South Carolina MAKING EXTORTIONATE EXTENSIONS OF CREDIT

Description

How to fill out South Carolina MAKING EXTORTIONATE EXTENSIONS OF CREDIT?

How much time and resources do you typically spend on composing official paperwork? There’s a better opportunity to get such forms than hiring legal experts or wasting hours browsing the web for a proper template. US Legal Forms is the leading online library that provides professionally designed and verified state-specific legal documents for any purpose, like the South Carolina MAKING EXTORTIONATE EXTENSIONS OF CREDIT.

To obtain and prepare a suitable South Carolina MAKING EXTORTIONATE EXTENSIONS OF CREDIT template, adhere to these simple steps:

- Examine the form content to ensure it complies with your state regulations. To do so, read the form description or use the Preview option.

- In case your legal template doesn’t meet your needs, locate another one using the search bar at the top of the page.

- If you already have an account with us, log in and download the South Carolina MAKING EXTORTIONATE EXTENSIONS OF CREDIT. Otherwise, proceed to the next steps.

- Click Buy now once you find the right document. Opt for the subscription plan that suits you best to access our library’s full service.

- Sign up for an account and pay for your subscription. You can make a payment with your credit card or through PayPal - our service is totally reliable for that.

- Download your South Carolina MAKING EXTORTIONATE EXTENSIONS OF CREDIT on your device and complete it on a printed-out hard copy or electronically.

Another advantage of our library is that you can access previously purchased documents that you safely store in your profile in the My Forms tab. Obtain them at any moment and re-complete your paperwork as frequently as you need.

Save time and effort completing legal paperwork with US Legal Forms, one of the most reliable web solutions. Sign up for us today!

Form popularity

FAQ

In South Carolina, the statute of limitations for most types of consumer and business debt is three years. Residents of South Carolina have several rights when it comes to paying off debt and it is important to understand each one to avoid being taken advantage of by debt collectors.

SECTION 37-5-104. No garnishment. With respect to a debt arising from a consumer credit sale, a consumer lease, a consumer loan, or a consumer rental-purchase agreement, regardless of where made, the creditor may not attach unpaid earnings of the debtor by garnishment or like proceedings.

Section 37-10-102 of the South Carolina Consumer Protection Code requires a creditor to ascertain and comply with the consumer's preference as to the legal counsel the consumer wants to hire to conduct the transaction.

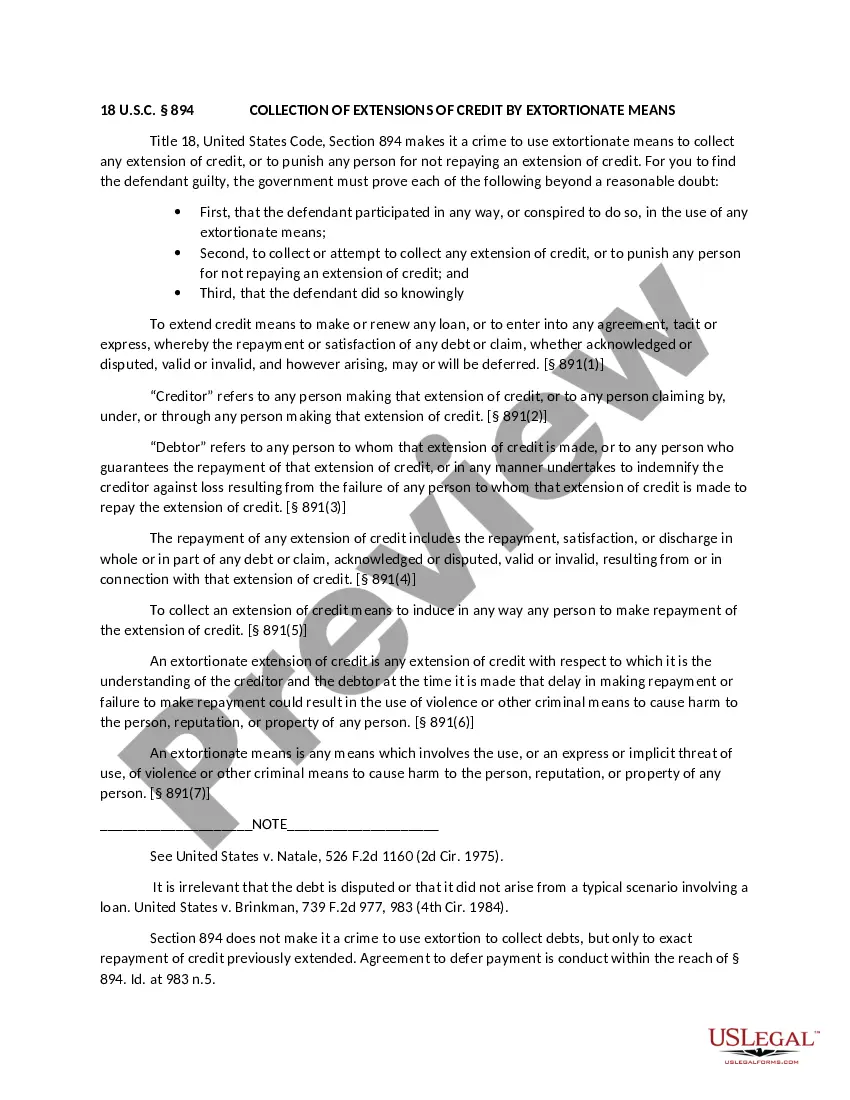

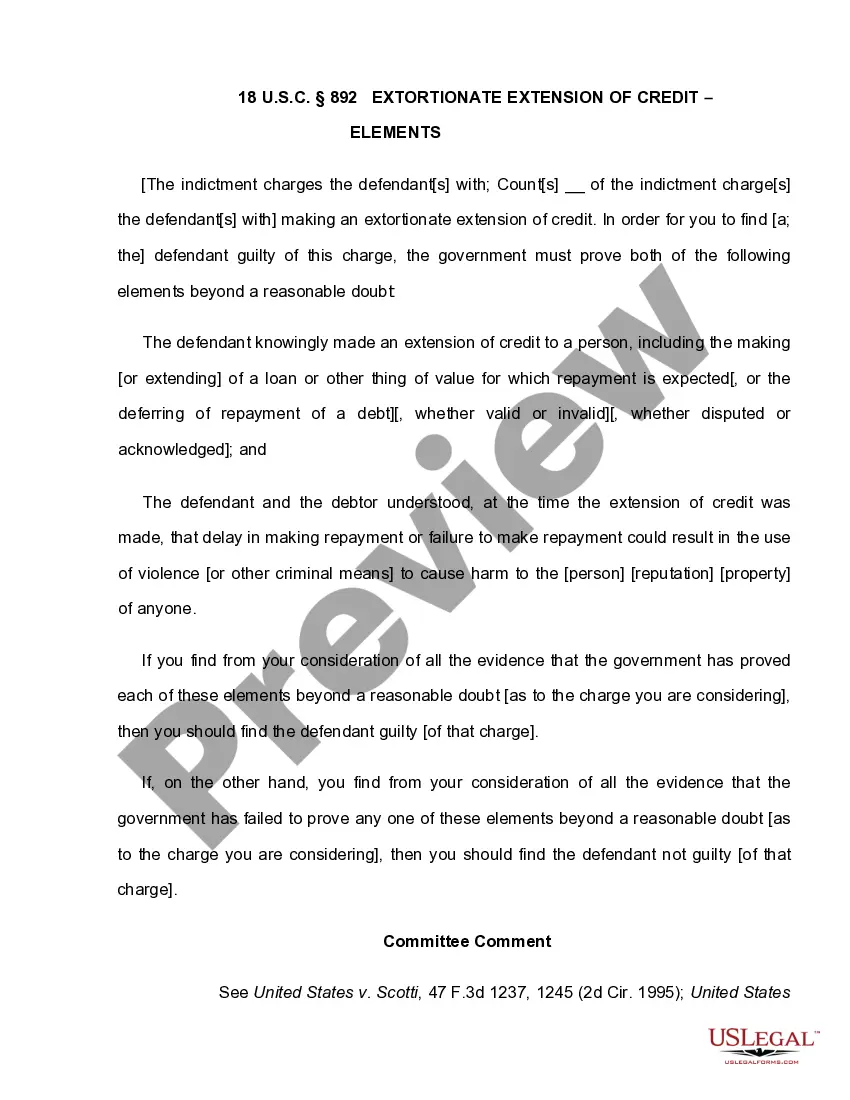

"(2) Extortionate credit transactions are characterized by the use, or the express or implicit threat of the use, of violence or other criminal means to cause harm to person, reputation, or property as a means of enforcing repayment.

(1) With respect to a secured or unsecured consumer credit transaction payable in two or more installments, after a consumer has been in default for ten days for failure to make a required payment and has not voluntarily surrendered possession of goods that are collateral, a creditor may give the consumer the notice