South Carolina Sample Letter for Insufficient Amount to Reinstate Loan

Description

How to fill out Sample Letter For Insufficient Amount To Reinstate Loan?

If you need detailed, obtain, or generate legal document templates, utilize US Legal Forms, the largest repository of legal forms available online.

Take advantage of the site's user-friendly and efficient search feature to locate the documents you need.

A variety of templates for business and personal purposes are categorized by type, region, or keywords.

Step 4. After you find the form you need, click the Buy now button. Choose your preferred pricing plan and enter your details to create an account.

Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the purchase.

- Utilize US Legal Forms to access the South Carolina Sample Letter for Insufficient Amount to Reinstate Loan in just a few clicks.

- If you're an existing US Legal Forms user, Log In to your account and click the Download button to obtain the South Carolina Sample Letter for Insufficient Amount to Reinstate Loan.

- You can also find forms you've previously acquired under the My documents tab in your account.

- If you are using US Legal Forms for the first time, follow the steps below.

- Step 1. Ensure you have chosen the form for the correct city/state.

- Step 2. Use the Preview option to review the form’s details. Don’t forget to read the summary.

- Step 3. If you are not satisfied with the form, utilize the Search area at the top of the screen to find other forms within the legal document repository.

Form popularity

FAQ

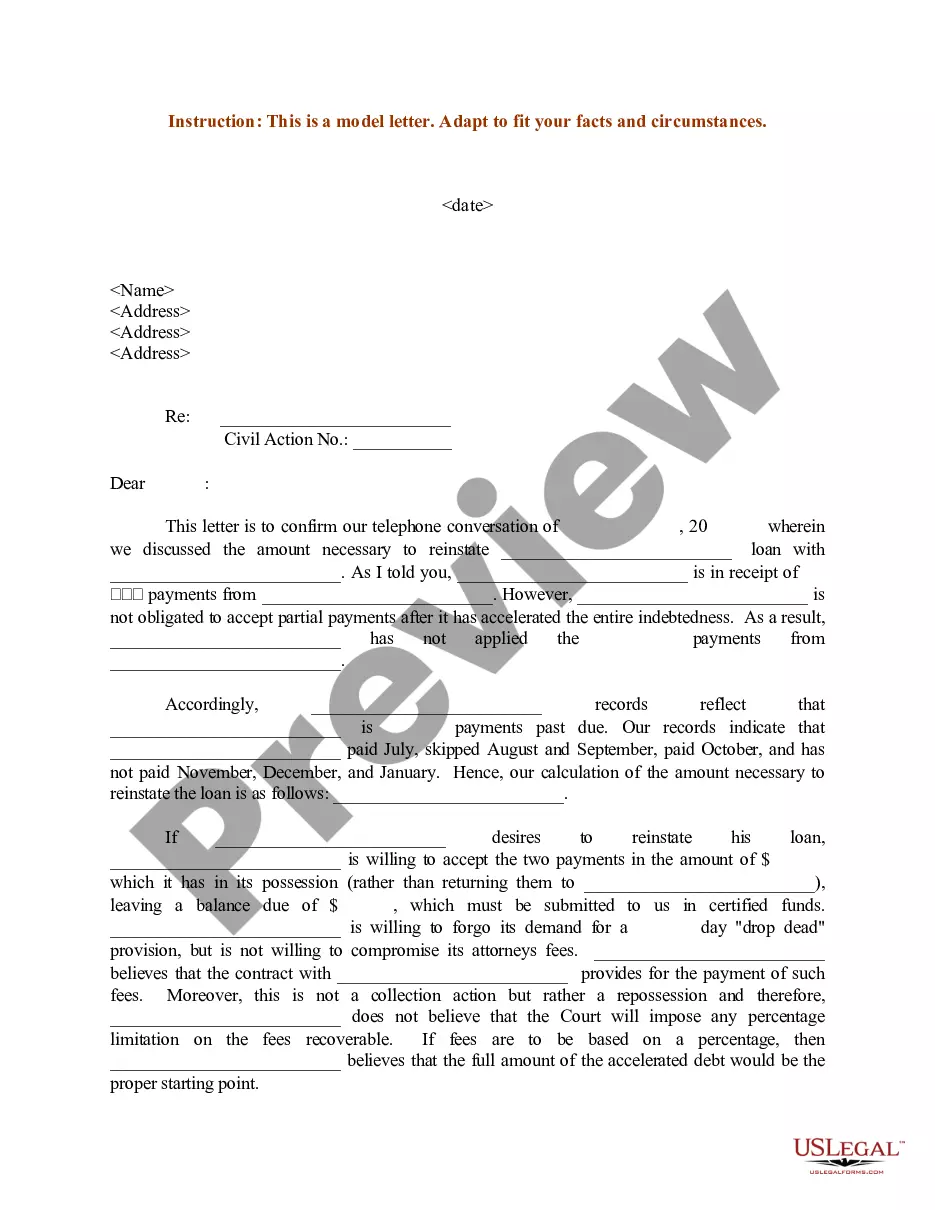

When a lender fails to provide satisfaction of a mortgage in South Carolina, it may lead to legal complications for both the borrower and the lender. The borrower could face difficulties in securing future loans, while the lender may encounter issues with compliance. It is advisable to document all communications and, if necessary, reference a South Carolina Sample Letter for Insufficient Amount to Reinstate Loan to address any outstanding obligations. This proactive approach can help in resolving misunderstandings efficiently.

The right to cure in South Carolina allows borrowers who are behind on their loan payments to rectify the situation before foreclosure proceedings begin. This means you can bring your payments up to date within a specified time frame. To exercise this right, you may want to consider using a South Carolina Sample Letter for Insufficient Amount to Reinstate Loan as part of your communication with the lender. This letter can help ensure that your intent to cure is clear.

Laws governing car repossession in South Carolina require lenders to adhere to fair practices. Lenders must notify borrowers of their default status and ensure they do not breach the peace during the repossession process. You can utilize the South Carolina Sample Letter for Insufficient Amount to Reinstate Loan as a means to negotiate terms or clarify any misunderstandings with the lender. Understanding these laws helps in navigating tough situations effectively.

In South Carolina, lenders typically initiate repossession after one or two missed payments, depending on the terms of your loan. Each contract is different, so checking your specific financing agreement is crucial. If you're worried about missing payments, utilize a South Carolina Sample Letter for Insufficient Amount to Reinstate Loan to communicate with your lender. It’s always better to take proactive steps to avoid repossession.

The South Carolina Lemon Law protects consumers from defective vehicles that fail to meet quality standards. If your vehicle has significant issues that cannot be repaired after a reasonable number of attempts, you may be entitled to a replacement or refund. While dealing with such cases, you might want to reference a South Carolina Sample Letter for Insufficient Amount to Reinstate Loan when discussing potential financing options. This will ensure you manage your financial obligations correctly while seeking resolution.

Repossession laws in South Carolina allow lenders to reclaim vehicles when borrowers default on loans. However, lenders must follow specific legal procedures, including providing proper notice to the borrower. If you're facing repossession, consider using a South Carolina Sample Letter for Insufficient Amount to Reinstate Loan to negotiate terms. Understanding these laws can empower you to protect your rights as a borrower.

In South Carolina, a lender can repossess your vehicle if you miss just one payment, although they typically notify you before taking such action. Repossession can happen quickly, making it crucial to stay informed about your payment obligations. Writing a South Carolina Sample Letter for Insufficient Amount to Reinstate Loan can be a proactive step to discuss your situation with the lender and explore your options.

The statute of limitations on credit card debt in South Carolina is three years. This means that creditors have three years from the last payment made to pursue a lawsuit for the outstanding debt. Knowing this timeline can assist you in creating a strategic plan for debt management, including how to address insufficient amounts with tools such as the South Carolina Sample Letter for Insufficient Amount to Reinstate Loan.

In South Carolina, a lender may initiate foreclosure proceedings after a borrower misses three consecutive mortgage payments. This timeline emphasizes the importance of addressing payment issues promptly. For those in this situation, utilizing a South Carolina Sample Letter for Insufficient Amount to Reinstate Loan can be an effective way to communicate with the lender and potentially avoid foreclosure.

Section 29 3 330 of the SC Code of Laws outlines the requirements and procedures for loan reinstatement in South Carolina. This section details the rights of borrowers facing repayment issues and specifies what constitutes an insufficient amount to reinstate a loan. For those looking to navigate these complex regulations, the South Carolina Sample Letter for Insufficient Amount to Reinstate Loan can provide the necessary foundation for communication with lenders.