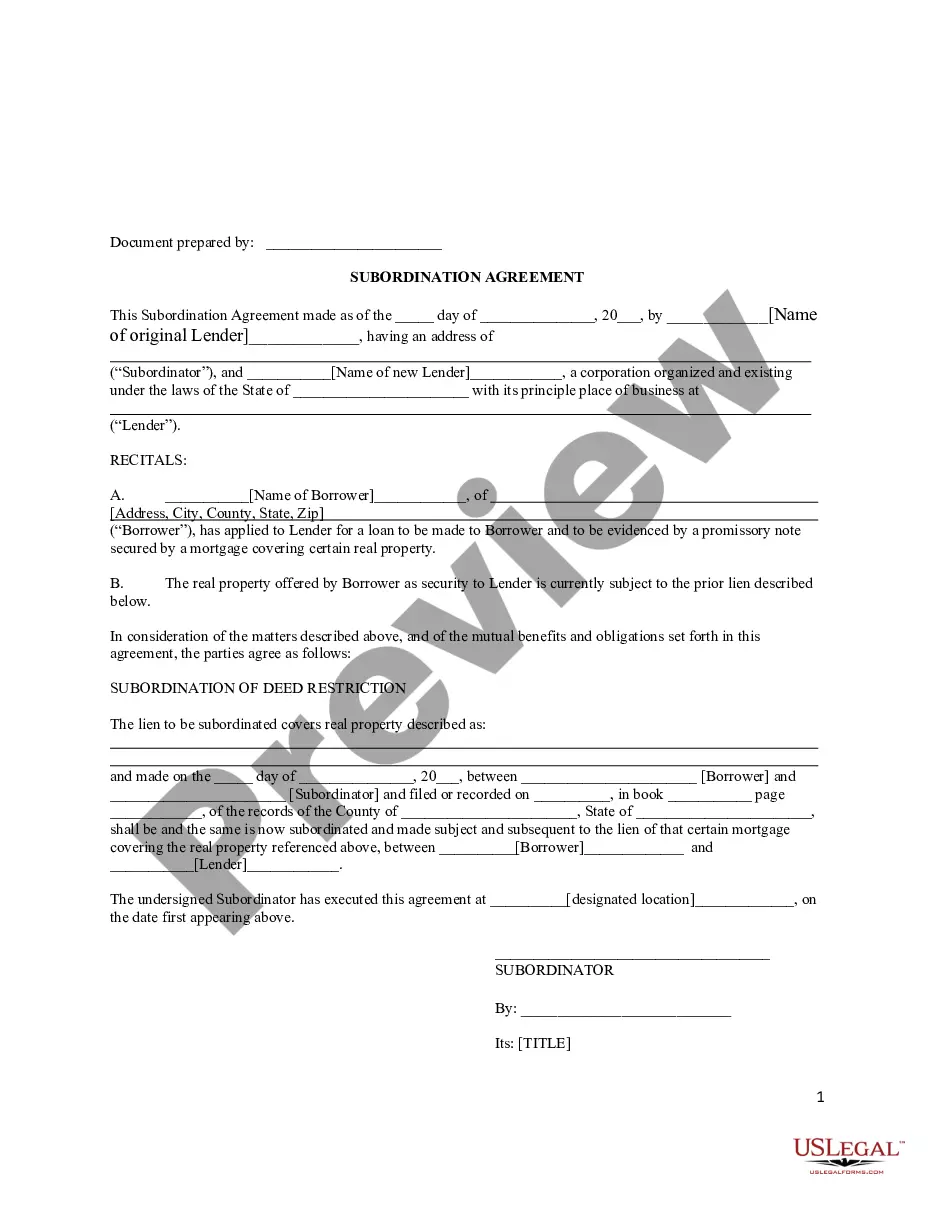

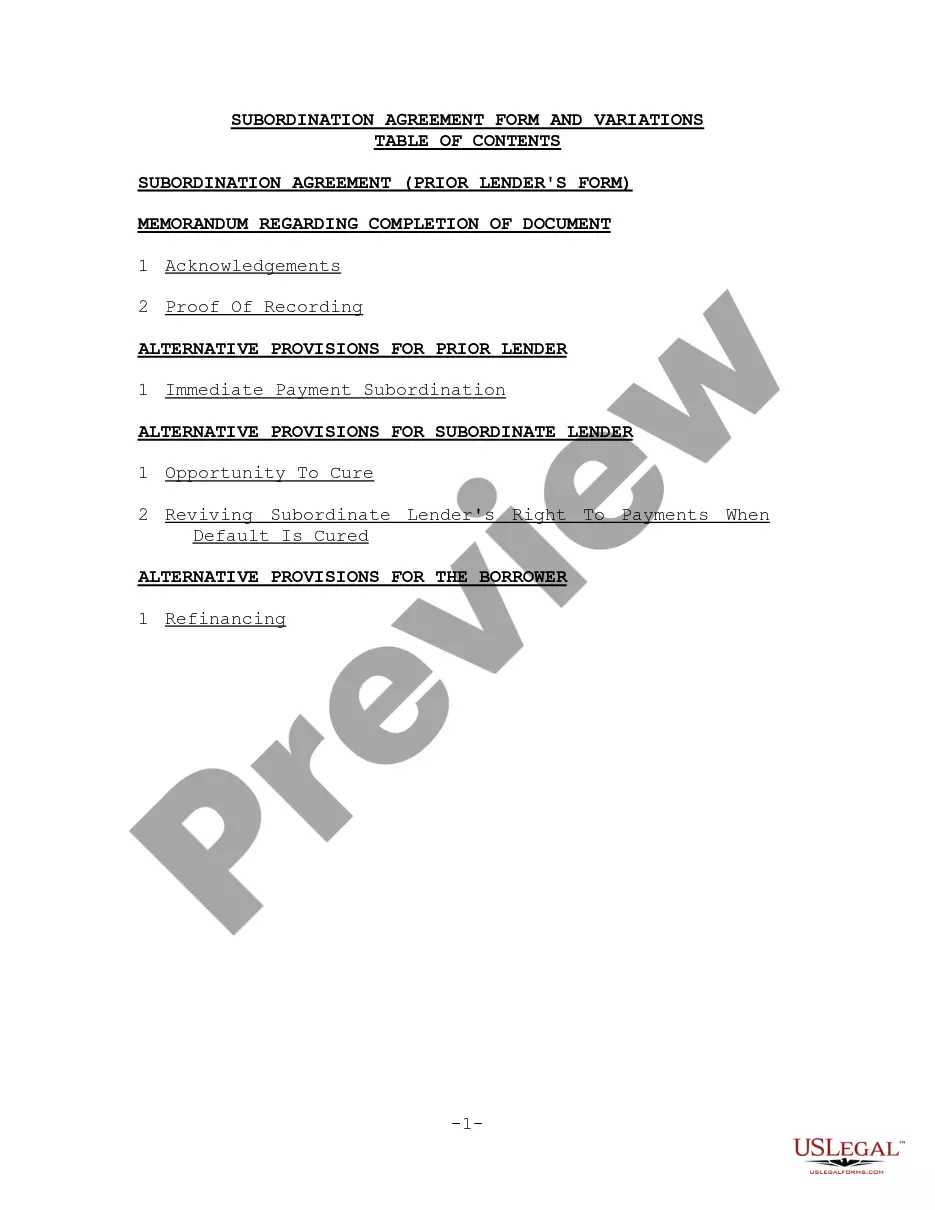

Pennsylvania Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

You may devote time on the Internet trying to find the lawful record template that suits the state and federal demands you need. US Legal Forms gives a huge number of lawful types that happen to be examined by professionals. You can actually obtain or print the Pennsylvania Subordination Agreement Subordinating Existing Mortgage to New Mortgage from your assistance.

If you already possess a US Legal Forms account, you are able to log in and click on the Down load button. Following that, you are able to total, change, print, or sign the Pennsylvania Subordination Agreement Subordinating Existing Mortgage to New Mortgage. Every lawful record template you get is your own eternally. To get one more copy of any acquired kind, visit the My Forms tab and click on the related button.

If you are using the US Legal Forms website for the first time, adhere to the straightforward instructions under:

- First, make sure that you have selected the proper record template for your state/area of your liking. Browse the kind explanation to make sure you have picked the correct kind. If offered, utilize the Preview button to appear with the record template as well.

- In order to find one more version in the kind, utilize the Research field to obtain the template that meets your requirements and demands.

- When you have located the template you need, just click Get now to carry on.

- Select the prices program you need, enter your credentials, and register for a merchant account on US Legal Forms.

- Complete the deal. You can utilize your Visa or Mastercard or PayPal account to purchase the lawful kind.

- Select the format in the record and obtain it to the product.

- Make modifications to the record if possible. You may total, change and sign and print Pennsylvania Subordination Agreement Subordinating Existing Mortgage to New Mortgage.

Down load and print a huge number of record themes while using US Legal Forms web site, which provides the greatest collection of lawful types. Use expert and state-certain themes to tackle your company or specific requires.

Form popularity

FAQ

Adding a person to your mortgage without refinancing can only work if the mortgage is assumable. Federal Housing Administration (FHA) loans tend to be assumable, but other types may not be.

When you refinance your home, you can add or remove co-borrowers from the mortgage and/or title. Adding a co-borrower can be advantageous in some refinancing cases, particularly if the combined income and assets help you qualify for more competitive rates and terms.

A subordinate mortgage loan is any loan not in the first lien position. The subordination order goes by the order the loans were recorded. For example, your first mortgage (the mortgage used to buy the house) is recorded first because it's the first loan you borrow.

In rare cases, lenders will allow you to add additional people to a mortgage although all will have different requirements around doing so. Unfortunately approaching the existing lender route is the exception and most lenders won't allow you to add someone to the mortgage without remortgaging the property with them.

Mortgages typically can't be transferred from one person to another. The borrower is responsible for repaying their home loan until they sell the property. Then the new owner must secure financing on their own. But federal law makes allowances in cases where the primary borrower passes away.

Broadly, there are two types of subordination: structural (common in the UK and mainland Europe) and contractual (common in the US). On a contractual subordination, loans are made to the same company but the senior creditor and junior creditor agree priority of payment by contract.

There are also situations where your first purchase loan can become subordinate by law or regulation, without your lender's agreement. Here are two examples: If you have a Federal tax lien for unpaid income taxes, this debt automatically becomes a primary lien ahead of your first mortgage.

Adding a new husband to a mortgage Your mortgage loan will most likely need to be fully refinanced. Adding a new person to your mortgage loan changes the loan's terms. You won't be able to change these terms unless a lender creates a new loan for you through a mortgage refinance.