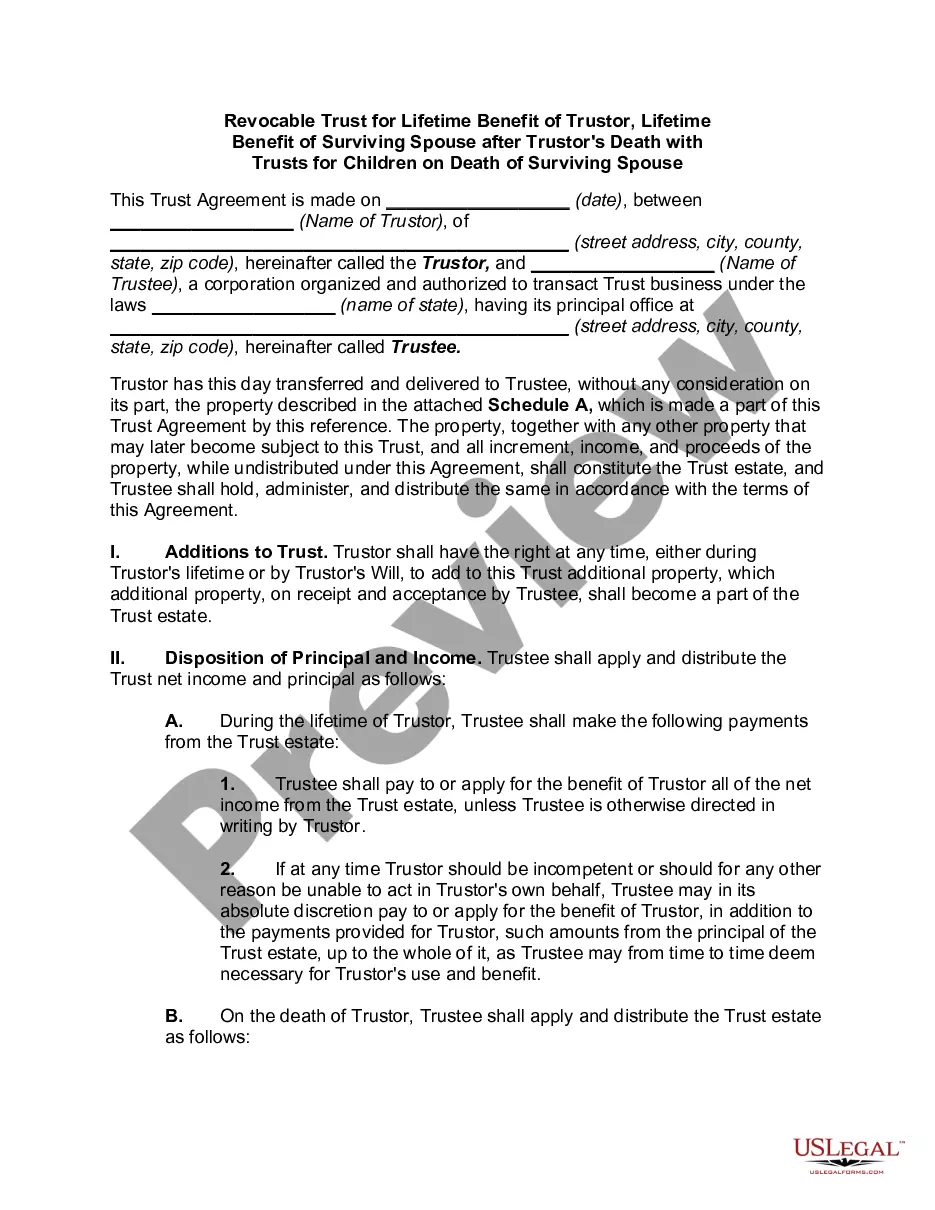

Tennessee Marital-deduction Residuary Trust with a Single Trustor and Lifetime Income and Power of Appointment in Beneficiary Spouse

Description

How to fill out Marital-deduction Residuary Trust With A Single Trustor And Lifetime Income And Power Of Appointment In Beneficiary Spouse?

Are you presently within a situation the place you will need files for possibly organization or individual purposes virtually every working day? There are a variety of lawful papers layouts available online, but locating types you can rely on isn`t effortless. US Legal Forms offers a huge number of type layouts, much like the Tennessee Marital-deduction Residuary Trust with a Single Trustor and Lifetime Income and Power of Appointment in Beneficiary Spouse, that happen to be composed to meet state and federal requirements.

Should you be previously acquainted with US Legal Forms site and get a free account, just log in. After that, you are able to acquire the Tennessee Marital-deduction Residuary Trust with a Single Trustor and Lifetime Income and Power of Appointment in Beneficiary Spouse design.

If you do not have an bank account and wish to start using US Legal Forms, follow these steps:

- Obtain the type you will need and make sure it is for the right town/county.

- Take advantage of the Review switch to examine the shape.

- See the description to actually have chosen the proper type.

- When the type isn`t what you`re seeking, make use of the Search industry to obtain the type that meets your requirements and requirements.

- Once you discover the right type, just click Buy now.

- Pick the rates plan you would like, submit the necessary information to create your money, and buy the transaction using your PayPal or charge card.

- Pick a convenient file structure and acquire your duplicate.

Locate all the papers layouts you may have purchased in the My Forms menus. You can get a further duplicate of Tennessee Marital-deduction Residuary Trust with a Single Trustor and Lifetime Income and Power of Appointment in Beneficiary Spouse any time, if needed. Just click on the required type to acquire or printing the papers design.

Use US Legal Forms, the most substantial variety of lawful types, to conserve time and steer clear of mistakes. The support offers professionally produced lawful papers layouts which can be used for a variety of purposes. Generate a free account on US Legal Forms and begin creating your way of life easier.

Form popularity

FAQ

A marital deduction trust is a trust where transfers of property between married partners are free of federal transfer tax. A marital deduction trust can take one of two forms: A life estate coupled with a general power of appointment given to the spouse, or. A Qualified Terminable Interest Property (QTIP) trust.

The unlimited marital deduction is a provision in the U.S. Federal Estate and Gift Tax Law that allows an individual to transfer an unrestricted amount of assets to their spouse at any time, including at the death of the transferor, free from tax.

For example, if an individual were to convey by will an entire estate to a surviving spouse, the decedent's estate would have no estate tax liability. The marital deduction is effectively a deferral of the estate tax to the date of the surviving spouse's death.

A general power of appointment is defined under Florida's elective share statute as ?a power of appointment under which the holder of the power, whether or not the holder has the capacity to exercise it, has the power to create a present or future interest in the holder, the holder's estate, or the creditors of either.

Property interests passing to a surviving spouse that are not included in the decedent's gross estate do not qualify for the marital deduction. Expenses, indebtedness, taxes, and losses chargeable against property passing to the surviving spouse will reduce the marital deduction.

The ?unlimited marital deduction? refers to the fact that gifts to a spouse, made during your lifetime or after death, are always exempt from the gift and estate tax. Moreover, there is no limit to the marital deduction.

Terminable interests do not qualify for the marital deduction (Sec. 2056(b)(1)). An example of a terminable interest is where the decedent leaves property to a surviving spouse for the spouse's lifetime, with a remainder interest to the decedent's children.

If the surviving spouse accepts the assets or tries to control what is done with those assets before or after they have been disclaimed, the tax exemption benefits are lost.