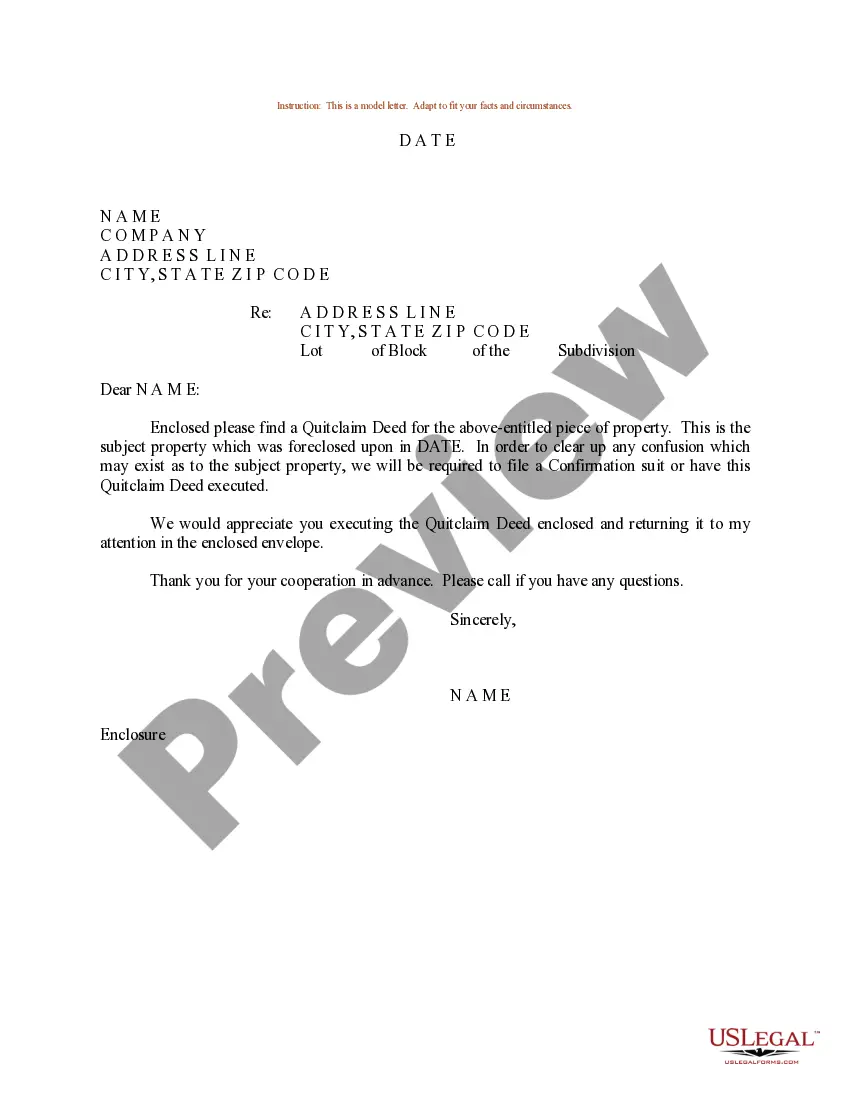

Sample Letter for Judicial Foreclosure

About this form

The Sample Letter for Judicial Foreclosure is a template designed to assist property owners in communicating with creditors regarding the foreclosure process. This form serves as a formal notice that outlines specific issues related to the foreclosed property, including any complications identified during a title search. Unlike other foreclosure forms, this letter focuses on providing a preliminary notification to the relevant parties about potential legal actions concerning the property in question.

Key components of this form

- Date: The date when the letter is drafted.

- Private name and company: The recipient's name and company information.

- Address: The complete address of the recipient.

- Description of the issue: Details regarding the title search findings and their implications.

- Contact request: An invitation for the recipient to discuss the next steps.

- Sender's name: The name of the person sending the letter.

- Enclosures: Any additional documents referred to in the letter.

When this form is needed

This sample letter should be used in situations where a property owner has identified issues with a property's title during a foreclosure process. It is particularly relevant when there are discrepancies in property ownership or when additional parcels are involved in the legal proceedings. This form is also applicable when notifying creditors or involved parties about these findings and seeking further communication regarding how to address the situation.

Who should use this form

- Property owners facing foreclosure proceedings.

- Attorneys representing clients in foreclosure cases.

- Individuals seeking to communicate title issues to creditors.

- Anyone needing a structured approach to notifying interested parties about foreclosure-related matters.

How to complete this form

- Enter the date at the top of the letter.

- Fill in the recipient's name and company information.

- Provide the complete address of the recipient.

- Clearly describe the findings from the title search, including any specific issues.

- Request contact for further discussion about the situation.

- Sign the letter with your name and include any necessary enclosures.

Does this form need to be notarized?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include all relevant details about the title issues.

- Not providing a clear request for follow-up communication.

- Using an improper format or tone for a legal letter.

- Omitting necessary enclosures or supporting documents.

Benefits of completing this form online

- Convenience of downloading and editing the form to meet specific needs.

- Access to templates drafted by licensed attorneys, ensuring legal clarity.

- Ability to quickly create a professional document without needing legal expertise.

Looking for another form?

Form popularity

FAQ

In a non-judicial foreclosure, the lender is proceeding on the basis that the mortgage or deed of trust provides for its right of foreclosure. This means that your lawsuit will ask the judge to stop the foreclosure proceeding until they can review your argument against the foreclosure.

Gather your loan documents and set up a case file. Learn about your legal rights. Organize your financial information. Review your budget. Know your options. Call your servicer. Contact a HUD-approved housing counselor.

A hardship letter should Start by stating the purpose of the letter whether it is a loan modification or a short sale so the lender knows what homeowners want. It should say something like I need to restructure my mortgage and obtain a lower, fixed interest rate2026, in a way that force them to find out why.

To contest a judicial foreclosure, you have to file a written answer to the complaint (the lawsuit). You'll need to present your defenses and explain the reasons why the lender shouldn't be able to foreclose. You might need to defend yourself against a motion for summary judgment and at trial.

As part of the lawsuit, the foreclosing party includes a petition for foreclosure that explains why a judge should issue a foreclosure judgment. In most cases, the court will do so, unless the borrower has a defense that justifies the delinquent payments.

Your name, address, phone number and account number. The type of debt resolution you're seeking. Your financial situation that has caused you to fall behind in your payments. A detailed budget and your plan for making payments (if you want to keep your home)

You can bring your loan current and stave off the foreclosure sale filing by paying the past due amount, plus penalties.You typically have to reinstate at least five days before the lender's deadline or risk the lender rejecting your payment and proceeding with a sale.

A lender can rescind a foreclosure sale if a borrower requests to reinstate the loan agreements and then makes payment to bring the loan balance current, provided this is done more than five days before the scheduled sale date.

It takes several months for a lender to foreclose on a California property. If everything goes according to schedule, the process typically takes approximately 120 days about four months but the process can take as long as 200 or more days to conclude.