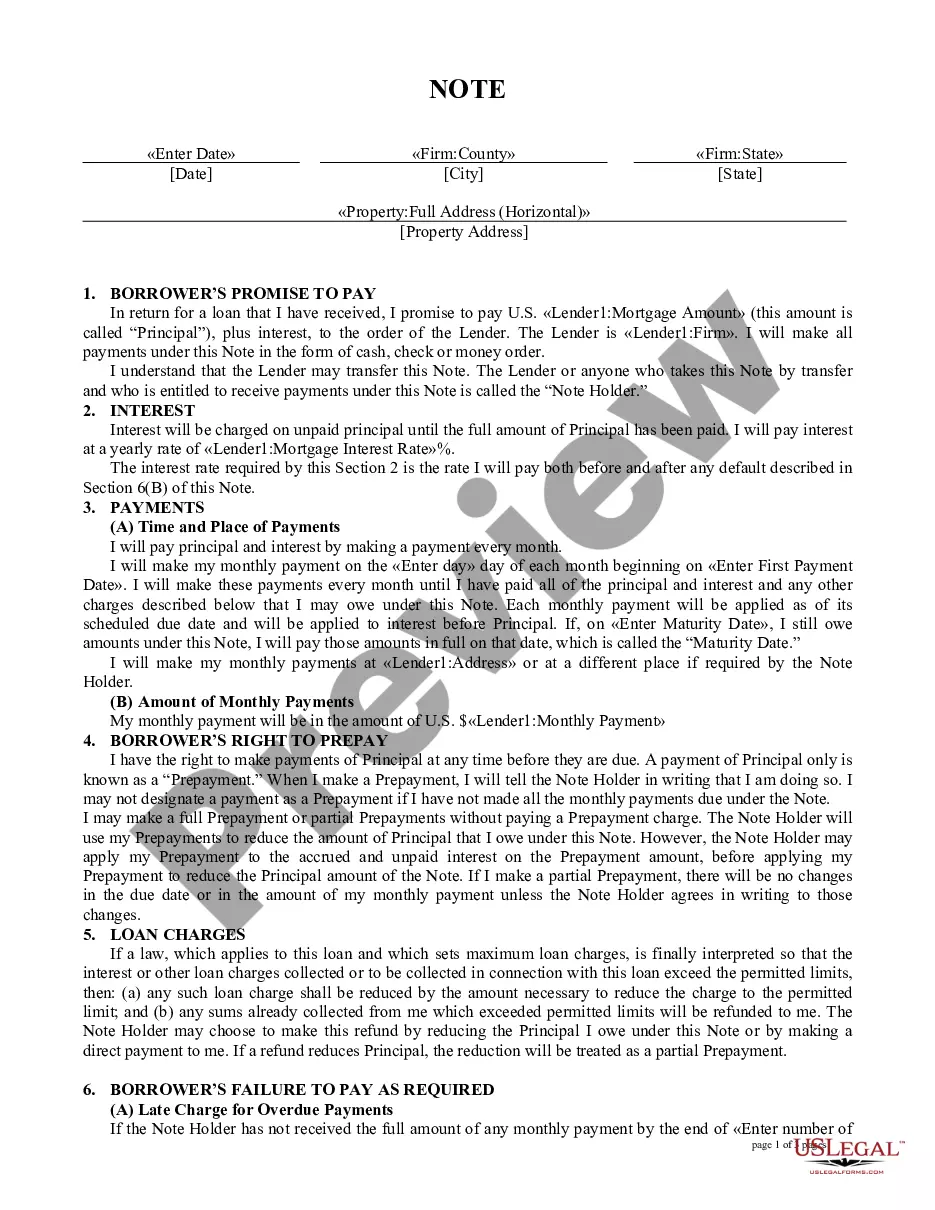

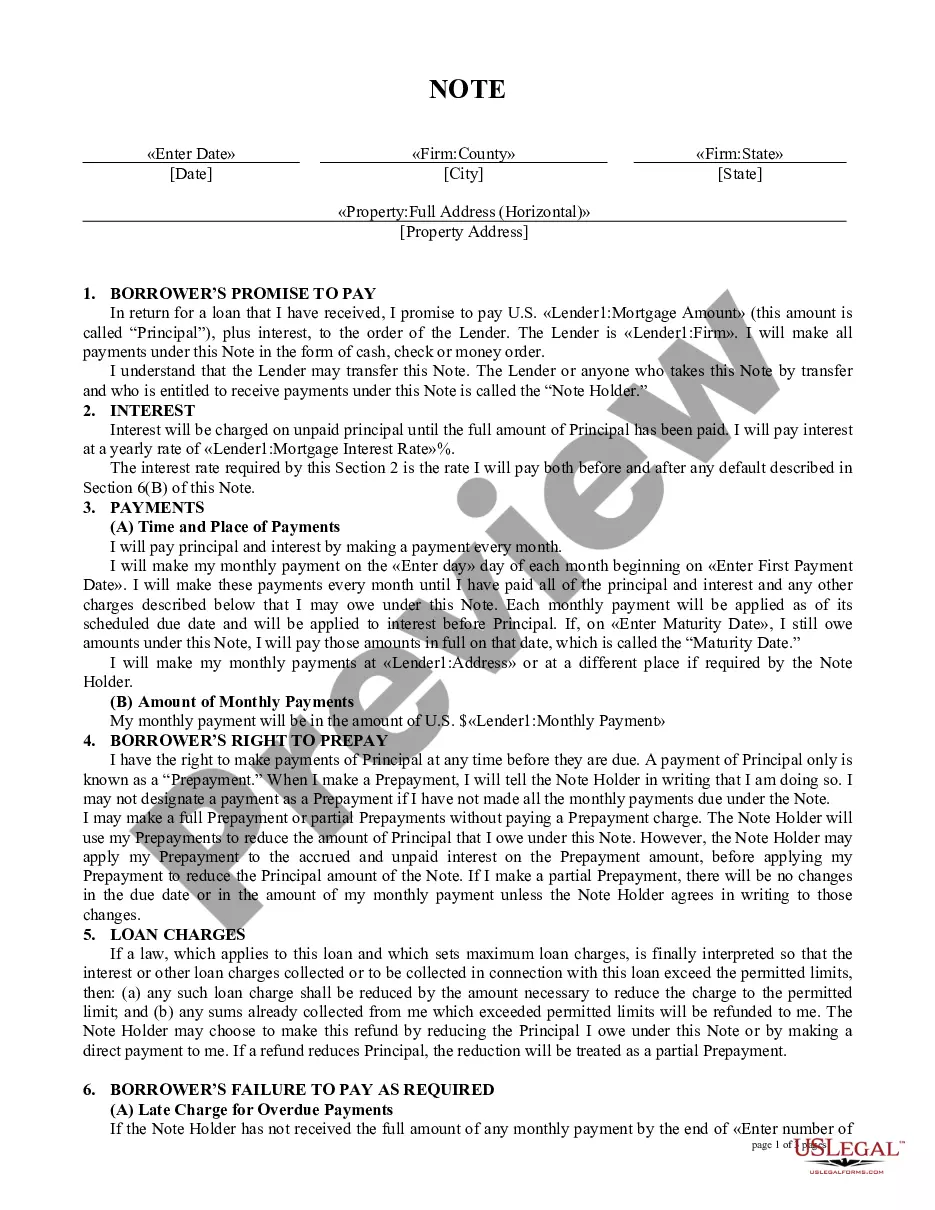

South Carolina Mortgage Note

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Mortgage Note?

You are able to devote hrs on the web attempting to find the legitimate record format that fits the state and federal specifications you require. US Legal Forms provides 1000s of legitimate forms that are evaluated by experts. You can actually acquire or produce the South Carolina Mortgage Note from the service.

If you have a US Legal Forms accounts, it is possible to log in and click on the Acquire option. After that, it is possible to total, modify, produce, or indicator the South Carolina Mortgage Note. Every single legitimate record format you buy is your own permanently. To get one more duplicate associated with a acquired develop, check out the My Forms tab and click on the related option.

If you are using the US Legal Forms internet site the very first time, adhere to the basic guidelines beneath:

- Initially, make certain you have chosen the right record format to the region/area that you pick. Browse the develop description to ensure you have selected the proper develop. If offered, utilize the Review option to search from the record format too.

- In order to find one more edition from the develop, utilize the Look for area to discover the format that suits you and specifications.

- Upon having discovered the format you want, click Acquire now to move forward.

- Pick the rates program you want, enter your credentials, and sign up for a free account on US Legal Forms.

- Full the deal. You should use your bank card or PayPal accounts to pay for the legitimate develop.

- Pick the structure from the record and acquire it in your gadget.

- Make alterations in your record if possible. You are able to total, modify and indicator and produce South Carolina Mortgage Note.

Acquire and produce 1000s of record web templates utilizing the US Legal Forms web site, that provides the biggest selection of legitimate forms. Use professional and state-certain web templates to take on your organization or individual demands.

Form popularity

FAQ

A mortgage note is the document that you sign at the end of your home closing. It should accurately reflect all the terms of the agreement between the borrower and the lender or be corrected immediately if it doesn't.

A promissory note is a written agreement containing the details of the mortgage loan, whereas a mortgage is a loan that is secured by real property. A promissory note is often referred to as a mortgage, but they are separate contracts.

Promissory notes are used to evidence a debt of the mortgagor entity incurred as a result of the development of an insured multifamily project and must receive HUD approval prior to their issuance. (As used herein, "Promissory Notes" refers to surplus cash notes and or residual receipts notes.)

Your lender will typically provide you with a copy of the promissory note, along with several other documents, when you close on your home purchase. The lender will keep the original promissory note until the loan is paid off.

So, as a rule of thumb, if someone is on the Deed, they must be on the Mortgage. But just because they are on the Mortgage, doesn't mean they are on the Note.

A borrower usually must sign a promissory note along with the mortgage. The promissory note gives legal protections to the lender if the borrower defaults on the debt and provides clarification to the borrower so that they understand their repayment obligations.

Promissory notes may also be referred to as an IOU, a loan agreement, or just a note. It's a legal lending document that says the borrower promises to repay to the lender a certain amount of money in a certain time frame. This kind of document is legally enforceable and creates a legal obligation to repay the loan.

Promissory Note Vs. Mortgage. A promissory note is a document between the lender and the borrower in which the borrower promises to pay back the lender, it is a separate contract from the mortgage. The mortgage is a legal document that ties or "secures" a piece of real estate to an obligation to repay money.