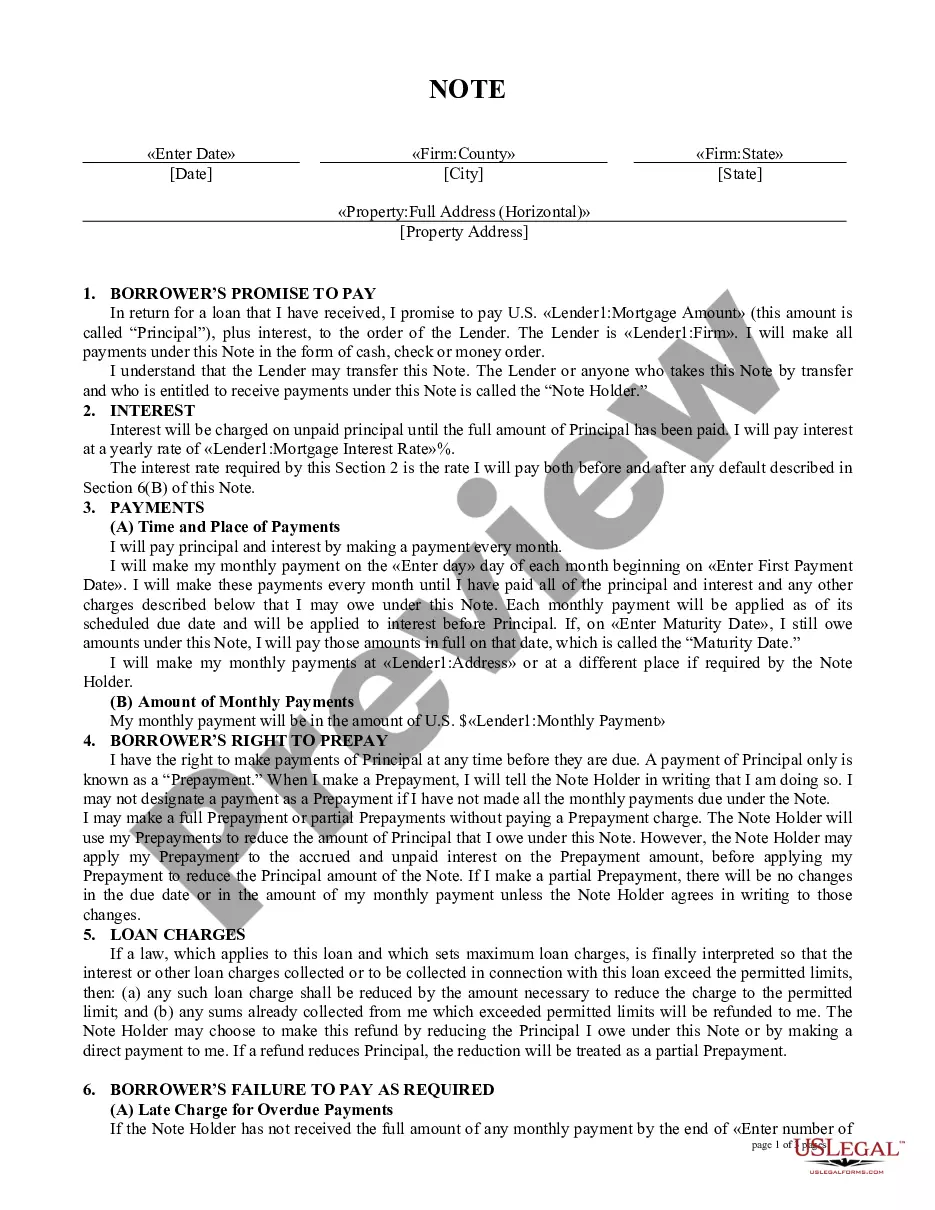

Texas Adjustable Rate Rider - Variable Rate Note

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Adjustable Rate Rider - Variable Rate Note?

Are you in a scenario where you require documents for various organizations or specific purposes almost every day.

There are numerous legal document templates available online, but finding ones you can rely on is not easy.

US Legal Forms offers thousands of form templates, including the Texas Adjustable Rate Rider - Variable Rate Note, that are designed to meet federal and state regulations.

Utilize US Legal Forms, the most extensive collection of legal forms, to save time and avoid errors.

The service provides professionally crafted legal document templates that you can use for various purposes. Create an account on US Legal Forms and start making your life easier.

- If you are already acquainted with the US Legal Forms website and have an account, just Log In.

- After that, you can download the Texas Adjustable Rate Rider - Variable Rate Note template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Find the form you need and ensure it is for the correct city/region.

- Use the Preview button to review the form.

- Check the details to ensure you have selected the correct form.

- If the form is not what you’re looking for, utilize the Search field to find the form that meets your needs.

- Once you find the correct form, click Get now.

- Choose the pricing plan you want, fill in the required information to set up your account, and pay for the order using your PayPal or credit card.

- Select a suitable document format and download your copy.

- Find all the document templates you have purchased in the My documents menu. You can download another copy of the Texas Adjustable Rate Rider - Variable Rate Note anytime, if necessary. Just click on the desired form to download or print the document template.