Pennsylvania Breakdown of Savings for Budget and Emergency Fund

Description

How to fill out Breakdown Of Savings For Budget And Emergency Fund?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a range of legal form templates that you can download or create.

By utilizing the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the most current versions of forms such as the Pennsylvania Summary of Savings for Budget and Emergency Fund within moments.

If you are already subscribed monthly, Log In to obtain the Pennsylvania Summary of Savings for Budget and Emergency Fund from the US Legal Forms library. The Download button will appear on each form you view. You can access all previously downloaded forms in the My documents section of your account.

Complete the transaction. Use a credit card or PayPal account to finalize the payment.

Select the format and download the form to your device. Make modifications. Fill out, edit, print, and sign the downloaded Pennsylvania Summary of Savings for Budget and Emergency Fund. Each template added to your account does not have an expiration date, so it is yours indefinitely. If you wish to download or print an additional copy, simply go to the My documents section and click on the form you need. Access the Pennsylvania Summary of Savings for Budget and Emergency Fund with US Legal Forms, one of the most comprehensive libraries of legal document templates. Utilize thousands of professional and state-specific templates that cater to your business or personal needs.

- Ensure that you have selected the appropriate form for your area/region.

- Click on the Review button to examine the details of the form.

- Read the form's summary to confirm you have chosen the right one.

- If the form doesn't suit your needs, use the Search bar at the top of the screen to locate one that does.

- If you are satisfied with the form, confirm your selection by clicking the Get now button.

- Then, choose the payment plan you prefer and provide your credentials to register for the account.

Form popularity

FAQ

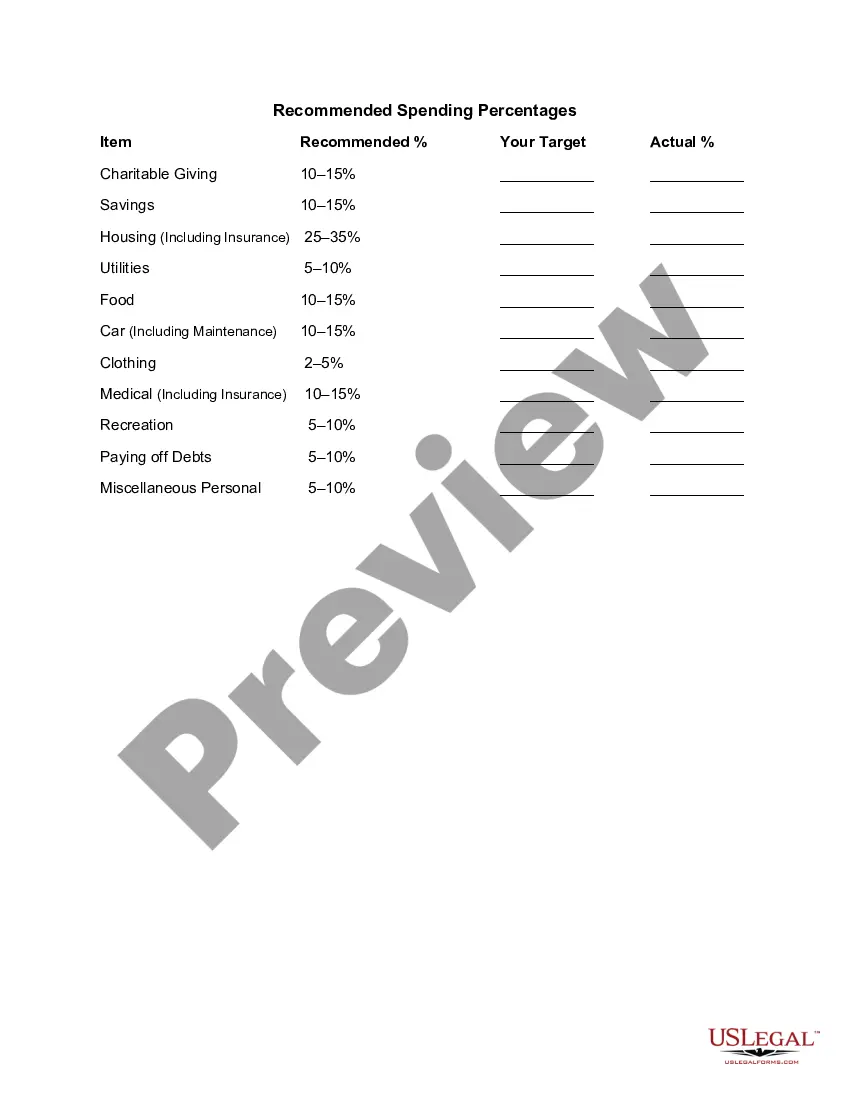

The 50/30/20 budget divides your after-tax income into three separate categories: 50% for needs, 30% for wants and 20% for savings/financial goals. This approach is best for younger, average-income earners who have paid off their high-interest debt.

Our 50/30/20 calculator divides your take-home income into suggested spending in three categories: 50% of net pay for needs, 30% for wants and 20% for savings and debt repayment.

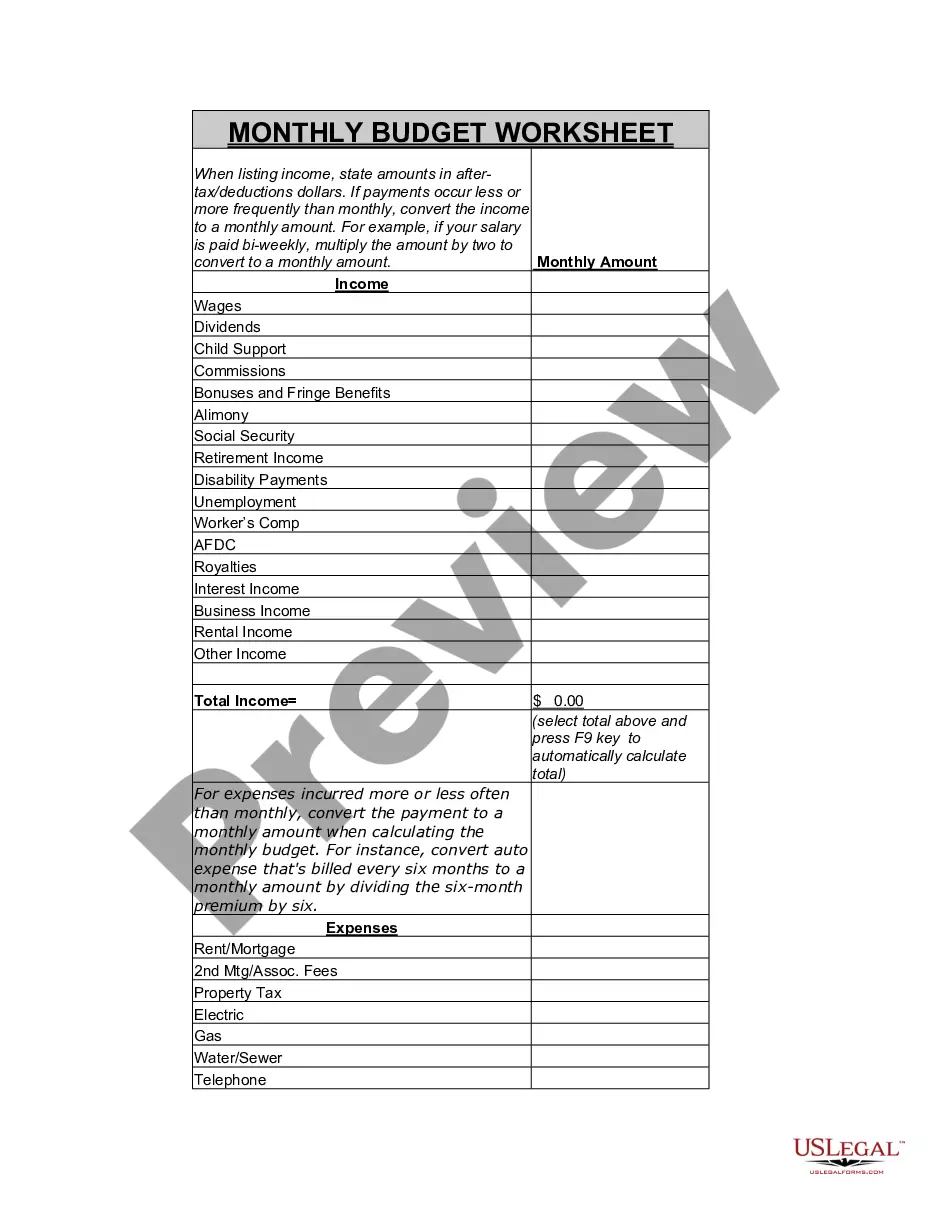

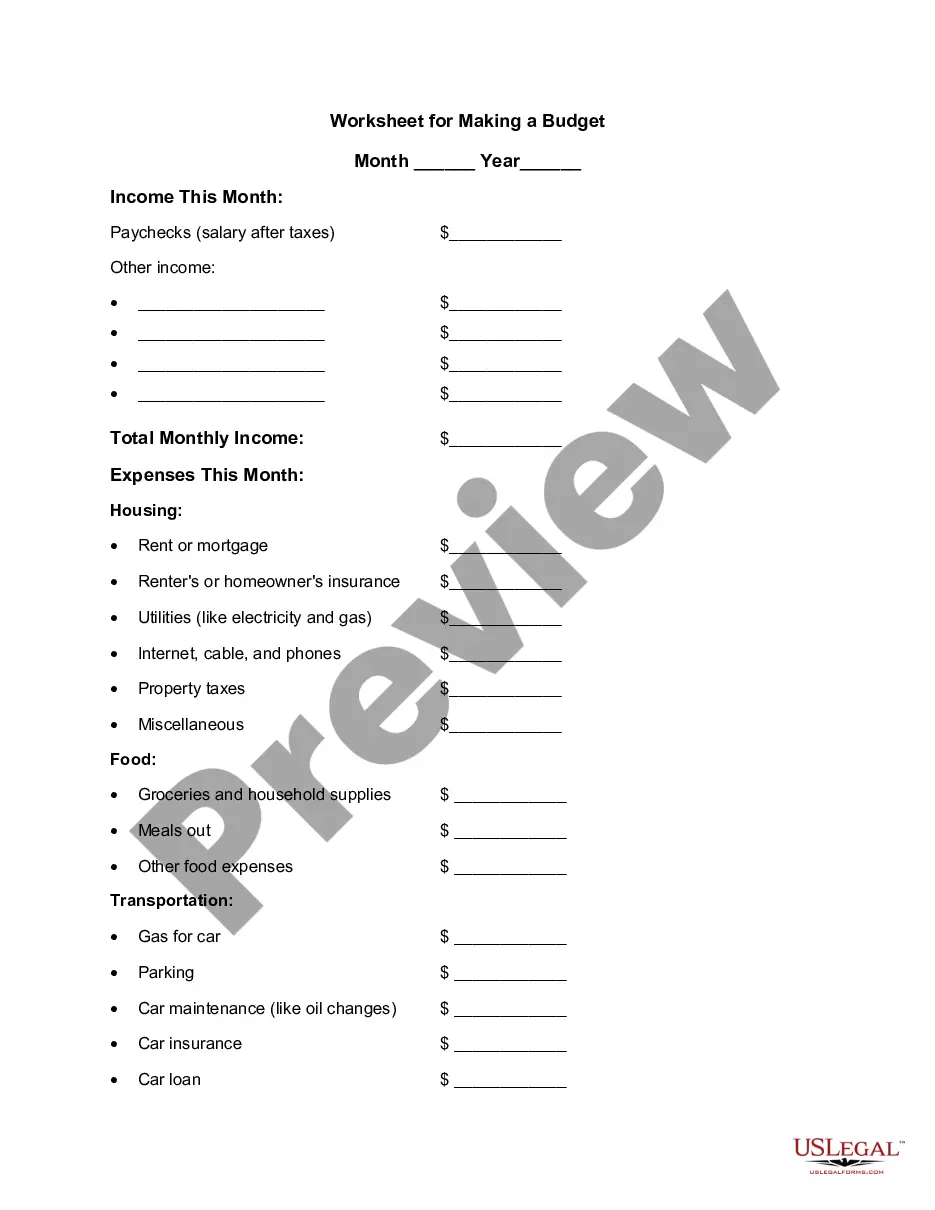

5 Steps to Creating a BudgetStep 1: Determine Your Income. This amount should be your monthly take-home pay after taxes and other deductions.Step 2: Determine Your Expenses.Step 3: Choose Your Budget Plan.Step 4: Adjust Your Habits.Step 5: Live the Plan.

The basic rule is to divide up after-tax income and allocate it to spend: 50% on needs, 30% on wants, and socking away 20% to savings.

Creating a budgetStep 1: Calculate your net income. The foundation of an effective budget is your net income.Step 2: Track your spending.Step 3: Set realistic goals.Step 4: Make a plan.Step 5: Adjust your spending to stay on budget.Step 6: Review your budget regularly.

The 50/30/20 rule budget is a simple way to budget that doesn't involve detailed budgeting categories. Instead, you spend 50% of your after-tax pay on needs, 30% on wants, and 20% on savings or paying off debt.

7 Steps to a Budget Made EasyStep 1: Set Realistic Goals.Step 2: Identify your Income and Expenses.Step 3: Separate Needs and Wants.Step 4: Design Your Budget.Step 5: Put Your Plan Into Action.Step 6: Seasonal Expenses.Step 7: Look Ahead.

While the size of your emergency fund will vary depending on your lifestyle, monthly costs, income, and dependents, the rule of thumb is to put away at least three to six months' worth of expenses.

The basic rule is to divide up after-tax income and allocate it to spend: 50% on needs, 30% on wants, and socking away 20% to savings.

The rule states that you should spend up to 50% of your after-tax income on needs and obligations that you must-have or must-do. The remaining half should be split up between 20% savings and debt repayment and 30% to everything else that you might want.