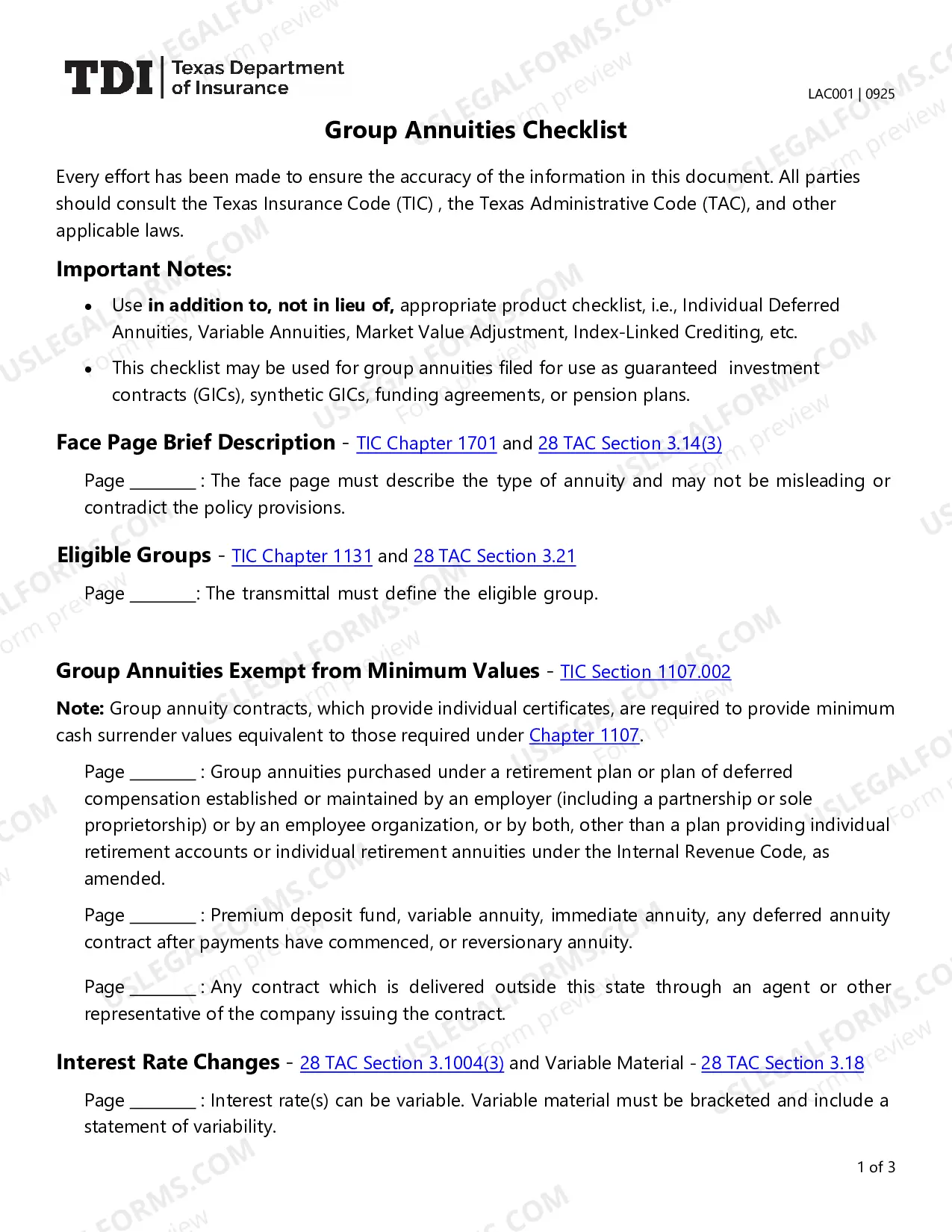

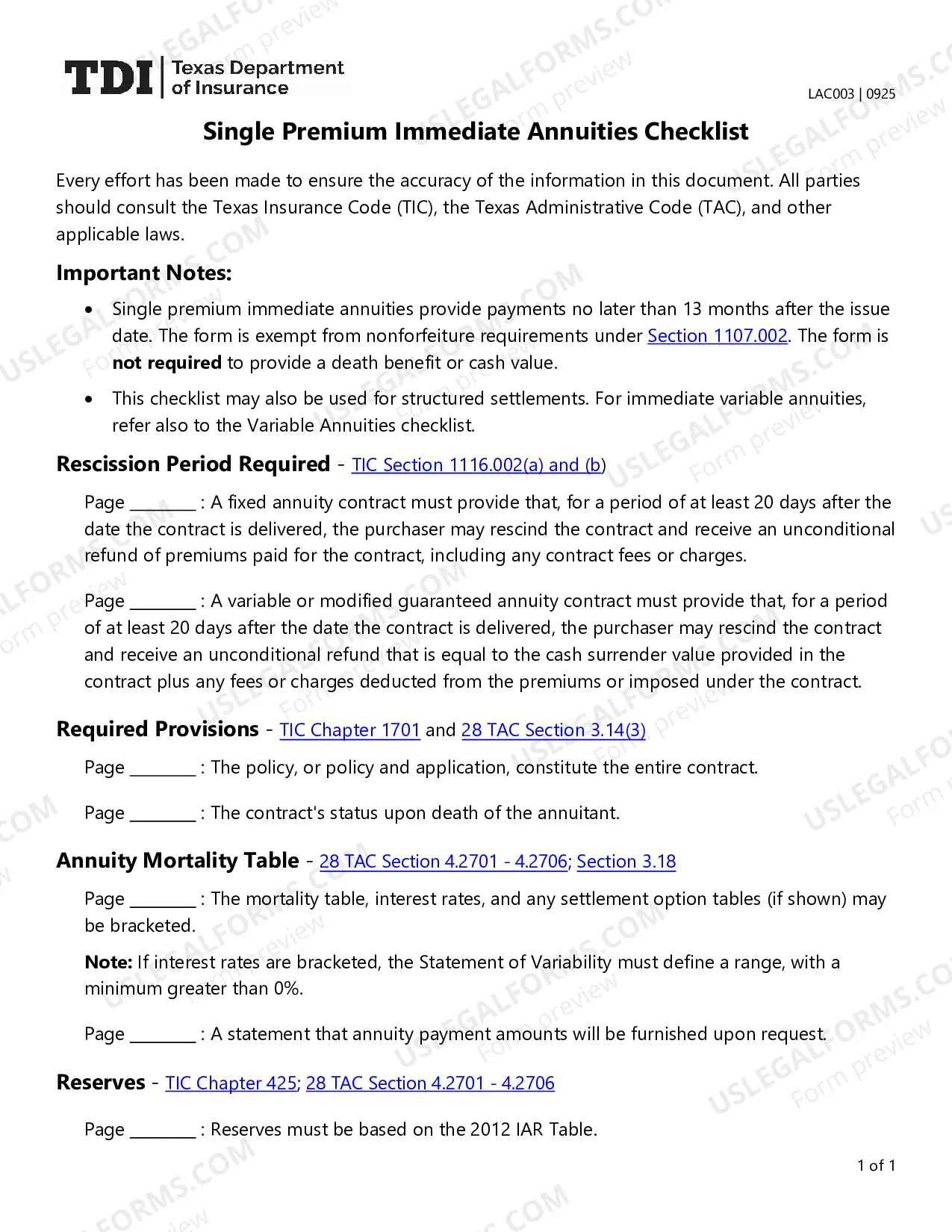

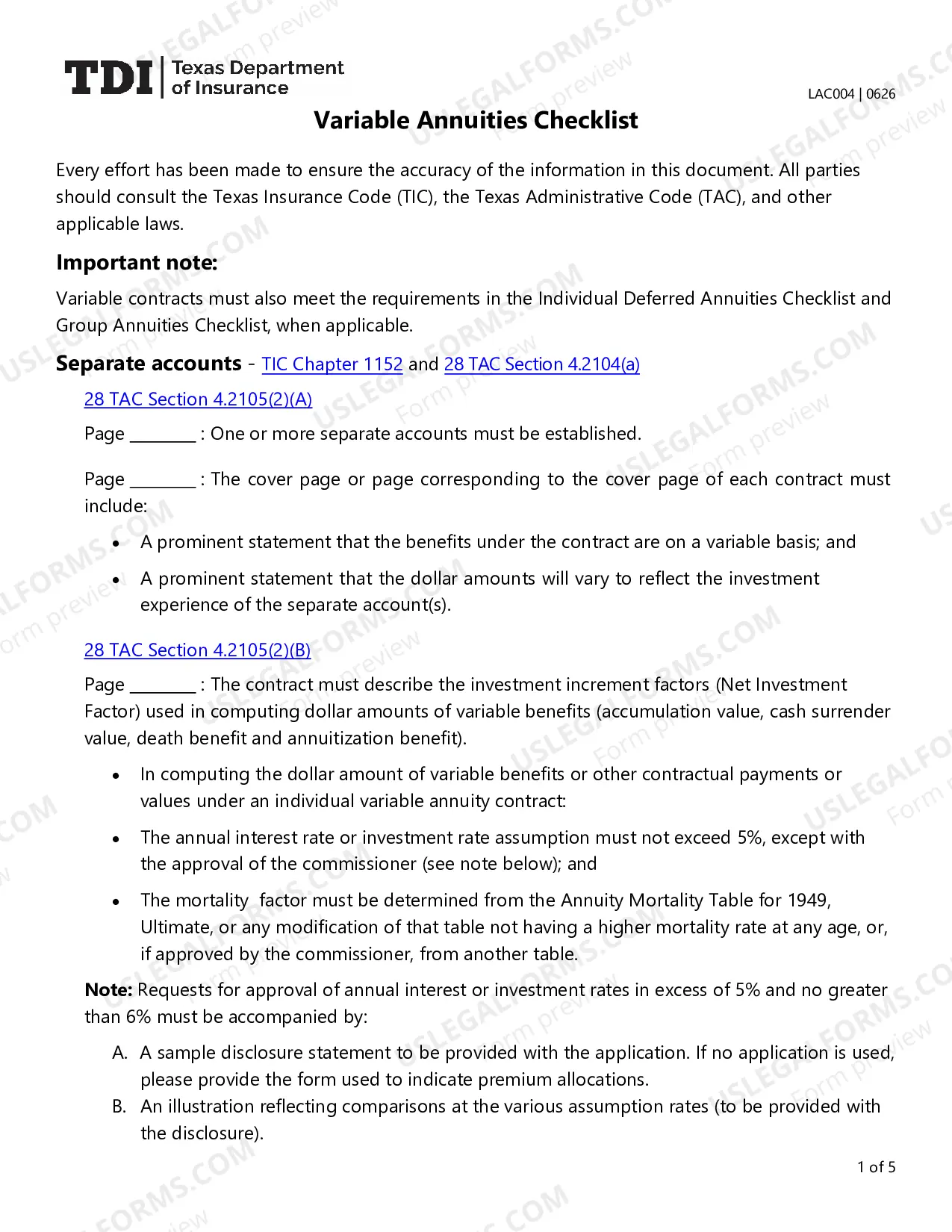

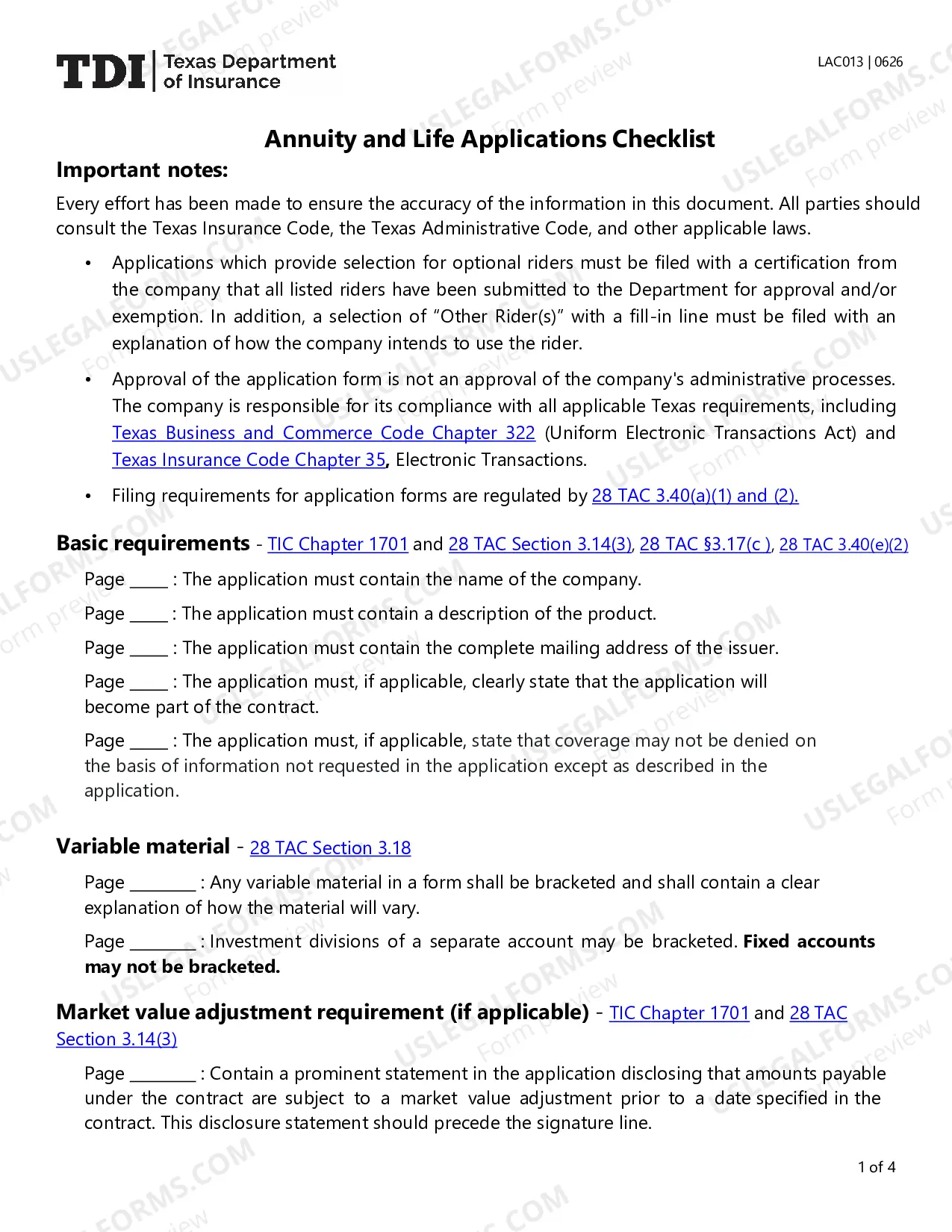

Texas Individual Deferred Annuities Checklist is a comprehensive set of guidelines used to ensure that the purchase of deferred annuities complies with the regulations of the Texas Department of Insurance. The checklist outlines the necessary documentation required for the purchase of an annuity contract, including a signed application, proof of age, and medical underwriting. It also provides guidance on how to complete the application, how to review the contract, and how to make changes to the annuity at a later date. There are three types of Texas Individual Deferred Annuities Checklist: Fixed Annuities, Index Annuities, and Variable Annuities. Each type of annuity requires different documentation and considerations, so it is important to consult the appropriate checklist when purchasing a deferred annuity.

Texas Individual Deferred Annuities Checklist

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Texas Individual Deferred Annuities Checklist?

US Legal Forms is the most simple and cost-effective way to find appropriate formal templates. It’s the most extensive online library of business and personal legal documentation drafted and verified by lawyers. Here, you can find printable and fillable blanks that comply with federal and local laws - just like your Texas Individual Deferred Annuities Checklist.

Obtaining your template takes just a few simple steps. Users that already have an account with a valid subscription only need to log in to the web service and download the document on their device. Afterwards, they can find it in their profile in the My Forms tab.

And here’s how you can obtain a professionally drafted Texas Individual Deferred Annuities Checklist if you are using US Legal Forms for the first time:

- Look at the form description or preview the document to guarantee you’ve found the one corresponding to your requirements, or locate another one utilizing the search tab above.

- Click Buy now when you’re sure of its compatibility with all the requirements, and select the subscription plan you like most.

- Register for an account with our service, log in, and pay for your subscription using PayPal or you credit card.

- Choose the preferred file format for your Texas Individual Deferred Annuities Checklist and save it on your device with the appropriate button.

Once you save a template, you can reaccess it whenever you want - just find it in your profile, re-download it for printing and manual fill-out or import it to an online editor to fill it out and sign more effectively.

Take advantage of US Legal Forms, your reliable assistant in obtaining the required formal paperwork. Give it a try!

Form popularity

FAQ

The Deferred Annuity Formula Calculating your deferred annuity returns involves a simple formula: FV = P (1 + r/n)^(nt). Here, FV is the future value of your annuity, P is the principal amount, r is the annual interest rate, and n is the number of times that interest is compounded per year.

WHAT LICENSE IS REQUIRED TO SELL VARIABLE CONTRACTS? You must hold the Insurance Producer license with the Variable Life and Variable Annuity Products LOA.

Agents who sell variable annuities must be registered with FINRA and have a TDI license. TDI also works with the Texas State Securities Board on issues involving agents that sell variable annuities.

Such advisors may only need a Series 6 license if they just sell insurance, annuities, and certain types of mutual funds, not individual stocks. Series 6 holders, however, are not authorized to sell stocks, exchange-traded funds (ETFs), or bonds.

Agents and companies must have a Texas insurance license to legally sell annuities in the state.

A deferred annuity is an insurance contract that promises to pay the annuity owner either a lump sum or a regular income at some future date. People frequently buy deferred annuities to supplement Social Security benefits and other income streams in retirement.

If an insurance agent offers products that are considered securities?such as variable annuity contracts or variable life insurance policies?the agent must also be licensed as a registered financial professional and comply with FINRA rules.

A deferred annuity has two phases: the accumulation phase, where you let your money grow for a period of time, and the payout phase. During accumulation, your money grows tax-deferred until you withdraw it, either as a lump sum or as a series of payments.