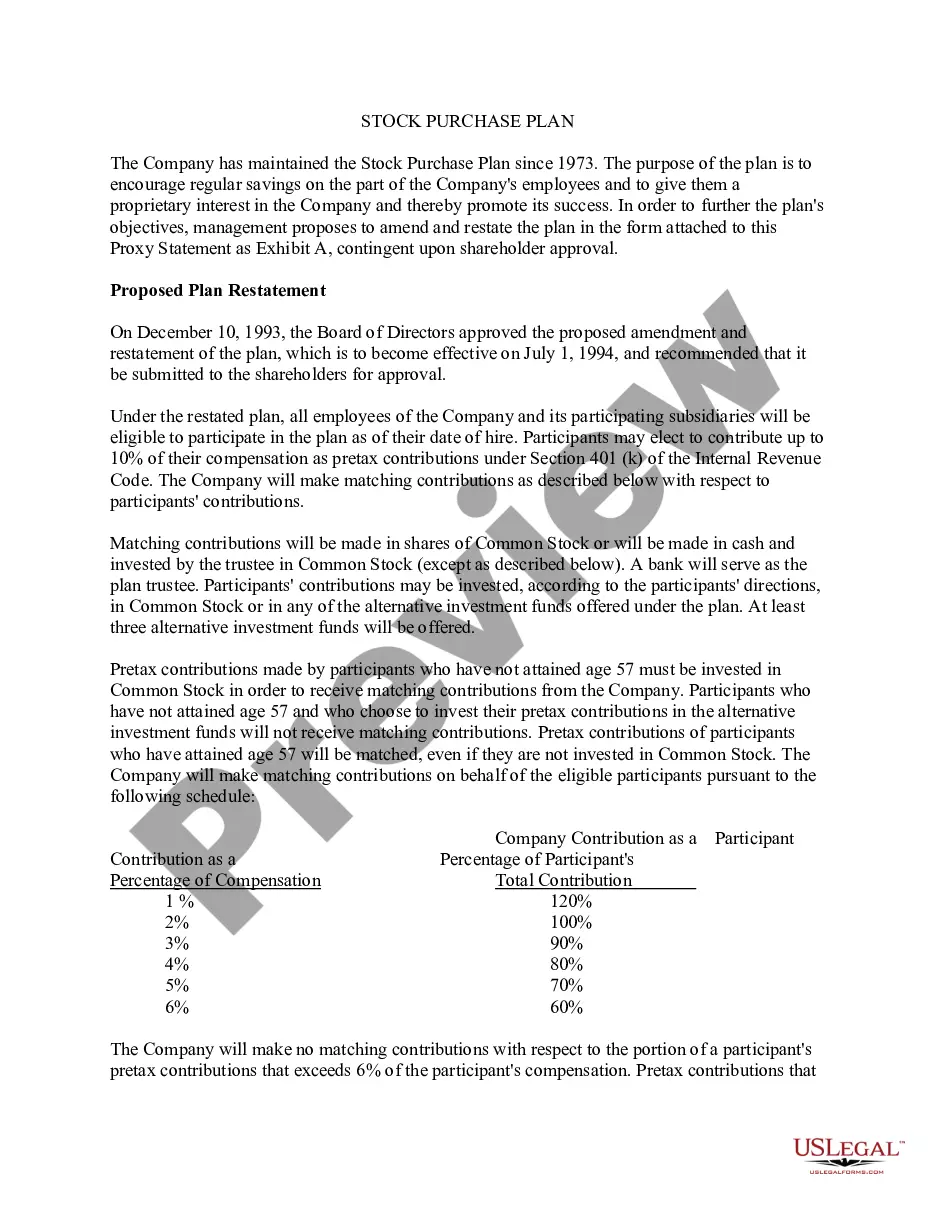

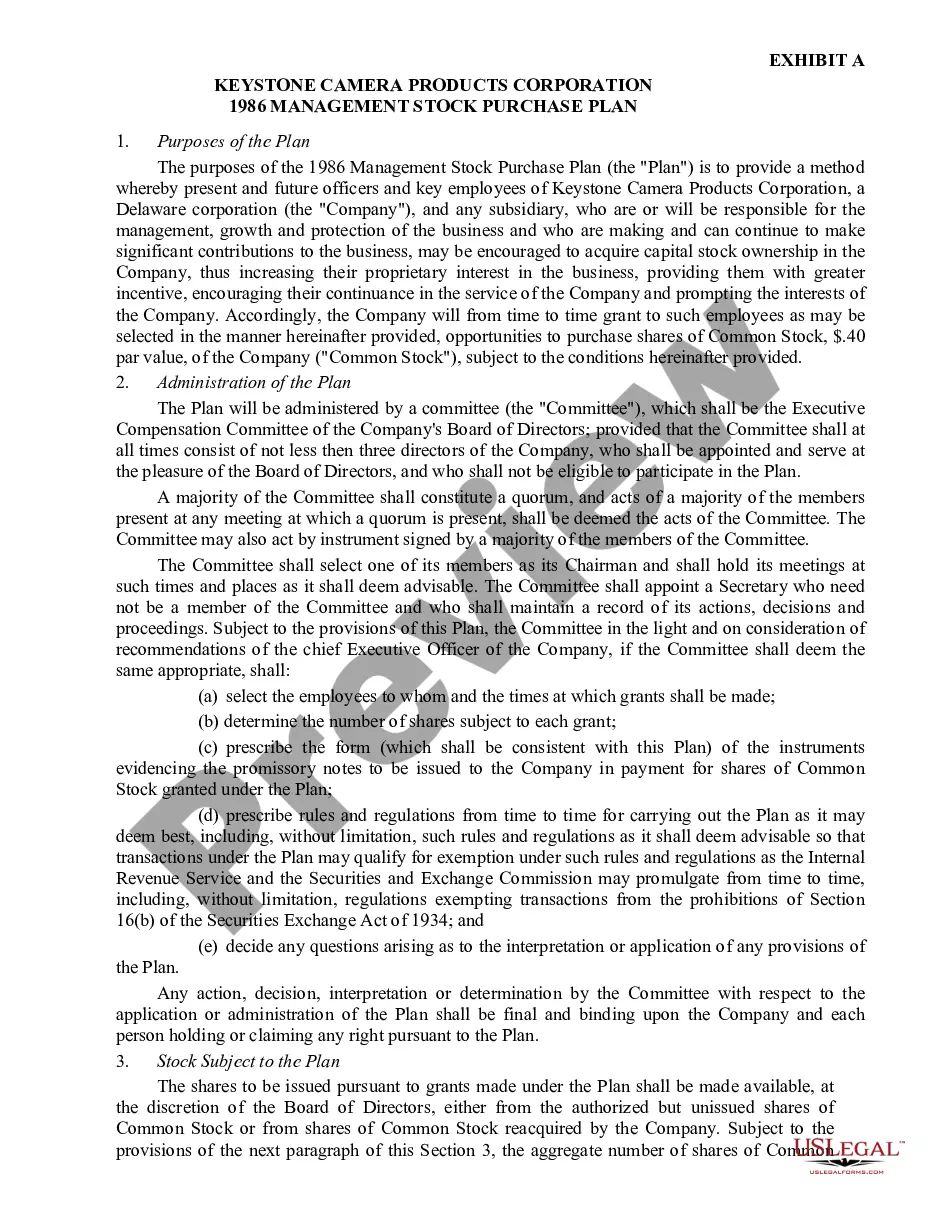

19-179 19-179 . . . Employee Stock Purchase Plan under which each employee of corporation and its wholly-owned direct or indirect, domestic and foreign subsidiaries that have authorized participation in Plan (Participating Company) can contribute up to 15% of earnings through payroll deductions and Participating Company contributes a cash amount equal to 5% of participant's payroll deductions for first year of participation, additional 7% for second year, additional 10% for third year, additional 13% for fourth year and additional 15% for fifth year. Custodian of plan purchases shares of common stock on open market or from corporation at current market prices, using payroll deductions and applicable matching Company contributions

South Carolina Amended and Restated Employee Stock Purchase Plan

Category:

State:

Multi-State

Control #:

US-CC-19-179

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Amended And Restated Employee Stock Purchase Plan?

US Legal Forms - one of many greatest libraries of authorized kinds in America - provides an array of authorized document layouts you may acquire or print out. Utilizing the internet site, you will get a huge number of kinds for enterprise and person purposes, sorted by groups, states, or key phrases.You will find the latest models of kinds just like the South Carolina Amended and Restated Employee Stock Purchase Plan within minutes.

If you currently have a membership, log in and acquire South Carolina Amended and Restated Employee Stock Purchase Plan from the US Legal Forms catalogue. The Obtain switch will show up on every kind you perspective. You get access to all in the past delivered electronically kinds in the My Forms tab of your own profile.

If you would like use US Legal Forms for the first time, allow me to share straightforward directions to obtain started out:

- Be sure to have chosen the correct kind for your city/area. Go through the Preview switch to review the form`s articles. Look at the kind information to ensure that you have selected the proper kind.

- In case the kind doesn`t match your demands, utilize the Look for discipline at the top of the display screen to find the one that does.

- If you are content with the shape, affirm your choice by clicking on the Acquire now switch. Then, opt for the costs prepare you like and offer your accreditations to register for an profile.

- Process the financial transaction. Make use of your bank card or PayPal profile to complete the financial transaction.

- Find the formatting and acquire the shape on your own system.

- Make modifications. Load, edit and print out and signal the delivered electronically South Carolina Amended and Restated Employee Stock Purchase Plan.

Every single template you put into your account lacks an expiration day and is also the one you have forever. So, if you want to acquire or print out yet another duplicate, just check out the My Forms segment and then click about the kind you want.

Get access to the South Carolina Amended and Restated Employee Stock Purchase Plan with US Legal Forms, probably the most substantial catalogue of authorized document layouts. Use a huge number of expert and state-distinct layouts that satisfy your business or person needs and demands.

Form popularity

FAQ

What is a qualified section 423 Plan? A. A qualified 423 employee stock purchase plan allows employees under U.S. tax law to purchase stock at a discount from fair market value without any taxes owed on the discount at the time of purchase.

ESPP lookback allows you to buy shares at a lower price point. An ESPP lookback allows you to purchase the share price of either A: the enrollment date (1 Jan) or B: the purchase date (30 Jun), whichever is lower.

ESPP Eligibility Cannot participate in an ESPP if an employee owns more than 5% of the company's stock. Must be employed with the company for a specific period of time. (e.g., 1 to 2 years). ESPPs are a benefit.

In this situation, you sell your ESPP shares more than one year after purchasing them, but less than two years after the offering date. This is a disqualifying disposition because you sold the stock less than two years after the offering (grant) date.

You may decrease your contribution 1 time during the offering period. If you choose to change your contribution percentage, you must do so at least 15 days before the purchase date. For example, if the purchase date is June 30, you must make this change prior to June 15.

Taxes on your ESPP transaction will depend on whether the sale is a qualifying disposition or not. The sale will be considered a qualifying disposition if it meets both of these criteria: You held the stocks for at least one year from the PURCHASE date. You held the stocks for at least two years from the OFFERING date.

If your company offers a tax-qualified ESPP and you decide to participate, the IRS will only allow you to purchase a maximum of $25,000 worth of stock in a calendar year. Any contributions that exceed this amount are refunded back to you by your company.

If your company offers a tax-qualified ESPP and you decide to participate, the IRS will only allow you to purchase a maximum of $25,000 worth of stock in a calendar year. Any contributions that exceed this amount are refunded back to you by your company.