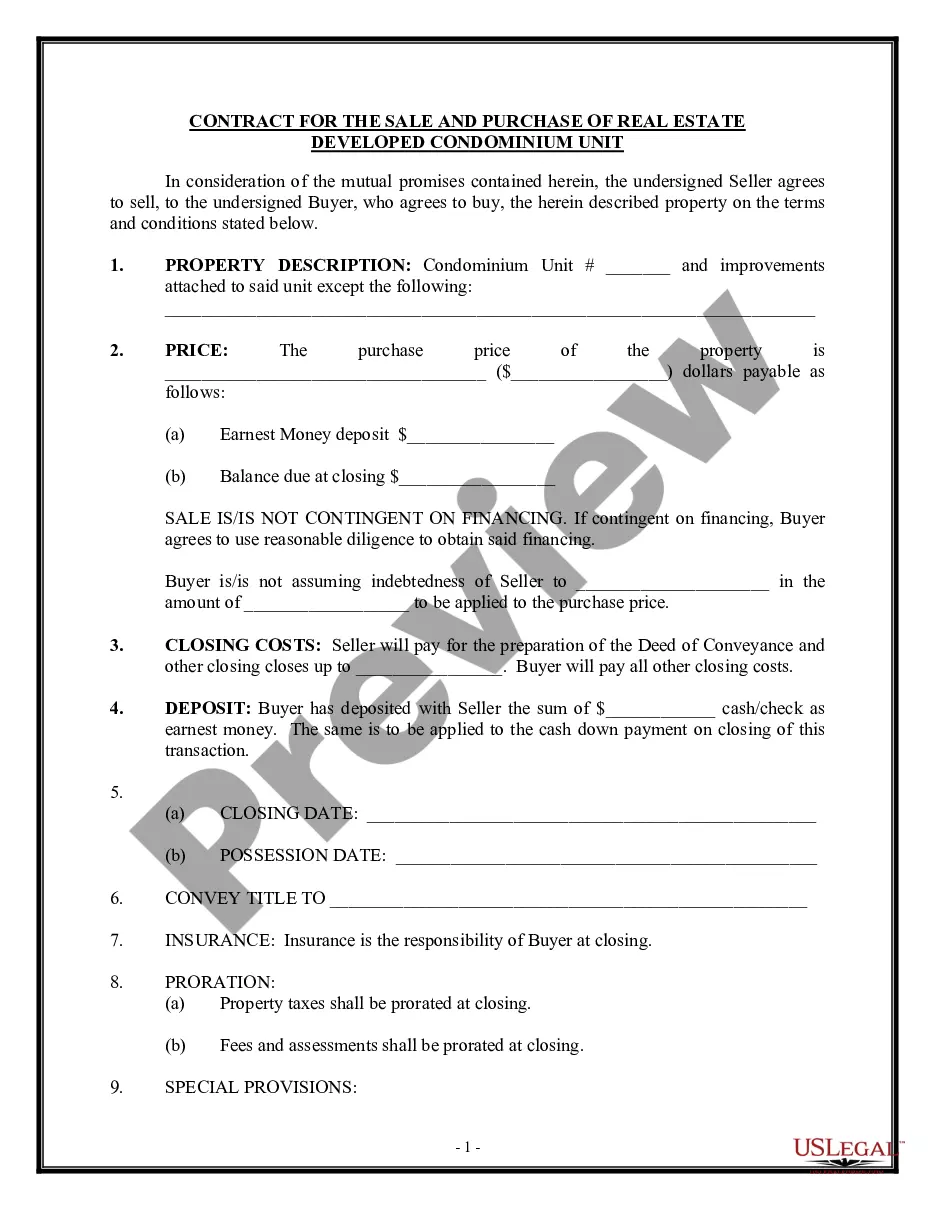

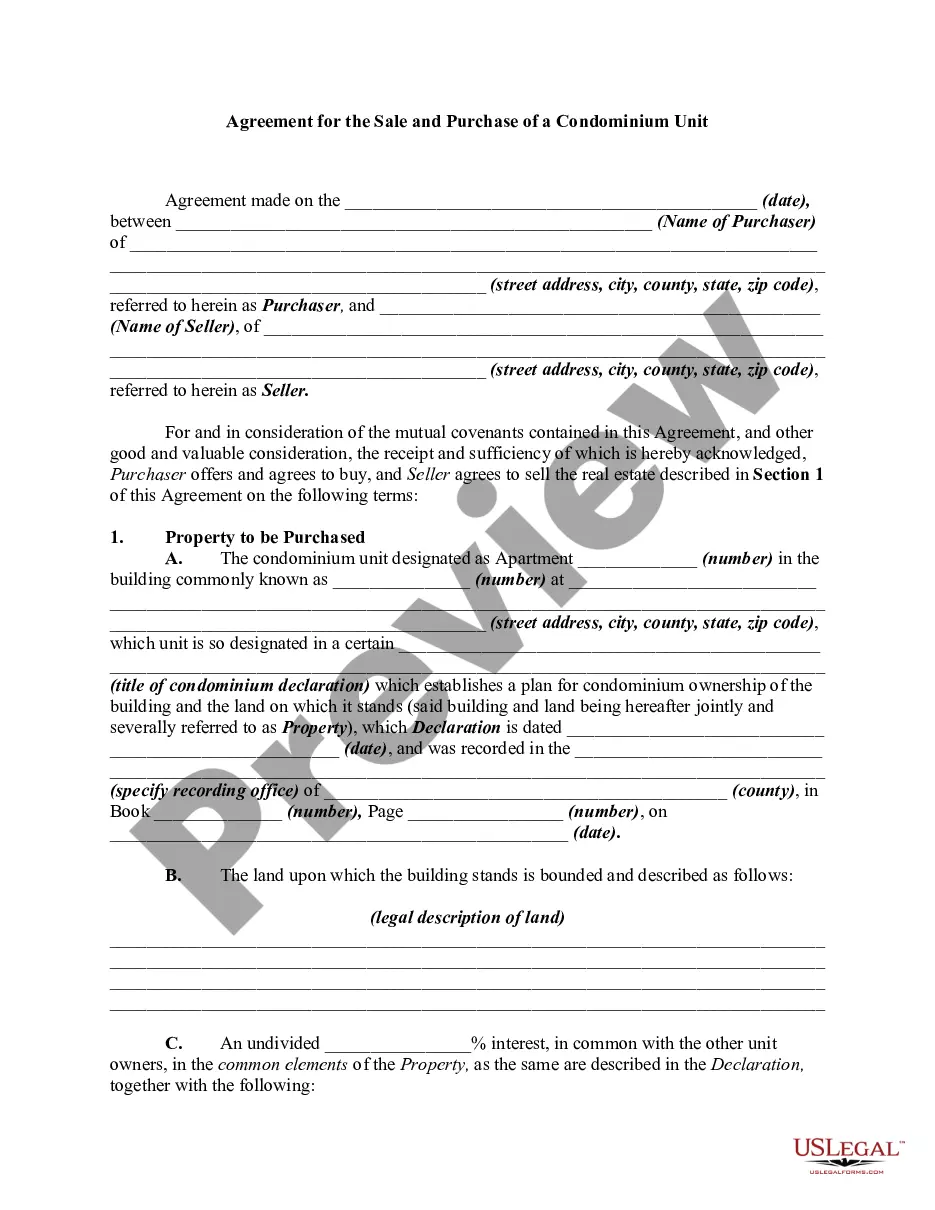

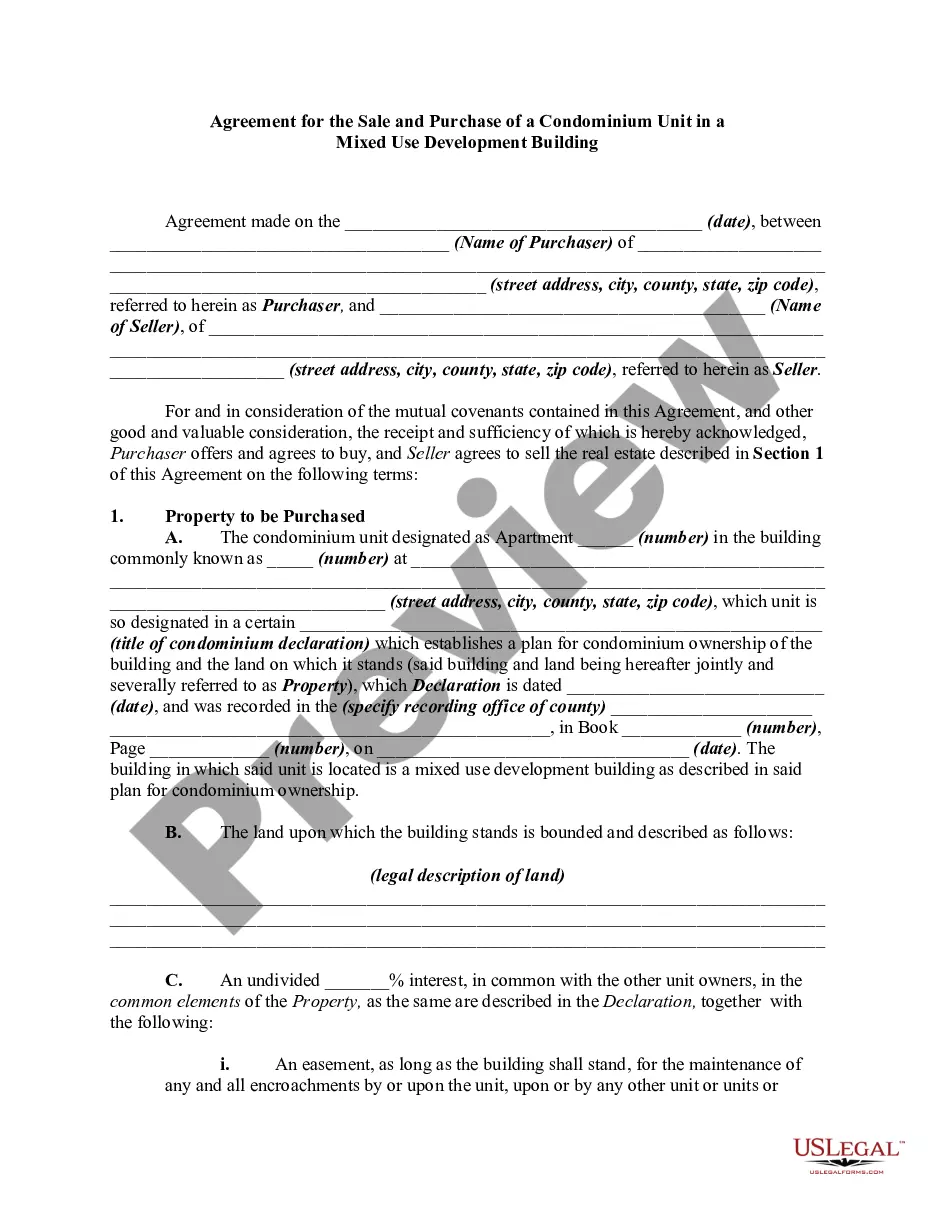

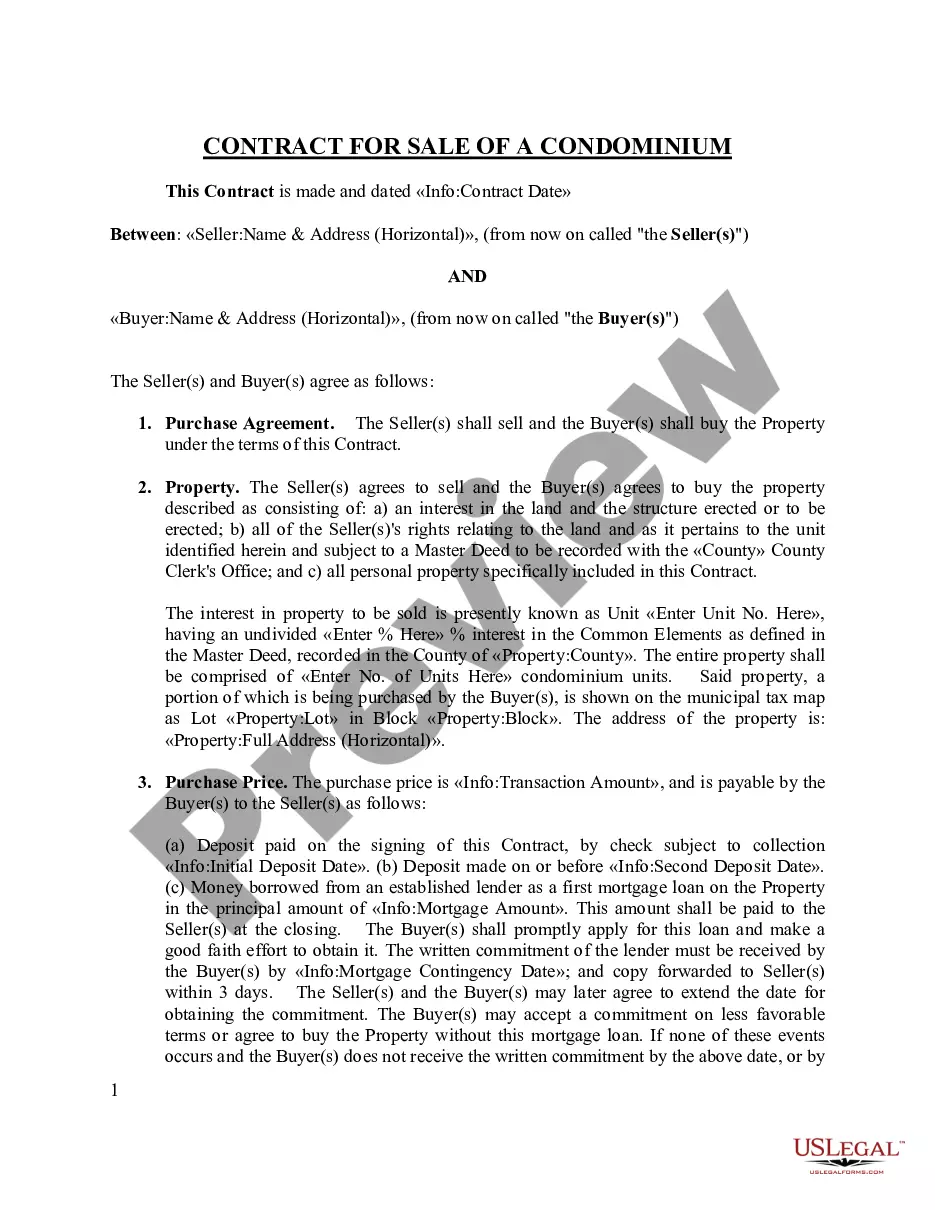

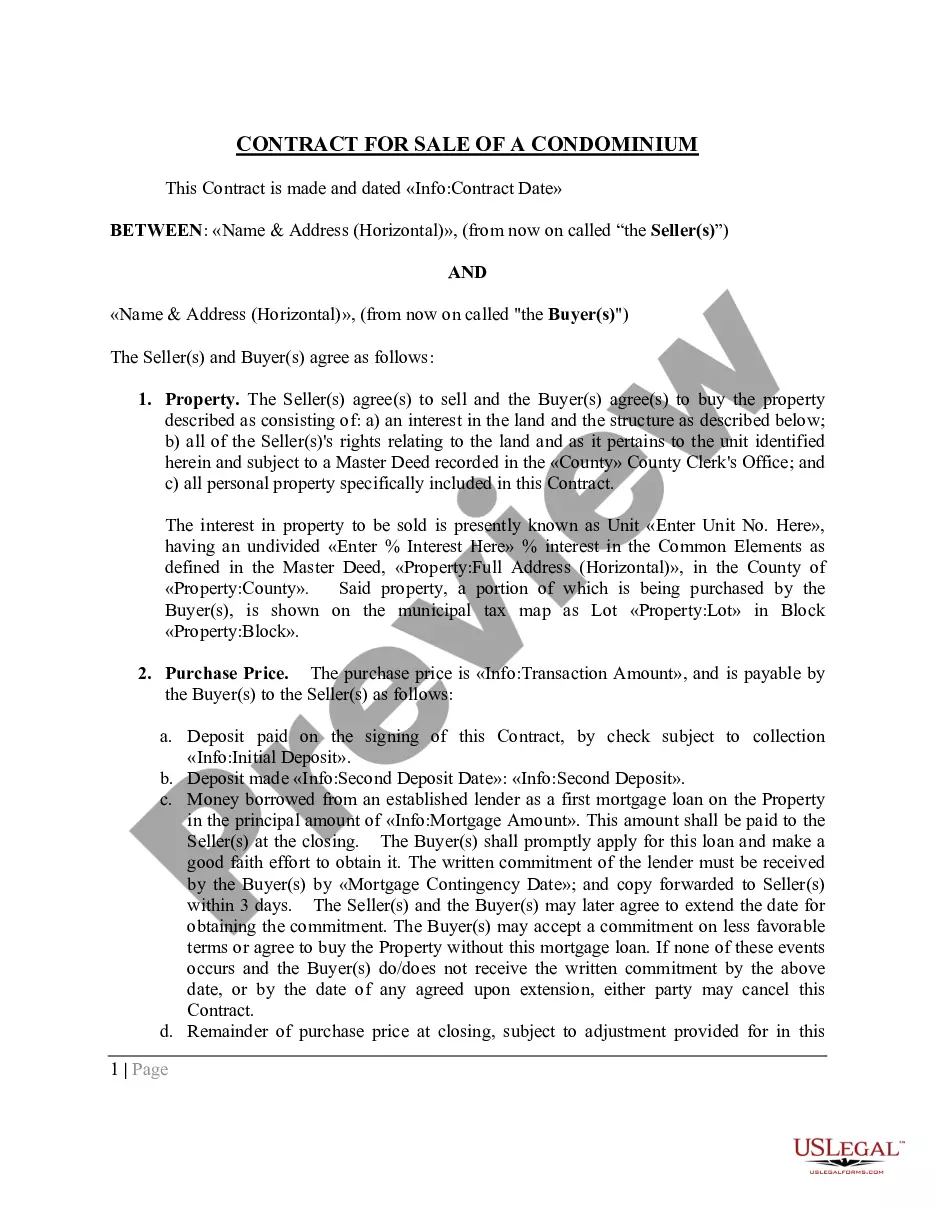

Texas Agreement to Purchase Condominium with Purchase Money Mortgage Financing by Seller, and Subject to Existing Mortgage

Description

How to fill out Agreement To Purchase Condominium With Purchase Money Mortgage Financing By Seller, And Subject To Existing Mortgage?

Choosing the best authorized record design can be a have difficulties. Obviously, there are tons of web templates accessible on the Internet, but how can you discover the authorized kind you will need? Take advantage of the US Legal Forms website. The support delivers a huge number of web templates, like the Texas Agreement to Purchase Condominium with Purchase Money Mortgage Financing by Seller, and Subject to Existing Mortgage, which you can use for business and personal requires. All of the forms are checked out by specialists and meet up with federal and state specifications.

Should you be previously listed, log in to your bank account and click on the Acquire option to obtain the Texas Agreement to Purchase Condominium with Purchase Money Mortgage Financing by Seller, and Subject to Existing Mortgage. Make use of your bank account to appear from the authorized forms you might have bought formerly. Proceed to the My Forms tab of your bank account and obtain yet another backup of the record you will need.

Should you be a fresh end user of US Legal Forms, allow me to share basic recommendations that you should follow:

- Very first, make sure you have chosen the right kind for the metropolis/county. You may look over the form while using Preview option and study the form outline to make certain this is basically the best for you.

- If the kind fails to meet up with your expectations, use the Seach industry to get the right kind.

- Once you are certain that the form is suitable, click the Acquire now option to obtain the kind.

- Pick the costs plan you desire and enter in the required info. Build your bank account and purchase an order with your PayPal bank account or Visa or Mastercard.

- Choose the data file formatting and obtain the authorized record design to your device.

- Total, change and print out and sign the acquired Texas Agreement to Purchase Condominium with Purchase Money Mortgage Financing by Seller, and Subject to Existing Mortgage.

US Legal Forms will be the largest library of authorized forms where you can find a variety of record web templates. Take advantage of the service to obtain skillfully-manufactured files that follow express specifications.

Form popularity

FAQ

How Do You Structure a Seller Financing Deal? Don't use current market interest rates to create the interest rate for your seller financing loan. ... The higher the price?the longer the loan term. ... Bring as little cash to the deal as possible. ... Defer payments if possible. ... Exchange down payment for needed repairs.

Cons Usually charges a higher interest rate compared to a traditional mortgage. Typically required a balloon payment at the end of the loan term. Sellers may not agree to this arrangement if the buyer has poor credit. A due-on-sale clause may prevent the seller from entering this type of arrangement.

An owner financing contract is an agreement between the owner or seller of the property and the buyer. The seller agrees to finance the balance of the purchase price (not including the down payment) with the buyer making payments to the seller.

In a traditional mortgage, the bank holds the deed. With a purchase-money mortgage, the seller holds the deed.

This is called a purchase money mortgage, because this type of mortgage usually replaces part or all of the cash that the buyer would otherwise pay the seller. For example, a buyer might pay for a $500,000 house with a $400,000 bank mortgage, $60,000 in cash, and a $40,000 purchase money mortgage.

A purchase-money mortgage is a mortgage issued to the borrower by the seller of a home as part of the purchase transaction. Also known as a seller or owner financing, this is usually done in situations where the buyer cannot qualify for a mortgage through traditional lending channels.

For example, if a seller-financed loan is for $100,000 at an interest rate of 8%, you would calculate that $100,000 x 0.08, which means $8,000 in interest for the year. In this scenario, a $100,000 loan at 8% would look like $666.67 in a monthly interest-only payment.

Examples of seller financing are all-inclusive mortgages, rent-to-own agreements, second mortgages or junior mortgages, wrap-around agreements, and land contracts.

The seller's financing typically runs only for a fairly short term, such as five years. At the end of that period, a balloon payment is due. The expectation is usually that the initial seller-financed purchase will improve the buyer's creditworthiness and allow them to accumulate equity in the home.

Here are three main ways to structure a seller-financed deal: Use a Promissory Note and Mortgage or Deed of Trust. If you're familiar with traditional mortgages, this model will sound familiar. ... Draft a Contract for Deed. ... Create a Lease-purchase Agreement.