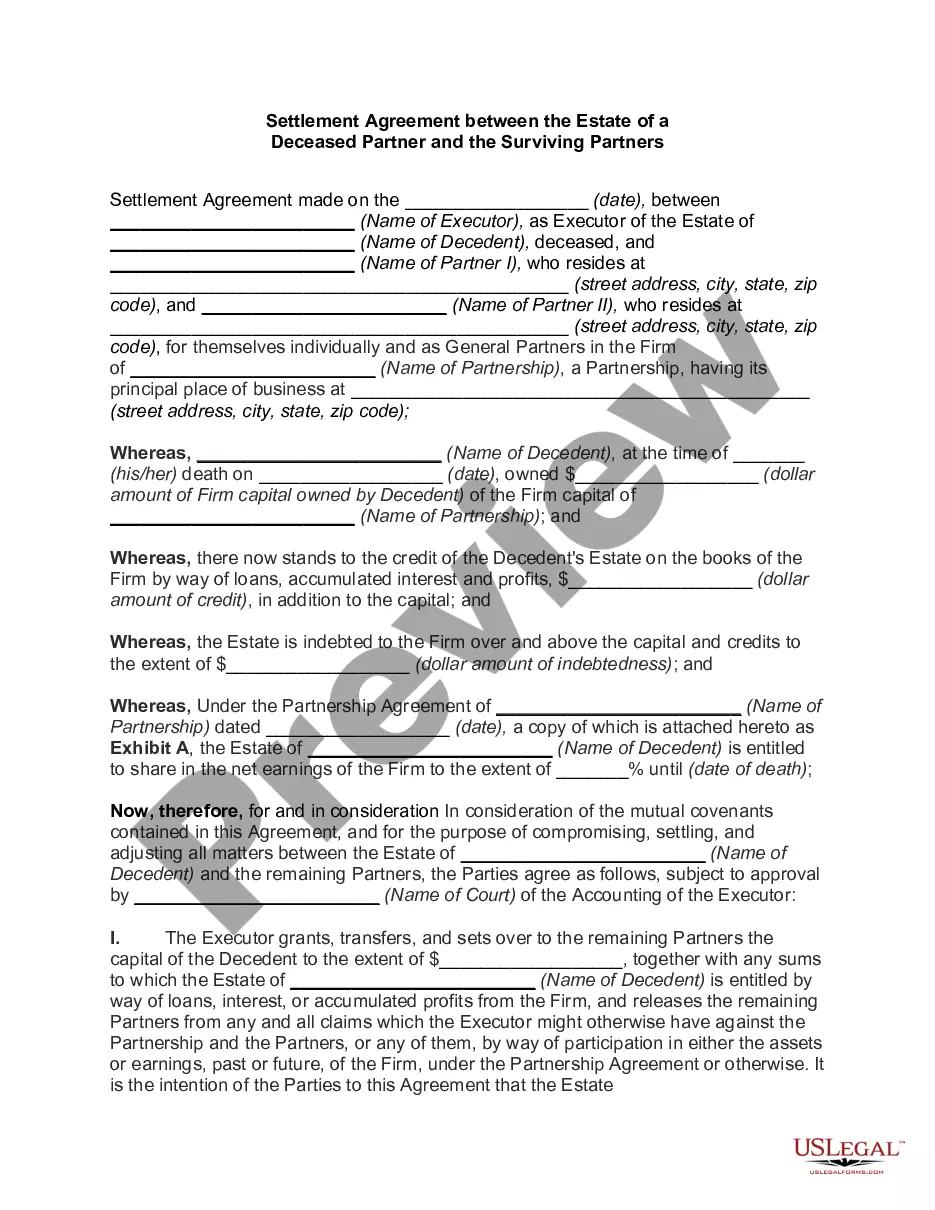

Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner

What this document covers

The Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner is a critical document that formalizes the continuation of a partnership after one partner has passed away. This agreement is specifically designed for surviving partners and the legal representative of the deceased, such as an executor of the estate, to ensure seamless operations of the business. Unlike similar agreements, this form addresses the unique challenges and legal considerations arising from the death of a partner, ensuring that all parties are aligned on the future direction of the business.

What’s included in this form

- Identification of the surviving partners and the deceased partner's representative.

- Overview of the partnership's business operations.

- Details regarding the financial interests of the deceased partner.

- Provisions for management and decision-making moving forward.

- Signatures of all parties involved to validate the agreement.

Common use cases

This form should be used when a partner in a business partnership passes away, and the surviving partners wish to continue the business operations. It is especially important in scenarios where there is a need to clarify ownership, management roles, and financial responsibilities pertaining to the deceased partner's share of the business.

Intended users of this form

This form is intended for:

- Surviving partners in a business partnership.

- Executors or legal representatives of the deceased partner's estate.

- Partners who wish to formalize agreements regarding the operation of the business after a partner's death.

How to complete this form

- Identify all parties involved, including the surviving partners and the legal representative of the deceased partner.

- Provide a brief overview of the business and outline its operational details.

- Specify the financial interests of the deceased partner that need to be addressed.

- Agree on management responsibilities and decision-making processes moving forward.

- Ensure all parties sign and date the form to make it legally binding.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, having the agreement notarized can provide an added layer of authenticity and prevent disputes in the future.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include all relevant parties in the agreement.

- Not clearly outlining the financial responsibilities of each surviving partner.

- Omitting necessary signatures, which can void the agreement.

- Using outdated or incorrect legal language, which may confuse the purpose of the document.

Advantages of online completion

- Immediate access to expertly drafted legal templates.

- Convenient download options that allow for easy completion.

- Reliable formats that ensure compliance with legal standards.

- Editability that allows customization based on specific partnership needs.

Summary of main points

- The agreement helps ensure business continuity after a partner's death.

- Essential for managing the interests of the deceased partner's estate.

- Should be completed with attention to detail to avoid disputes.

Looking for another form?

Form popularity

FAQ

The Supreme Court held as under: Section 42(c) of the Partnership Act can appropriately be applied to a' partnership where there are more than two partners. If one of them dies, the firm is dissolved; but if there is a contract to the contrary, the surviving partners will continue the firm.

Name of your partnership. Contributions to the partnership and percentage of ownership. Division of profits, losses and draws. Partners' authority. Withdrawal or death of a partner.

Partnership agreement. A partnership agreement spells out the relationship between partners, as well as their individual obligations and contributions to a business. Indemnity agreement. Nondisclosure agreement. Property and equipment lease.

Continuation of the Partnership Your agreement or your applicable state law may require the continuation of the business upon a partner's death. However, your deceased partner's estate becomes a transferee of the business.

A dissolution of a partnership generally occurs when one of the partners ceases to be a partner in the firm. Other causes of dissolution are the BANKRUPTCY or death of a partner, an agreement of all partners to dissolve, or an event that makes the partnership business illegal.

If a Limited Partner dies, the personal representative or other successor in interest of the deceased Limited Partner shall have all the rights and privileges of a Limited Partner. Death of a Limited Partner. The death of a Limited Partner shall not dissolve or terminate the Partnership.

The death of a partner in a two-person partnership will terminate the partnership for federal tax purposes if it results in the partnership's immediately winding up its business (Sec.If this occurs, the partnership's tax year closes on the partner's date of death.

When a partner in a partnership dies, the basic position under the Partnership Act 1890 is that the partnership is dissolved: 'Subject to any agreement between the partners, every partnership is dissolved as regards all the partners by the death2026 of any partner.