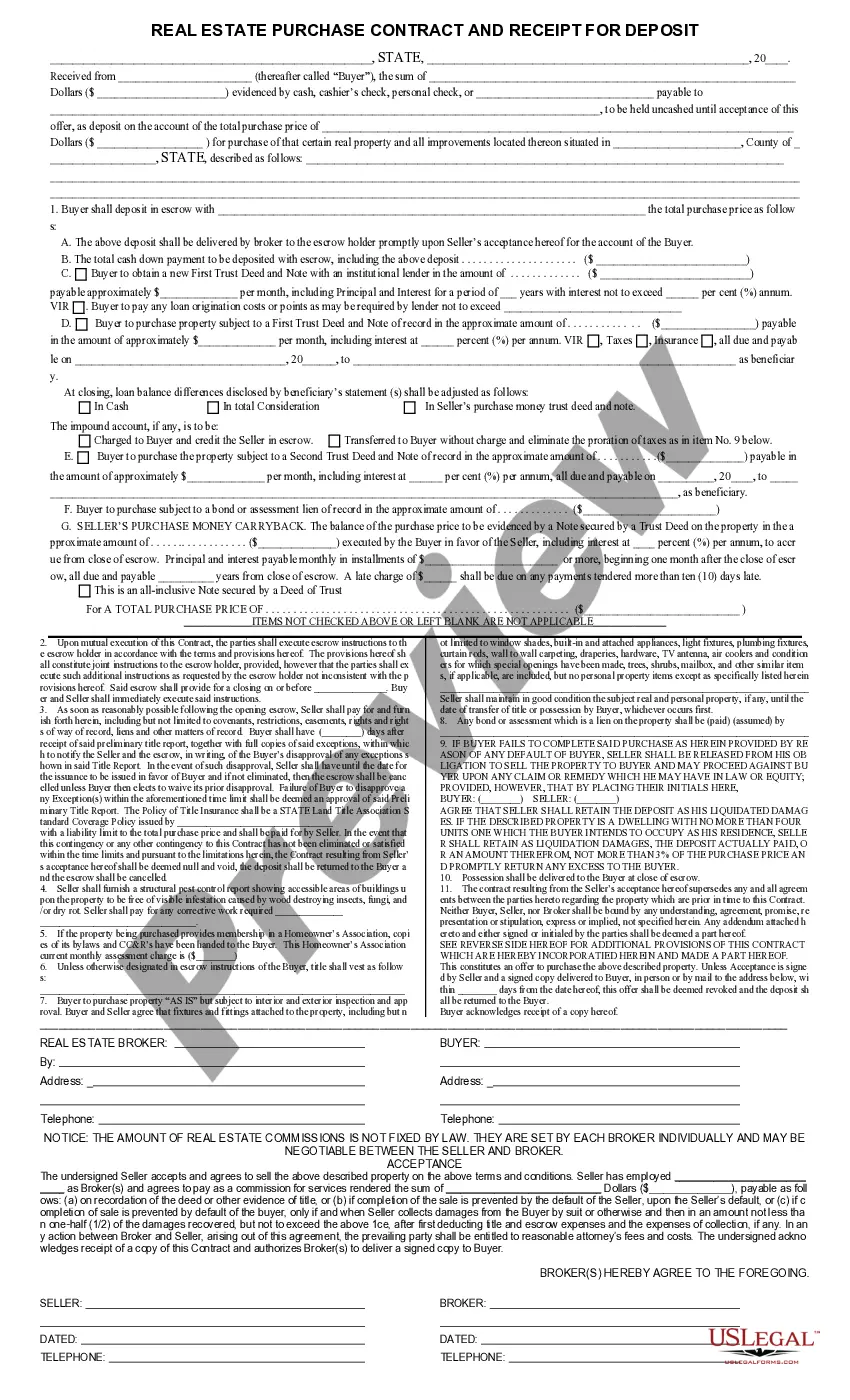

Purchase Contract and Receipt - Residential

Understanding this form

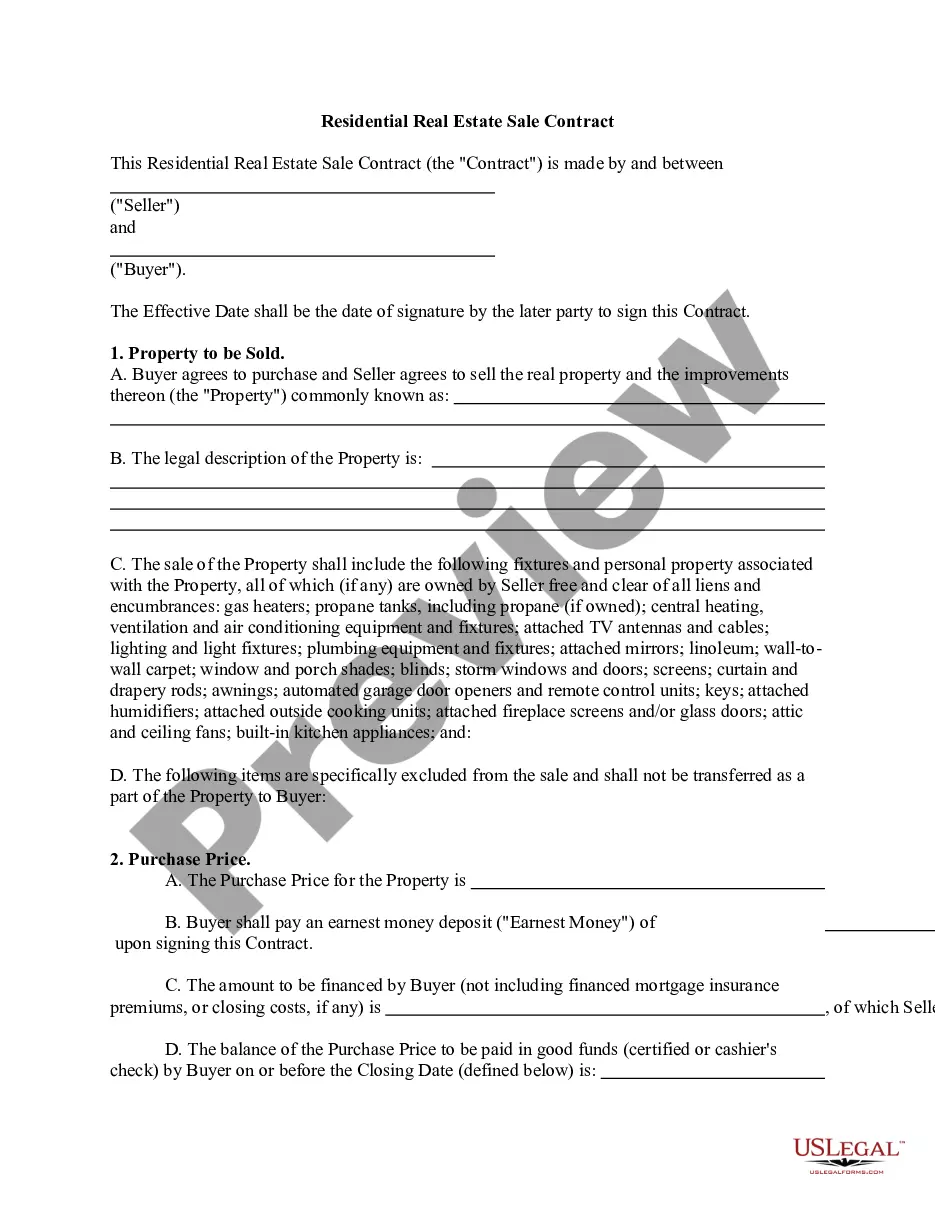

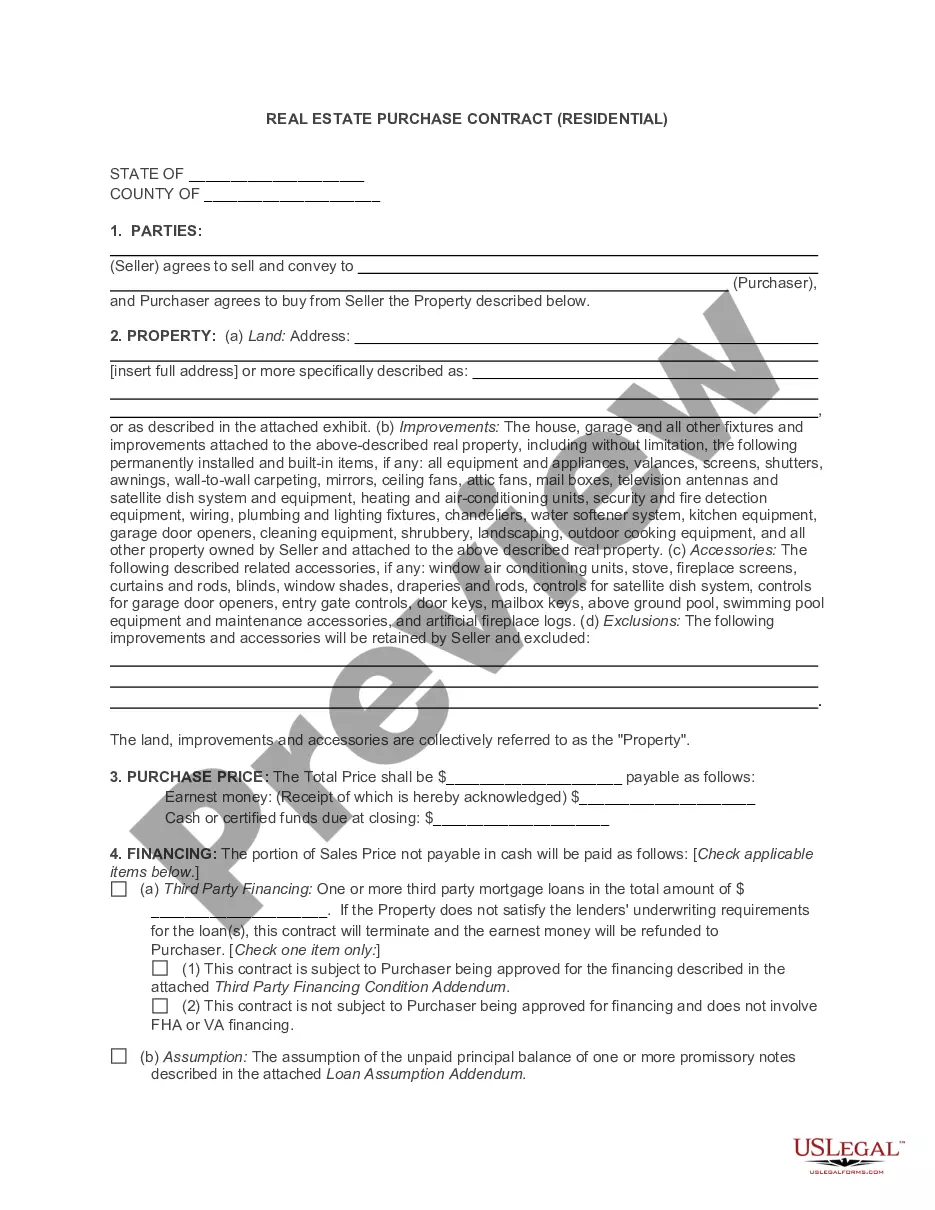

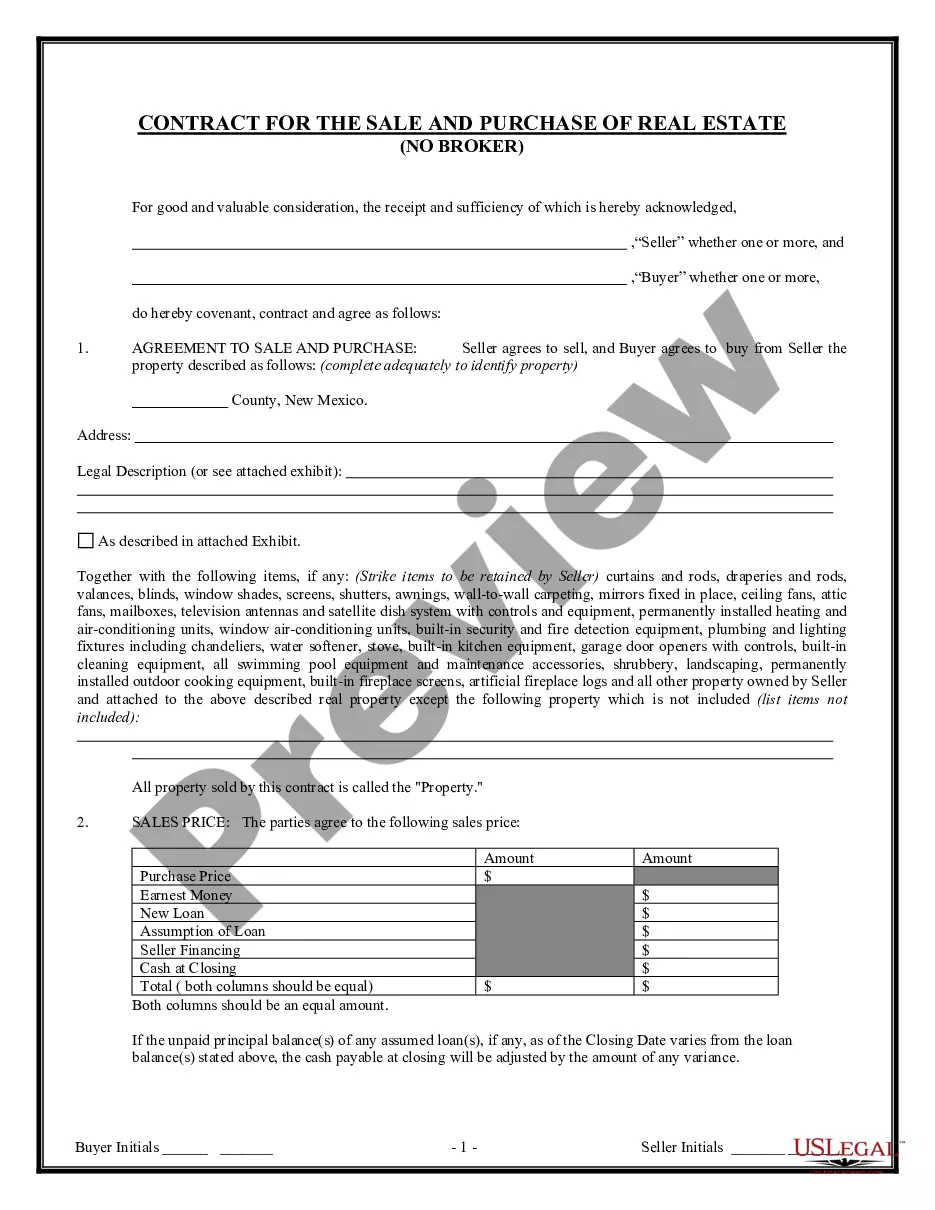

The Purchase Contract and Receipt - Residential is a legal document used for the sale of residential real estate. It serves as both a contract and a receipt, detailing the terms of sale between a seller and purchaser. This form is suitable for various real estate transactions, including the sale of unimproved land, but differs from longer contracts typically used for fully developed properties. Always ensure it meets your specific needs and circumstances.

What’s included in this form

- Details of the seller and purchaser, including names and addresses.

- Description and location of the real property being sold.

- Terms of the sale, including purchase price and payment methods.

- Provisions regarding title transfer and potential defaults.

- Broker information and commission structure.

- Critical dates for acceptance, closing, and possession.

When to use this document

This form is useful when you are ready to purchase or sell a residential property. It is appropriate for both simple transactions involving unimproved land and slightly more complex residential sales. Use this contract when you have agreed on the terms of sale but need a structured way to formalize and document the agreement.

Who needs this form

This form should be used by:

- Individuals looking to buy or sell residential property.

- Real estate agents who need a streamlined process for clients.

- Investors interested in purchasing unimproved land or residential properties.

How to prepare this document

- Identify the parties involved by entering the seller's and purchaser's information.

- Specify the real property location and legal description.

- Enter the purchase price and outline the payment terms.

- Include any additional provisions that may affect the transaction.

- Ensure that all parties review and sign the contract to acknowledge acceptance.

Is notarization required?

This document requires notarization to meet legal standards. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include complete and accurate property descriptions.

- Not specifying earnest money details and payment method clearly.

- Overlooking critical dates related to acceptance and closing.

- Neglecting to review state-specific laws that may impact the sale.

Benefits of using this form online

- Convenient access allowing you to download and complete the form anytime.

- Editability ensures you can customize the document to fit specific needs.

- Reliability, as forms are drafted by licensed attorneys to comply with legal standards.

Looking for another form?

Form popularity

FAQ

The sale of farm land is capital gain income and it will show on schedule D and form 8949. To enter the sale in TurboTax, go to: Go to the Federal Taxes category at the top of the window. Choose the Wages and Income subcategory.

It depends on how long you owned and lived in the home before the sale and how much profit you made. If you owned and lived in the place for two of the five years before the sale, then up to $250,000 of profit is tax-free. If you are married and file a joint return, the tax-free amount doubles to $500,000.

Losses are not allowed for personal-use items. Unless you can prove that you bought it exclusively for business, rental, or investment use and never used it personally or had personal intentions for the property, the loss is not deductible.

Hanging on until the gain qualifies for favorable long-term capital gains tax treatment if you've owned the property for less than a year. Lowering your taxable income. Receiving installments. Exchanging instead of selling. Donating the land to charity.

Hanging on until the gain qualifies for favorable long-term capital gains tax treatment if you've owned the property for less than a year. Lowering your taxable income. Receiving installments. Exchanging instead of selling. Donating the land to charity.

1Exemptions under Section 54F, when you buy or construct a Residential Property.2Purchase Capital Gains Bonds under Section 54EC.3Investing in Capital Gains Accounts Scheme.4Purchase Capital Gains Bonds under Section 54EC.Best and safe way to save capital gains tax on Property Sale\nwww.ashianahousing.com > real-estate-blog > 3-best-and-safe-ways-to-save...

Short-term capital gains are taxed as part of your ordinary income, meaning that the regular income tax brackets of 10 to 37 percent apply. Depending on where you live or where the land you are selling is located, you may also be liable for capital gain taxes at the state level.

If you have sold land or investment real estate and realized a profit, the IRS is likely standing in line to collect capital gains tax on the sale. Fortunately, you can avoid paying tax by completing a 1031 Exchange, where the proceeds from the sale are used to purchase similar land or property.

Capital asset is defined to include various assets including real estate. So, any gain on sale of land or building by the owner is taxable as capital gain. Sale consideration reduced by cost of acquisition (indexed cost of acquisition for land or building held for more than 24 months) is taxable as capital gain.