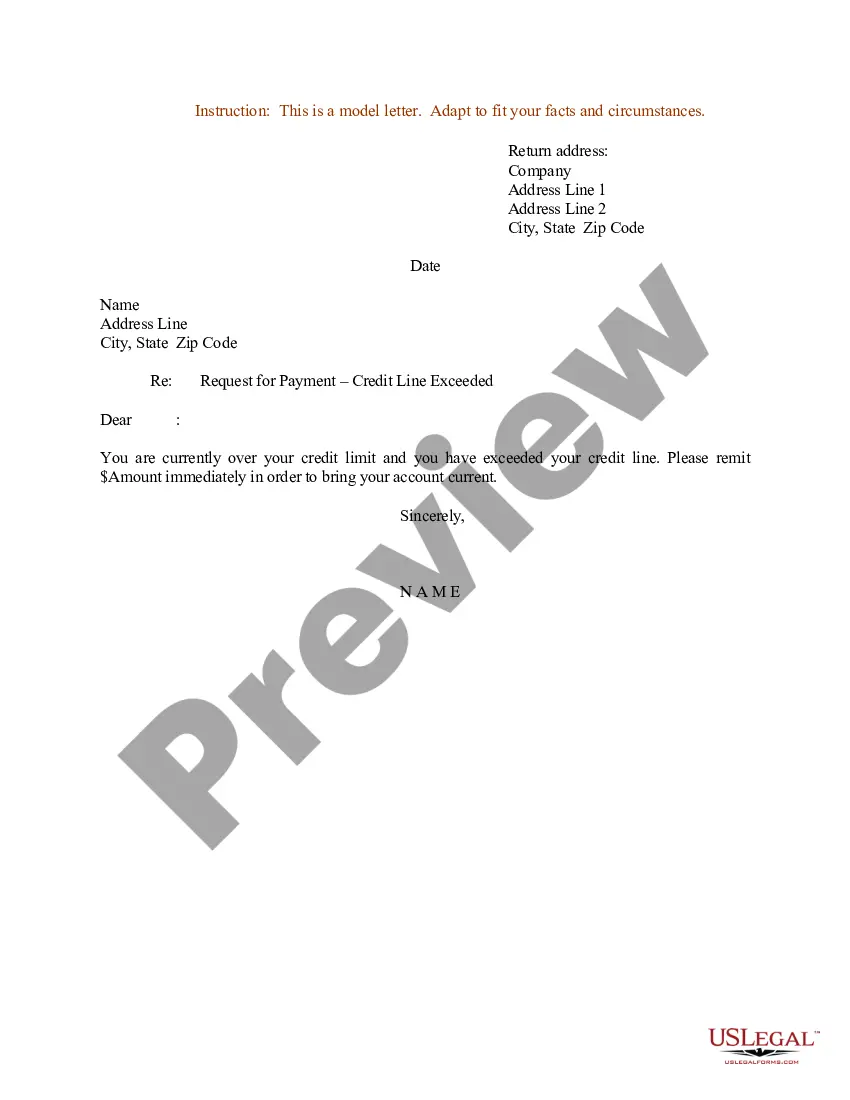

Request for Payment - Credit Line Exceeded

Overview of this form

The Request for Payment - Credit Line Exceeded form is a formal document used by creditors to notify account holders that they have exceeded their approved line of credit. This request urges the account holder to make a payment to bring their balance within the permitted limit. This form is specifically tailored for situations where the outstanding balance must be addressed to maintain financial credibility, differing from general payment requests by emphasizing credit limit adherence.

Key parts of this document

- Sender's Address: Include the address of the creditor.

- Date: The date on which the request is issued.

- Account Information: Details about the account where the credit line has been exceeded.

- Requested Amount: The specific payment amount required to reduce the balance.

- Instructions for Payment: Guidance on what to do if the payment cannot be made immediately.

- Signature and Title: The authorized representative's name and designation from the creditor's company.

Situations where this form applies

This form should be used when a debtor exceeds their credit line and the creditor needs to formally request a payment to bring the account back into good standing. It is important for businesses to manage credit risks proactively, and using this form helps establish clear communication with the debtor about their obligation.

Who can use this document

This form is suitable for:

- Creditors or businesses that extend credit to customers.

- Account managers overseeing customer accounts with credit limits.

- Financial institutions managing loan and credit lines.

Steps to complete this form

- Identify the creditor's address at the top of the form.

- Fill in the date of the notice.

- Provide the debtor's name and address accurately.

- Specify the account number associated with the exceeded credit line.

- Clearly state the payment amount needed to reduce the balance.

- Sign the document and include your name and title as the representing authority.

Notarization guidance

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include the correct account number.

- Not specifying the exact payment amount required.

- Leaving out the signature from the authorized representative.

- Using incorrect or outdated contact information for the debtor.

Benefits of completing this form online

- Convenient access for quick downloading and customization.

- Editable fields allow for easy adjustments to meet specific needs.

- Reliability of attorney-drafted templates ensures legal adherence.

Legal use & context

- This form is a formal request and can serve as evidence of the creditor's efforts to collect the owed amount.

- Proper completion could prevent further collection actions if payment is made promptly.

Looking for another form?

Form popularity

FAQ

Generally, your limit is included on your credit card statement or is available via your online account. You can also call the number on the back of your card to ask your provider.

A credit limit is the maximum amount you can charge on a revolving credit account, such as a credit card. As you use your card, the amount of each purchase is subtracted from your credit limit. And the number you're left with is known as your available credit.

The customer knows where they stand and can plan purchases ingly. If the customer needs to purchase above its credit limit, it can either pay down the account or pay cash for the new shipments.

It's a good idea to attach a copy of their current balance so the customer can see exactly how much they've exceeded their designated credit limit. You can also attach a copy of the credit policy and credit terms the customer agreed to when they opened an account with your financial institution.

I am writing to request an increase of $5,000.00 in my credit limit with Doe. My current limit is insufficient to cover my monthly purchases at your firm. As you know, my credit history with you is spotless. I have always made payments on time, so I do not anticipate problems handling the increased limit.

Your credit card company may decide to automatically increase your credit limit because of changes in your personal situation or improvements in your credit scores. Or you could request an increase yourself. Remember, a lender isn't guaranteed to give you an increase when you ask for one.

A good guideline is the 30% rule: Use no more than 30% of your credit limit to keep your debt-to-credit ratio strong. Staying under 10% is even better. In a real-life budget, the 30% rule works like this: If you have a card with a $1,000 credit limit, it's best not to have more than a $300 balance at any time.