Tennessee Installments Fixed Rate Promissory Note Secured by Personal Property

What is this form?

The Tennessee Installments Fixed Rate Promissory Note Secured by Personal Property is a legal document that outlines a borrower's promise to repay a loan with fixed monthly payments secured by personal property. This form is specifically designed for loans that involve collateral, distinguishing it from unsecured promissory notes, thereby providing additional security for the lender.

Key parts of this document

- Borrower's promise to pay back the principal amount and interest to the lender.

- The specified interest rate and how it applies both before and after default.

- Details regarding the timing and amount of monthly payments.

- Conditions under which the borrower can prepay the loan and any associated penalties.

- Terms regarding late payments, default conditions, and possible late charges.

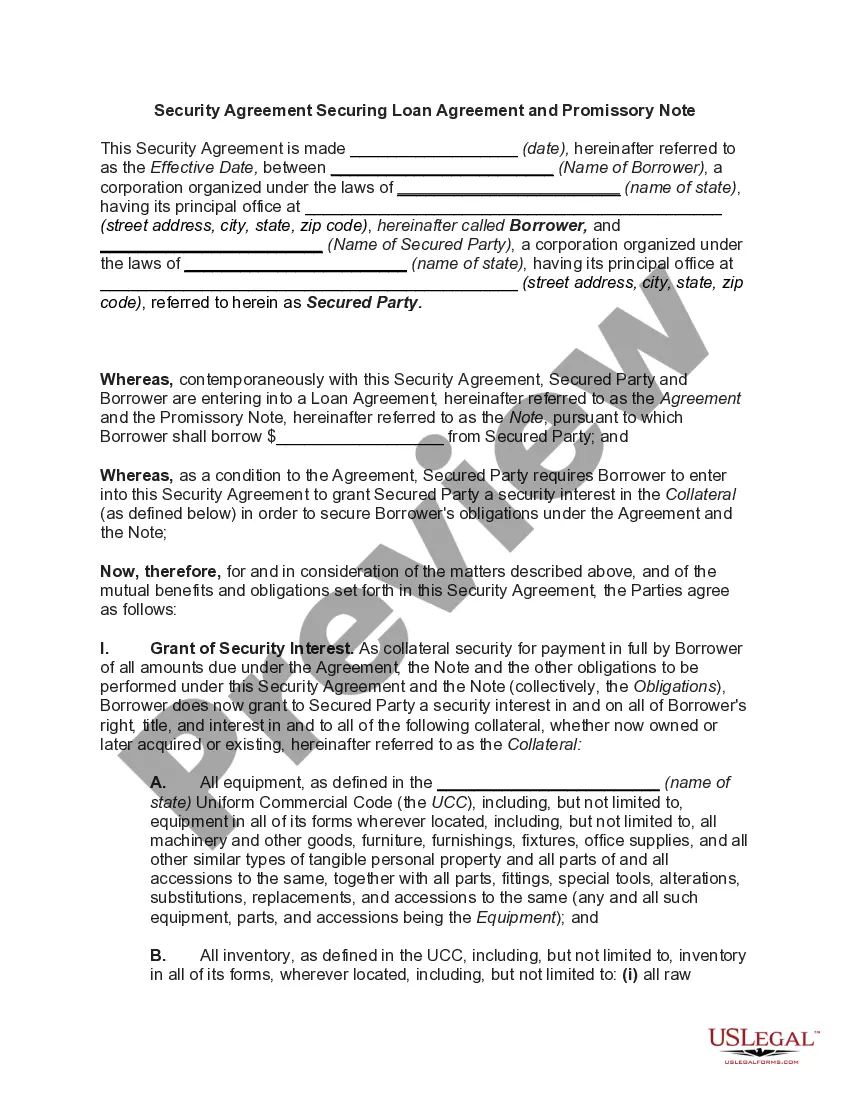

- Security clause where personal property is identified as collateral for the loan.

When this form is needed

This form is used when an individual or business borrows money and offers personal property as collateral. It is ideal for circumstances where the lender seeks extra assurance by securing the loan against valuable assets, which could include vehicles, equipment, or other personal items. If you are entering a loan agreement that requires this level of security, this form is essential.

Who can use this document

- Individuals or businesses seeking a secured loan in Tennessee.

- Lenders looking to safeguard their investment with collateral.

- Borrowers who prefer fixed monthly payments over a set loan duration.

- Those who want clear terms regarding interest, payment schedules, and consequences of default.

Completing this form step by step

- Identify all parties involved in the loan, including the borrower and lender.

- Enter the loan amount, interest rate, and specify the personal property that will serve as collateral.

- Fill in the repayment details, including the commencement date and the schedule of monthly payments.

- Clearly outline any rights regarding early repayment and prepayment penalties.

- Ensure all parties sign the document to validate the agreement.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, having the document notarized can help authenticate the signatures and may provide additional legal benefits.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Not specifying the collateral accurately, which may complicate enforcement of the security agreement.

- Failing to include all parties' signatures, making the agreement potentially unenforceable.

- Leaving sections blank, particularly regarding payment amounts and dates, which can lead to confusion.

Benefits of completing this form online

- Convenience of immediate access and download from the comfort of your home.

- Editability allows for adjustments to terms as necessary before finalizing the agreement.

- Reliability of forms drafted by licensed attorneys ensures compliance with legal standards.

Key takeaways

- The form secures a loan with personal property as collateral, providing safety for lenders.

- It outlines specific terms for repayment, including interest rates and late payment conditions.

- Proper completion and understanding of the terms are crucial for both parties.

Looking for another form?

Form popularity

FAQ

You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.

Unlike a mortgage or deed of trust, the promissory note isn't recorded in the county land records. The lender holds the promissory note while the loan is outstanding. When the loan is paid off, the note is marked as "paid in full" and returned to the borrower.

Types of Property that can be used as collateral. Speak to them in person. Draft a Demand / Notice Letter. Write and send a Follow Up Letter. Enlisting a Professional Collection Agency. Filing a petition or complaint in court. Selling the Promissory Note. Final Tips.

A promissory note is a contract, a binding agreement that someone will pay your business a sum of money. However under some circumstances if the note has been altered, it wasn't correctly written, or if you don't have the right to claim the debt then, the contract becomes null and void.

No. California promissory notes do not need to be notarized or witnessed for validity.

Write the date of the writing of the promissory note at the top of the page. Write the amount of the note. Describe the note terms. Write the interest rate. State if the note is secured or unsecured. Include the names of both the lender and the borrower on the note, indicating which person is which.

Although a promissory note is usually written on a computer and printed out or a pre-made form is filled out, a handwritten promissory note signed by both parties is legal and will stand up in court.

A promissory note can be secured with a pledge of collateral, which is something of value that can be seized if a borrower defaults.

The lender holds the promissory note while the loan is being repaid, then the note is marked as paid and returned to the borrower when the loan is satisfied. Promissory notes aren't the same as mortgages, but the two often go hand in hand when someone is buying a home.