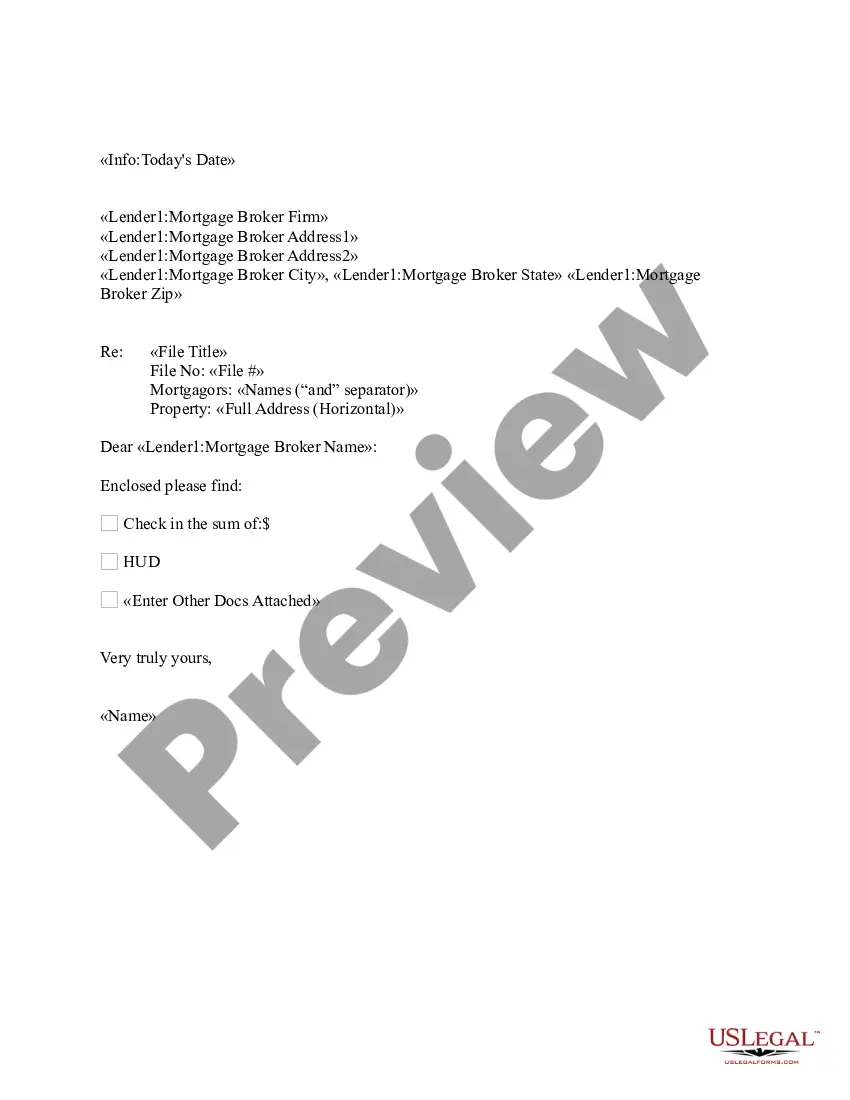

Sample Letter for Response to Inquiry - Mortgage Company

Understanding this form

This form is a sample letter for responding to an inquiry from a mortgage company. It outlines the necessary details to formally address and resolve queries regarding mortgage matters. This response letter is distinct from other forms in that it focuses specifically on inquiries related to mortgages, ensuring clarity in communication and compliance with industry practices.

Key components of this form

- Return address: Your information including name and address.

- Date: The date when the letter is sent.

- Recipient information: The mortgage company's name and address.

- Reference line: Subject indicating the purpose of the letter.

- Closing signature: Your printed name and signature.

Common use cases

This form is useful when you need to formally respond to an inquiry from your mortgage company. Common scenarios include clarifications on loan terms, requests for documentation, or responses to policy changes that may affect your mortgage terms. Utilizing this form can help ensure that your response is professional and complete.

Intended users of this form

This form is intended for individuals who hold a mortgage and have received an inquiry or request for information from their mortgage company. It is suitable for homeowners, property buyers, and anyone currently involved in a mortgage agreement.

Completing this form step by step

- Gather your personal information, including your address.

- Fill in the date you are sending the letter.

- Enter the mortgage companyâs name and address accurately.

- Clearly state the subject of your response in the reference line.

- Sign the letter with your name to finalize it.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. It serves as a standard written response to inquiries and can be sent directly to the mortgage company without formal witnessing.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Not including the proper return address or date.

- Failing to clearly state the purpose of the inquiry response.

- Omitting the recipient's name or addressing the letter incorrectly.

- Using informal language not suitable for business correspondence.

Advantages of online completion

- Convenient access to the letter template that you can complete at your own pace.

- Editability allows you to customize the form to your specific situation.

- Reliable format ensures it meets typical requirements for professional correspondence with mortgage companies.

Quick recap

- This form is essential for formal responses to mortgage inquiries.

- Includes all necessary components for effective communication.

- Can be customized for clarity and compliance with local requirements.

Looking for another form?

Form popularity

FAQ

Give precise details of the situation or circumstances. Describe the facts that resulted in the current situation. Be truthful so that you may not find yourself in a difficult position. Provide supporting documents if they are available. Describe what you will do to make the correction.

The key to writing a great letter of explanation is to keep it short, simple and informative. Be clear and write with as much detail as you can since someone else will need to understand your situation. Avoid including irrelevant information or answers to questions the underwriter didn't ask.

Inquiries tell other creditors that you are thinking of taking on new debt. An inquiry typically has a small, but negative, impact on your credit score. Inquiries are a necessary part of applying for a mortgage, so you can't avoid them altogether.

The Inquiry letter is used to explain all credit inquiries in the last 120 days. When the lender pulls credit OR when credit is automatically pulled at borrower submission. Notes:If they do, then Blend will treat those 2 or 3 inquiries as the same and only request one single inquiry from the borrower.

Give precise details of the situation or circumstances. Describe the facts that resulted in the current situation. Be truthful so that you may not find yourself in a difficult position. Provide supporting documents if they are available. Describe what you will do to make the correction.

An underwriter may request a letter of explanation from you if they're unsure about something they see.They might simply need clarification or more information about your credit report or bank statement. Letters of explanation are requirements from secondary authorities that own or back the loan in many cases.

Typically, hard inquiries occur when lenders look at your credit report after you have applied for credit. A hard inquiry often has a negative effect on your credit score. Lenders may do a hard inquiry when you request a preapproval or submit a formal application as you are mortgage shopping.

To send a credit inquiry removal letter, you should contact any credit reporting agency that is reporting the inquiry. Credit inquiry removal letters can be sent to both the credit reporting agencies and the lender who issued the credit inquiry.

If the borrower had six or more months in job gaps, then they need to be with a full-time job for at least six months to qualify for a mortgage loan. If the borrower had gaps in employment for less than six months, then they can qualify for a mortgage with a new full-time job.