South Dakota Testamentary Trust Provision for the Establishment of a Trust for a Charitable Institution for the Care and Treatment of Disabled Children

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Testamentary Trust Provision For The Establishment Of A Trust For A Charitable Institution For The Care And Treatment Of Disabled Children?

You can dedicate time online attempting to locate the legal document template that satisfies the federal and state requirements you desire.

US Legal Forms offers numerous legal documents that are reviewed by professionals.

You can conveniently acquire or print the South Dakota Testamentary Trust Provision for the Creation of a Trust for a Charitable Organization for the Care and Treatment of Disabled Children from your services.

If available, use the Review button to browse through the document template as well.

- If you presently possess a US Legal Forms account, you can Log In and click on the Obtain button.

- Next, you can complete, modify, print, or sign the South Dakota Testamentary Trust Provision for the Creation of a Trust for a Charitable Organization for the Care and Treatment of Disabled Children.

- Every legal document template you obtain is yours permanently.

- To obtain another copy of the downloaded form, navigate to the My documents tab and click on the relevant button.

- If you are visiting the US Legal Forms website for the first time, follow the straightforward instructions below.

- First, ensure that you have selected the correct document template for the area/city of your choice.

- Check the form outline to confirm you have selected the appropriate form.

Form popularity

FAQ

To create a testamentary trust, the settlor first must select the trustee and the beneficiary and specify the assets that are to be placed in trust. The settlor also has the ability to specify when and how to disburse the trust to the beneficiary. The last will and testament should detail all of this information.

There are five key elements of trust that drive our philosophy:Reliability: Being reliable creates trust.Honesty: Telling the truth creates trust.Good Will: Acting in good faith creates trust.Competency: Doing your job well creates trust.Open: Being vulnerable creates trust.

A beneficiary to a Testamentary Trust will therefore be entitled to marginal tax rates when being assessed on income from the trust, while also receiving distributed franking credits. This maximises their overall net income.

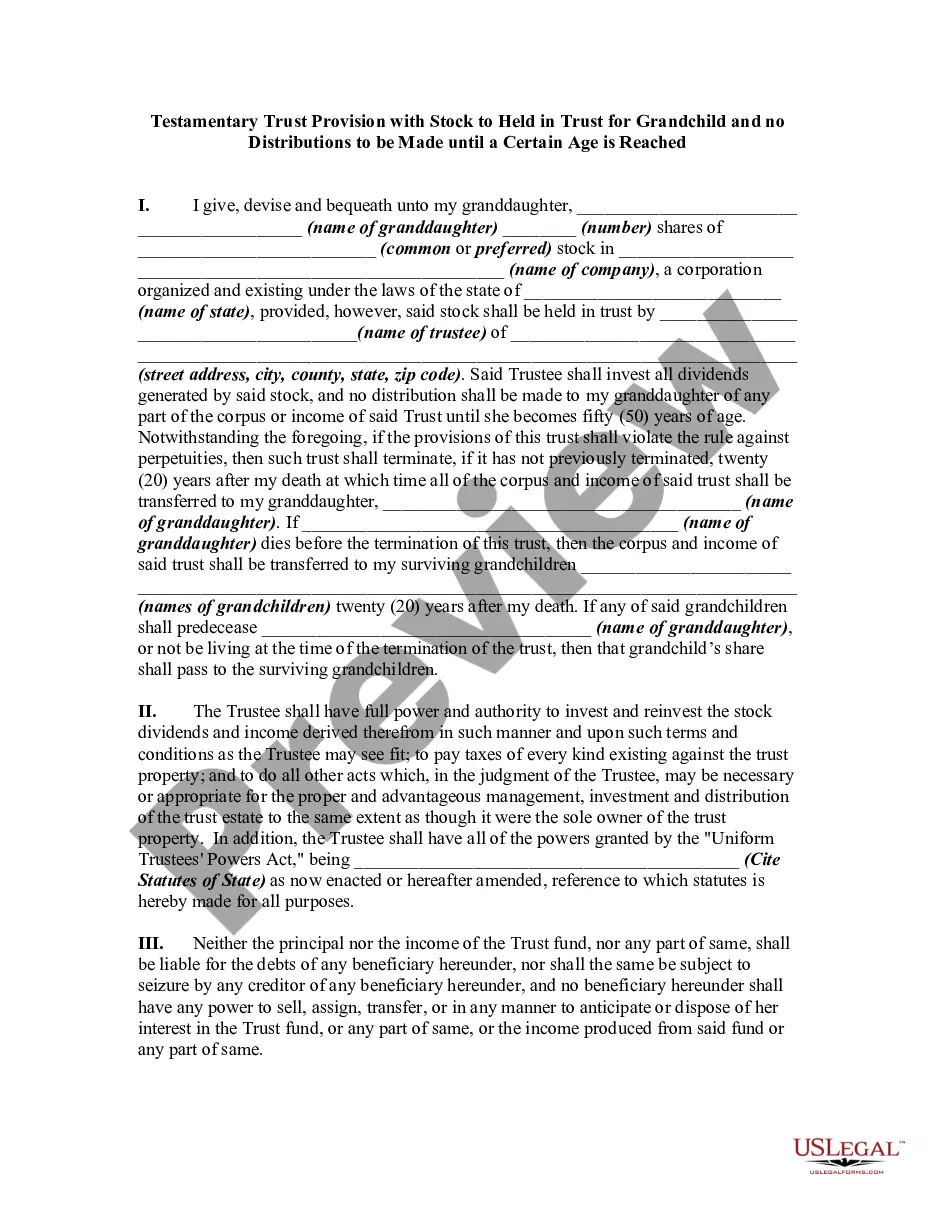

A trust can stipulate, for example, that until age 25, the trust assets are held for the benefit of the beneficiary but that he is not automatically entitled to any distributions unless the trustee believes that a distribution is advisable. At age 25, the beneficiary becomes entitled to one third of the trust assets.

A testamentary trust (a trust established by will after death) is subject to tax at graduated income tax rates. Conversely, an inter vivos trust (a trust created during a settlor's lifetime) is taxed at the highest marginal tax rate applicable to individuals (currently 43.7% in BC).

Testamentary trusts are discretionary trusts established in Wills, that allow the trustees of each trust to decide, from time to time, which of the nominated beneficiaries (if any) may receive the benefit of the distributions from that trust for any given period.

All trusts are required to contain at least the following elements:Trusts must identify the grantor, trustee and beneficiary. The grantor and trustee must be identified because they are parties to the contract.The trust res must be identified.The trust must contain the signature of both the grantor and the trustee.

As part of its definition, a trust is composed of three parties - the trustor, trustee and beneficiary.

The trust can also be used to reduce estate tax liabilities and ensure professional management of the assets. A disadvantage of a testamentary trust is that it does not avoid probatethe legal process of distributing assets through the court.