traditional loans, this open-ended credit agreement allows buyers to borrow money repeatedly as long as they do not exceed their credit limit. It also outlines payment terms, finance charges, and account management, making it distinct from other loan agreements.

Form components explained

- Parties involved: Identification of the buyer and seller with their respective addresses.

- Establishment of account: Terms under which the buyer may use the credit line.

- Maximum amount of credit: The limit that cannot be exceeded during the agreement.

- Periodic statements: Requirements for monthly statements detailing balances and transactions.

- Finance charge calculation: The method and rate for accruing finance charges on outstanding balances.

- Cancellation and payment terms: Conditions under which the agreement can be canceled and payment obligations.

When this form is needed

This form is essential when businesses or individuals require flexible financing options for purchasing goods or managing cash flow. It's particularly useful for retailers who wish to offer customers a credit line for purchases or for buyers seeking ongoing access to funds for operational expenses. If you expect to make repeated transactions, a revolving credit agreement provides the necessary framework for maintaining credit and managing payments effectively.

Intended users of this form

This form is suitable for:

- Businesses that want to provide credit to clients or customers.

- Buyers looking for flexible payment arrangements for purchases over time.

- Sellers who wish to facilitate ongoing transactions without requiring immediate full payment.

- Corporations needing structured financing options for operational cash flow.

How to complete this form

- Identify the parties: Enter the names and addresses of the buyer and seller at the start of the agreement.

- Set the credit limit: Specify the maximum amount of credit that the buyer may utilize.

- Detail payment terms: Outline the required minimum payment and terms for late payments.

- Define finance charges: State the interest rate to be applied on the outstanding balance monthly.

- Establish cancellation terms: Include conditions under which either party may cancel the agreement.

Notarization guidance

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to specify the maximum credit limit clearly.

- Not detailing the calculation for finance charges, leading to confusion.

- Neglecting to include payment due dates and conditions for late fees.

- Forgetting to obtain signatures from both parties to validate the agreement.

Benefits of using this form online

- Easy access: Downloadable format allows quick acquisition and editing.

- Legal assurance: Templates are drafted by licensed attorneys, ensuring legal compliance.

- Time-saving: Reduces the need for consultations or lengthy drafting processes.

- Cost-effective: Affordable alternatives to hiring legal professionals for standard agreements.

Looking for another form?

Form popularity

FAQ

Primary tabs. Revolving credit facilities are a type of committed credit facility which allow the borrower to borrow on an ongoing basis while repaying the balance in regular payments. Each repayment of the loan, minus interest and fees, replenishes the amount available to the borrower.

Two of the most common types of revolving credit come in the form of credit cards and personal lines of credit.

Three examples of revolving credit are a credit card, a home equity line of credit (HELOC) and a personal line of credit. Revolving credit is credit you can use repeatedly up to a certain limit as you pay it down.

The most common types of revolving credit are credit cards, personal lines of credit and home equity lines of credit.

Common Examples Of Revolving Debt Credit cards, lines of credit and home equity lines of credit (HELOCs) are the most common examples of revolving credit, which turns into revolving debt if you carry a balance month-to-month.

Revolving credit is a type of loan that gives you access to a set amount of money. You can access money until you've borrowed up to the maximum amount, also known as your credit limit. As you repay the outstanding balance, plus any interest, you unlock the ability to borrow against the account again.

Revolving credit facility vs term loan In other words, a term loan is a type of loan that is lent for a specific amount of time (the term). With a revolving facility, the lender stipulates the maximum amount you can spend, however within that you have the freedom to decide how much you borrow and pay back every month.

A revolving loan is considered a flexible financing tool due to its repayment and re-borrowing accommodations. It is not considered a term loan because, during an allotted period of time, the facility allows the borrower to repay the loan or take it out again.

Unlike a term loan, a revolving credit facility does not have a fixed repayment schedule. The borrower only pays interest on the funds that are actually used, and the credit limit can be renewed once the outstanding balance is paid down.